Market Data

October 29, 2021

Global Steel Production Falls Further in September

Written by David Schollaert

Steel Market Update is pleased to share this Premium content with Executive members. For information on upgrading to a Premium-levels subscription, email Info@SteelMarketUpdate.com.

World crude steel production fell further in September, contracting for the fourth straight month. Since repeated months of record-breaking output in late Q1 and early Q2, steel production has begun trending down, accentuated by aggressive production cuts in China, according to World Steel Association (worldsteel) data.

Global production in September, at an estimated 144.4 million metric tons, was 8.9% lower than the same year-ago period. September’s total was the third lowest total in nearly two years and rivaled the low mark of 136.9 million metric tons seen in April 2020 when the globe was grappling with the first COVID-19 surge.

Since peaking at 174.4 million metric tons this May, world crude steel production has trended downward. September’s total is 30 million metric tons lower than May’s high and 12.4 million metric tons below August’s total. Total global output in September was greatly affected by an 11.3% drop in Chinese production, along with smaller decreases in seven of the top 10 steel-producing countries, reported worldsteel.

Year-to-date, world crude steel production totaled 1.457 billion metric tons, up by 7.9% compared with the same period in 2020. Production was also up 4.8% when compared to the same pre-pandemic period in 2019.

The U.S. remained the fourth largest crude steel producer in the world in September, accounting for 7.3 million metric tons or 5.1% of the global total. U.S. production in September was down 2.7% from the prior month or 200,000 metric tons. Compared with the same month last year when the economy was struggling with COVID disruptions, September’s production was an improvement of 22.2%, and up 4.2% compared to the pre-pandemic period in 2019.

U.S. production through the first nine months of 2021 totaled 63.8 million metric tons, 18.5% higher than the same period one year ago but still 3.5% or 2.332 million metric tons behind pre-pandemic levels from 2019.

China continued to produce more than half of the world’s steel at 51.1% or an estimated 73.8 million metric tons in September. Chinese production was down 11.3% from the prior month and accounted for nearly three-fourths of the global decline in September. China’s steel production was down 20.3% when compared with September 2020.

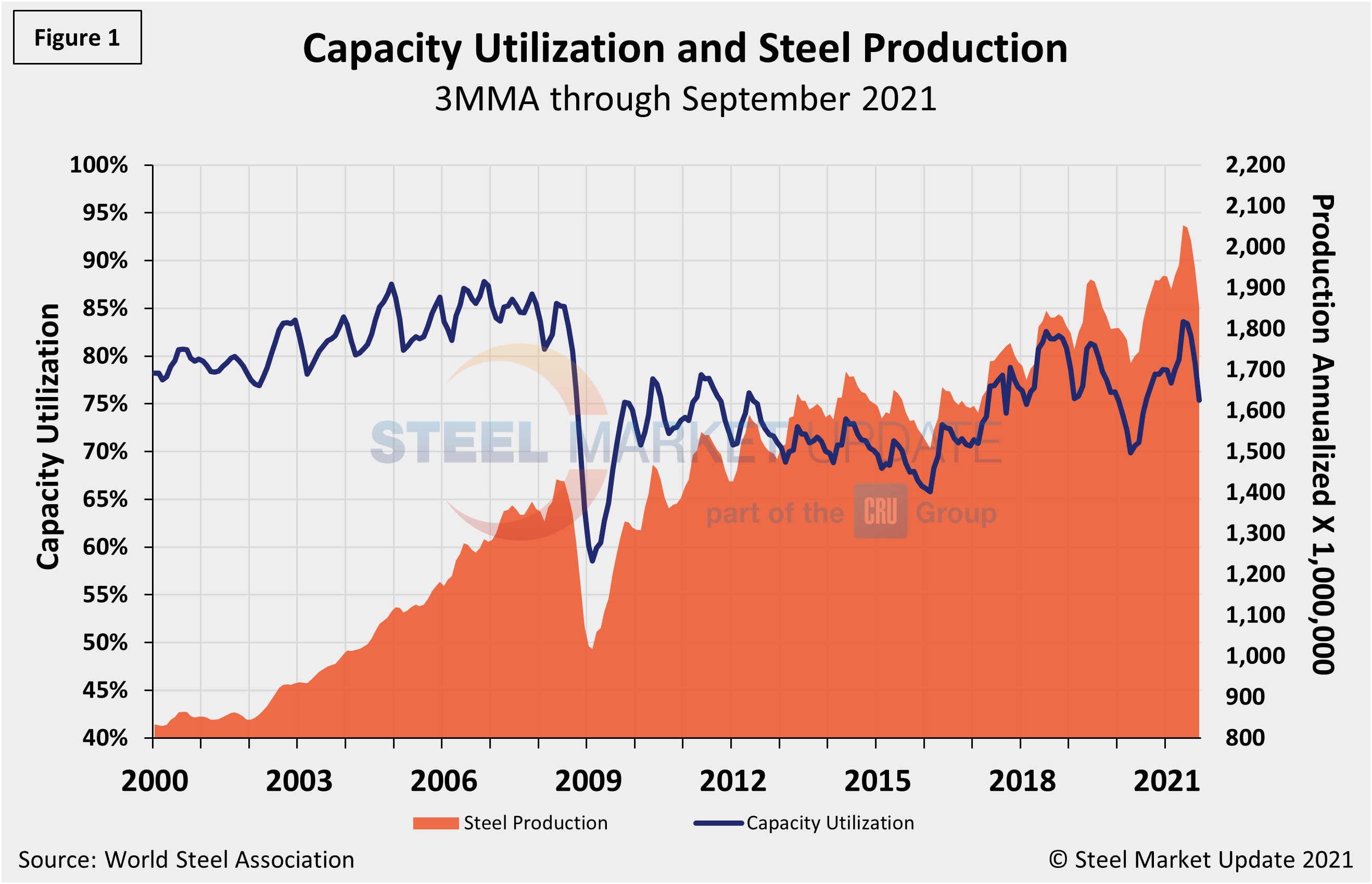

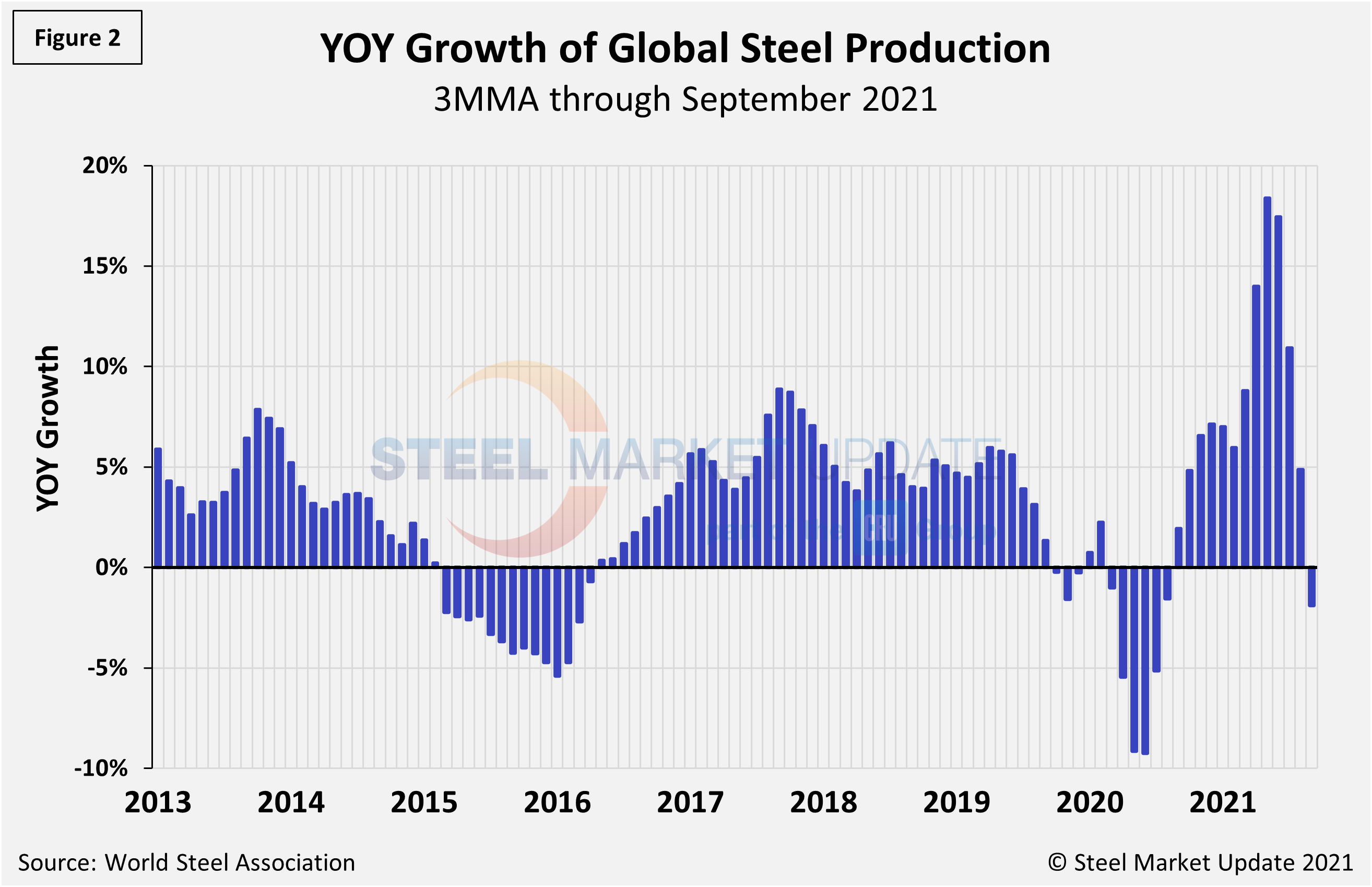

Shown below in Figure 1 is the annualized monthly global steel production on a three-month moving average (3MMA) basis and capacity utilization since January 2000 based on data from worldsteel, while Figure 2 shows the year-over-year growth rate of global production on the same 3MMA basis since January 2013. Capacity utilization in September on a 3MMA basis was 75.4%, down 3.8 percentage points from the month prior. On a tons-per-day basis, production in September was 4.813 million metric tons, down for the fourth straight month following May’s record rate of 5.813 million metric tons, and the lowest daily output since May 2020. Growth on a three-month moving average through September on a year-over-year basis was -1.9%, a collapse from 18.4% expansion seen in May.

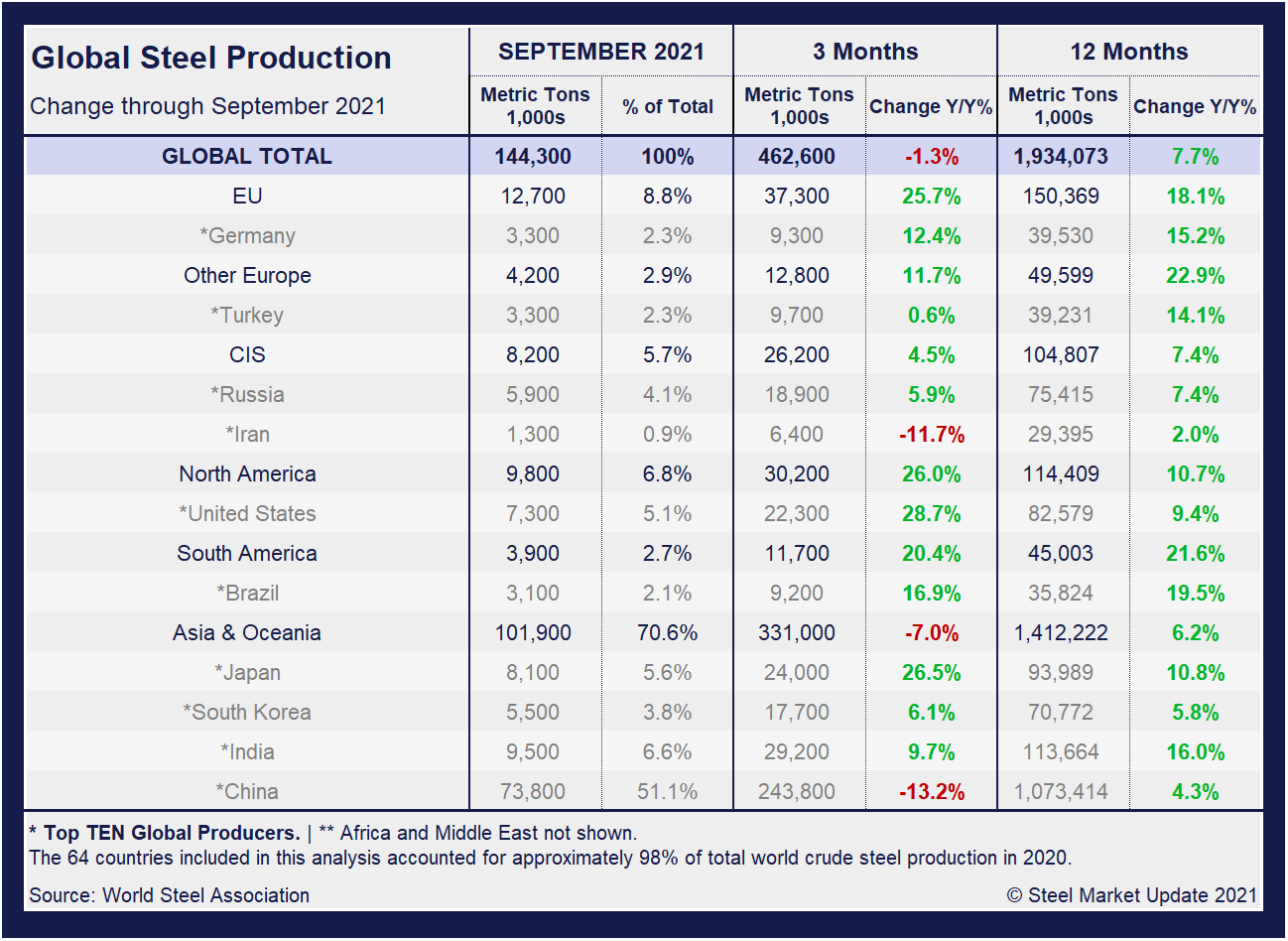

Displayed in the table below is global production broken down into regions, the production of the top 10 nations in the single month of September, and their share of the global total. It also shows the latest three months and 12 months of production through September with year-over-year growth rates for each period. Regions are shown in black font and individual nations in gray. World steel production overall fell 1.3% in three months, a significant deceleration from the 17.9% growth just three months prior. Over 12 months through September, though, growth was 7.7%, down up 0.9 percentage points from the same period in August. The market has not maintained positive momentum, as the three-month growth rate has been lower than the 12-month growth rate for two straight months.

The table shows that North American production was up 26.0% in the three months through September, and up 10.7% year on year. The positive momentum in the North American market is significant as the economy continues to recover from the pandemic. More importantly, when compared to the same pre-pandemic period in 2019, present output is up 1.6%.

China’s Crude Steel Production

China’s monthly steel production was estimated at 73.8 million metric tons in September, down from 83.2 million metric tons the month prior. The 9.4-million-ton month-on-month decrease marks the fourth consecutive decline following repeated record-breaking months of crude steel output, reaching an all-time high of 99.5 million metric tons in May.

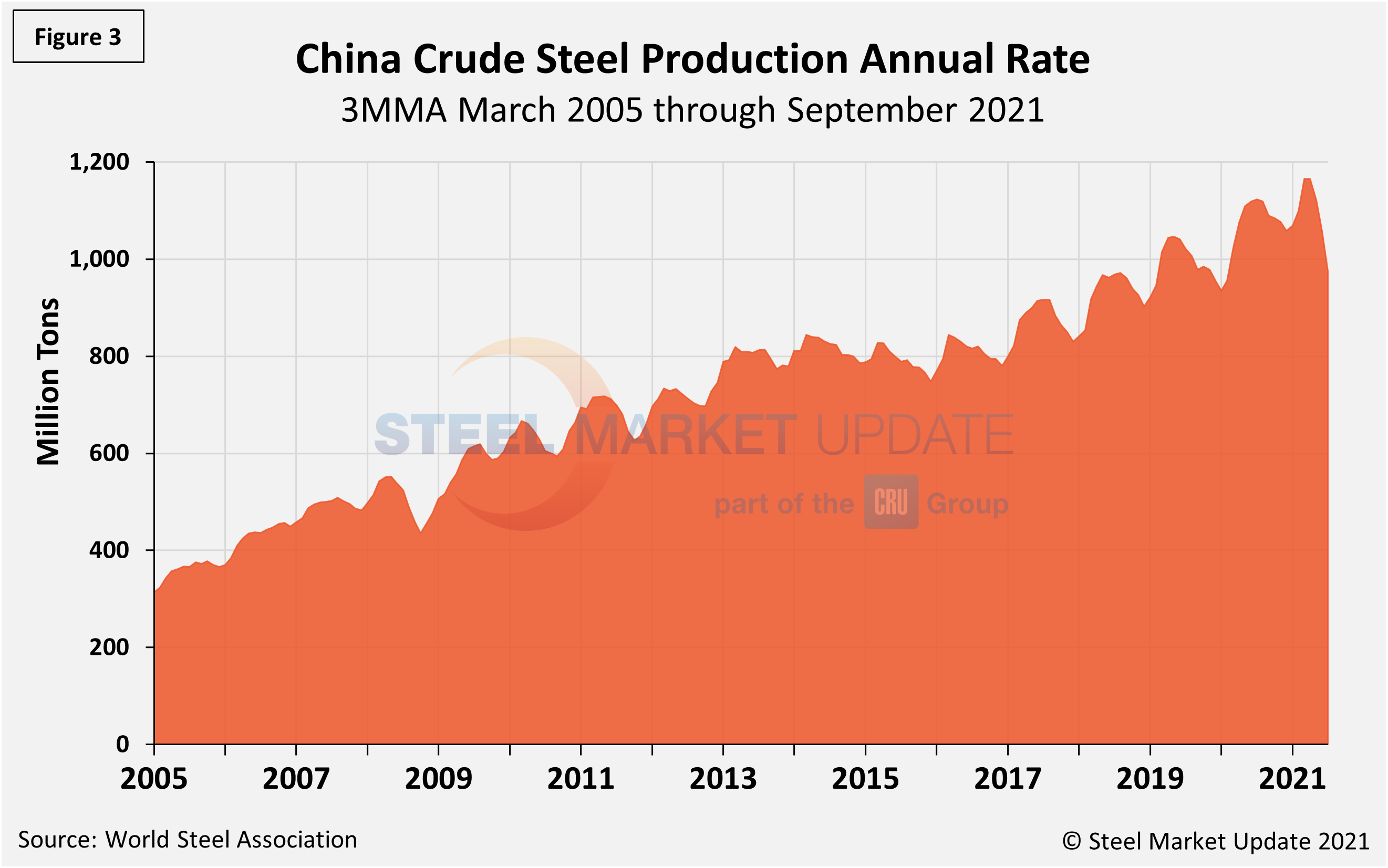

On a 3MMA basis (Figure 3), the annual rate of China’s crude steel production had maxed out at 1.123 billion metric tons in September 2020, then dipped month on month through February. March through May were the first increases since last September, setting a new high of 1.166 billon metric tons in May. September’s total fell to 975.2 million metric tons, slipping again, for the fourth time in as many months. China’s annual capacity is presently 1.128 billion metric tons, and its annual capacity utilization slipped to 95.2% in September, down from its all-time high of 98.4% in June.

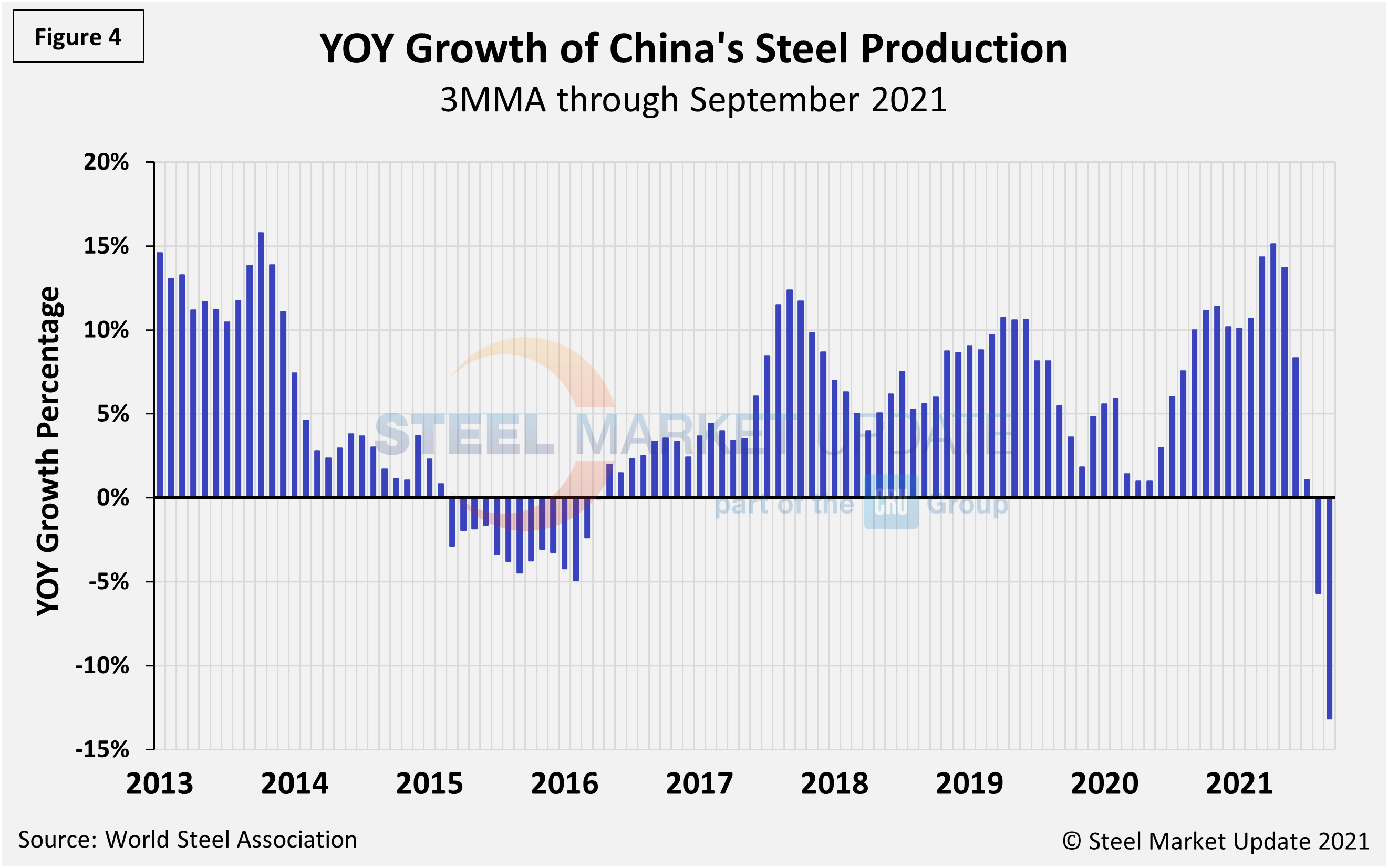

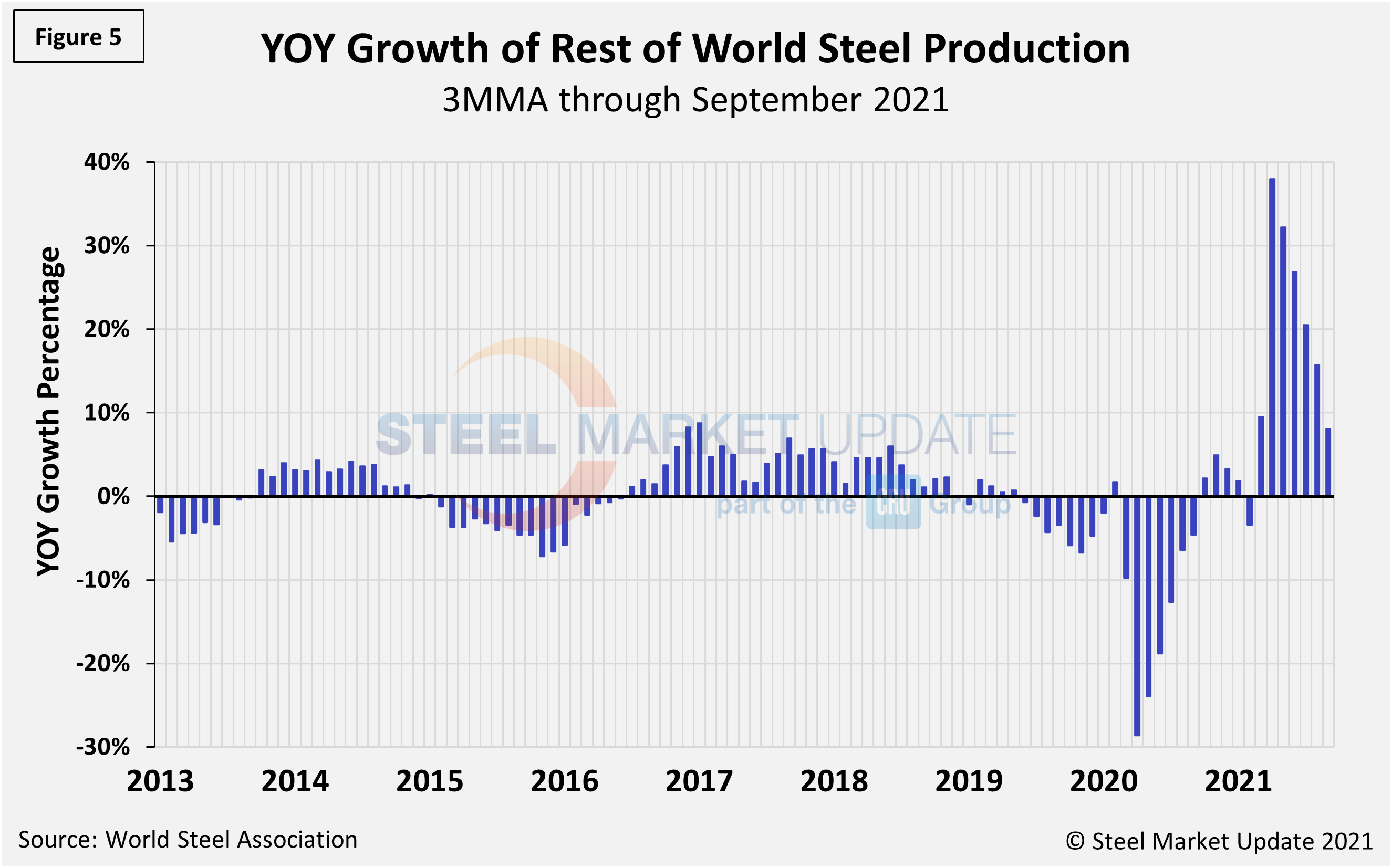

The fluctuations in China’s steel production since April 2013 are shown in Figure 4, while Figure 5 shows the growth of global steel excluding China, both on a 3MMA basis. From November 2020 through September 2021, the rest of the world’s production rose sharply, reaching a peak of 38.0% in April. Since then, the rate for the rest of the world’s annual production has decreased sequentially to just 8.1% in September. China’s annual growth rate was -13.2% in September, a decrease from -5.7% in August, and a complete turn from a high of +15.1% in April. It’s also the first negative growth rate since March 2016. The sharp downturn in steel production continues to be attributable to power shortages resulting from high coal prices and the Chinese government’s efforts to curb harmful air emissions from the steel industry. The trend is expected to continue in the near-to-medium-term.

By David Schollaert, David@SteelMarketUpdate.com