CRU

October 15, 2021

CRU: After 14 Months of Gains, Global Sheet Prices Fall

Written by Josh Spoores

By CRU Principal Analyst Josh Spoores, from CRU’s Steel Sheet Products Monitor

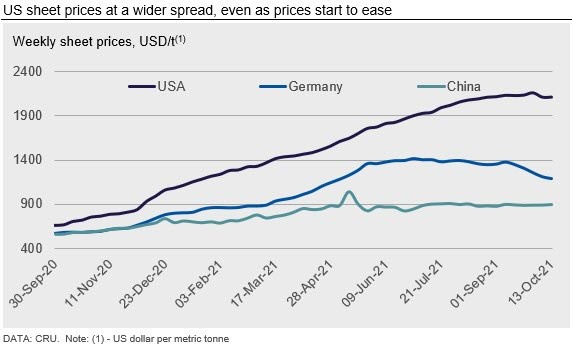

After 14 consecutive months of rising global sheet prices, CRU’s Global Flat Products Steel Price Indicator (CRUspi flats) has fallen m/m. This indicator fell 3.5% as sheet prices continue to fall across most regional markets.

The U.S. Midwest market remains the last holdout of higher prices, yet HR coil prices are now slightly lower from our Sept. 8 assessment. On a weekly basis, HDG coil prices have also fallen back slightly while CR coil prices have made a new record high. Even with these initial declines, the price chart in this section clearly shows the widening spread between the U.S. market and others. This spread has incentivized U.S. buyers to increase their use of imports as current offers of CR and HDG coil remain around $600 /s.ton cheaper, inclusive of all logistics costs and duties.

In China, price volatility remains a prominent issue as daily sheet prices quickly picked up after the National Day holiday, yet earlier this week they eased, somewhat. The government continues to strictly enforce steel production cuts and now with the worsening energy shortage, we are picking up evidence of lower demand for sheet due to the recent power rationing. This issue of significantly higher energy costs has also affected the European market. However, while some mills are now instituting an energy surcharge, we are seeing base sheet prices fall at a quicker pace.

One other market of note is India, where monthly sheet prices have now turned higher after falling through all of 2021 Q3. This gain comes at a time of seasonal restocking, which was delayed due to the well-known supply chain issues surrounding semiconductors. However, even as this market faces their own energy shortage, higher prices here may be limited as a new blast furnace ramps up production.

Outlook: Energy Shortages Threaten Demand

In our near-term view, we continue to expect further price declines across all markets based on regional supply/demand dynamics as well as typical seasonal pressures. Additionally, we expect sheet prices to come back in line with steelmaking raw materials costs, which have also become increasingly volatile. Iron ore prices fell dramatically over the past two months, yet strong gains have been recorded thus far in October.

These recent jumps in iron ore price though have been nothing in comparison with the recent rate of increase for both coking coal and electricity. These rapid price movements may keep sheet prices at a higher rate than previously expected. However, significant gains in energy costs alongside a true shortage of supply have already led to cuts in electricity consumption at an industrial level. Due to this, we expect that sheet demand across multiple regions may now be challenged to reach previously anticipated levels. Worse, we see the increased likelihood that various materials and components will be in short supply if industrial activity is curtailed. After all, an industrial input produced in China today is required for a product manufactured in Europe or North America in the following months. Due to the shortage of thermal coal in China and record high price of LNG in most markets, we have become more concerned with what this means for industrial activity in the near term.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com