Market Data

March 3, 2022

SMU Survey: Steel Buyers Weigh in on Ukraine, Prices

Written by Tim Triplett

The war in Eastern Europe is hitting close to home for some steel buyers. Steel Market Update’s survey this week asked readers: How might the Russian invasion of Ukraine impact your business? Roughly three out of four of the service center and manufacturing executives who responded said they fear at least some fallout from the conflict overseas on their operations in the U.S.

Most said they expect the supply-chain disruptions and the lost shipments of pig iron and slabs from the two countries to cause shortages of raw materials and add upward pressure to global steel prices. Many are also concerned about the impact on the cost of energy. Following are some of their comments:

“I expect a big impact on raw material items from scrap, iron ore, pig iron and various alloys. The volumes that come from Russia and the Ukraine are substantial and will be disruptive to mills’ input costs.”

“It will create a bit of a panic, with everyone worrying about supply.”

“Lack of pig iron will drive up the cost of prime scrap.”

“It will drive prices up due to sanctions on slabs and bands. It won’t take much for the U.S. mills to use it as an excuse, real or fake!”

“The chaos on the macro level will help support the mills ‘drawing a line in the sand’ around $1,000/ton. Hopefully the invasion gets squashed within the next week by the combination of Ukrainian defiance and NATO/EU/U.S. involvement via harsh(er) sanctions.”

“We are going to see a scramble unfortunately because of Ukraine. God bless those people!”

Bottom in Sight?

These geopolitical factors add currency to the argument that steel prices are near the end of their year-long slide. Up until very recently, prices were dropping by $50 to $100 per ton each week. But $50 price hikes announced by Cleveland-Cliffs and Nucor last week aim to slow that descent.

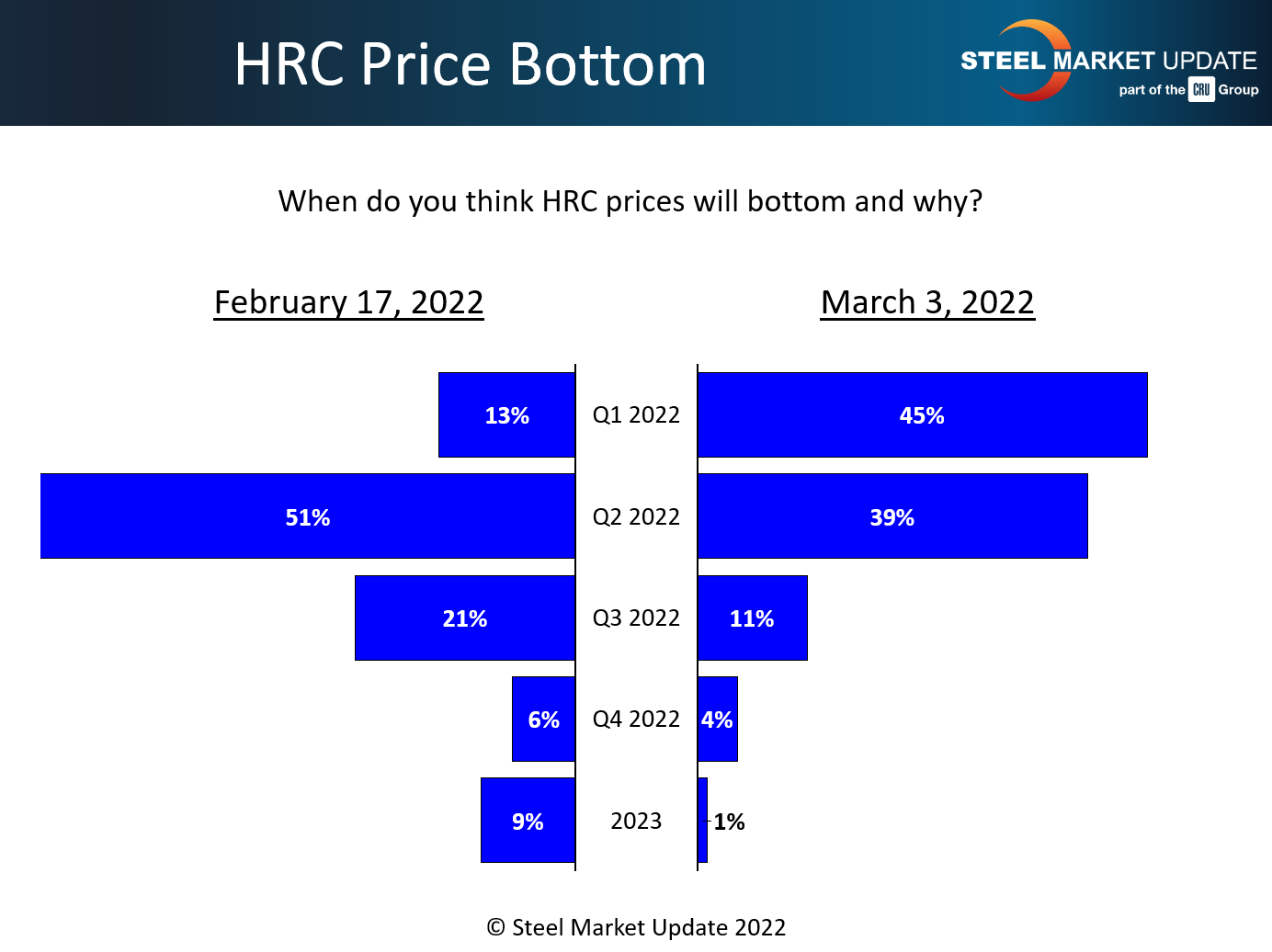

Indeed, 45% of SMU’s survey respondents said they expect the price of hot-rolled coil to bottom out by the end of the first quarter, which is just four weeks from now. Another 39% expect pricing to turn around before the end of Q2. But there’s a persistent minority (of pessimists/realists?) who see HRC continuing to decline well into the second half.

Here’s what a few had to say:

“The market is going up right now. We left the bottom behind already.”

“Prices are likely to be higher two weeks from now.”

“I expect imports to be fewer and fewer and for OEM and service center restocking to start in earnest in the early spring.”

“I have prices stabilizing to even increasing by end March or early April. Stock rebuild is beginning. Imports from most countries are uncompetitive.”

“Uncertainty over the Russian invasion of Ukraine will bring buyers back.”

“The price slide was too abrupt. In unison, the mills will increase prices starting in mid to late March.”

First-Quarter Price Predictions

Steel demand appears to be holding up well, according to SMU survey data. About 88% of recent respondents said demand for their products and services is stable, if not improving.

As recently as mid-January, nearly half of buyers said they were staying on the sidelines, postponing purchases in anticipation of lower prices as they worked down excess inventories. As of this week, there’s lots of elbow room on the sidelines as 83% of respondents called themselves active buyers.

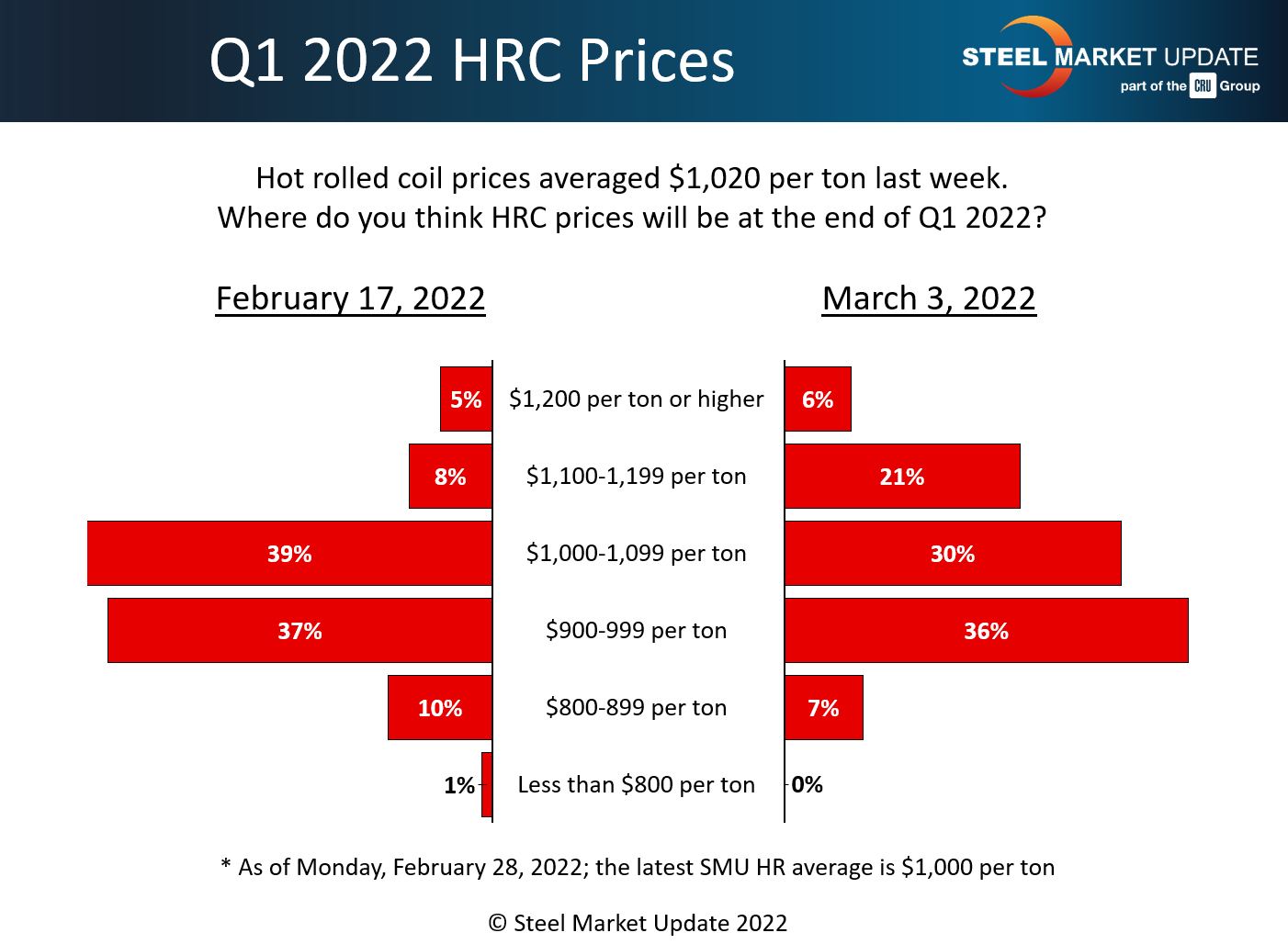

SMU also asked: Where do you think HRC prices will be at the end of the first quarter? About 27% forecast $1,100 tons or higher, while another 30% predicted prices will fall somewhere in the range from $1,000-1,099 per ton. In other words, the majority of survey respondents expect hot rolled prices to be higher than they are today just a few weeks from now. Calculating a weighted average of all the responses puts the average HRC price around $1,030 per ton at the end of March.

As one exec commented: “HRC prices are almost at their bottom for the moment.” Said another: “We are expecting the slide to continue for about 40 more days, but not at the crazy clip we have seen. It has gone down faster and more severely than it went up – which is hard to fathom.” Added a third: “In two weeks, the price will be up over $1,400.”

Those comments serve to illustrate that no one really knows what will happen to steel prices over the coming weeks and months, especially with an unprecedented war in the mix.

By Tim Triplett, Tim@SteelMarketUpdate.com