Prices

May 12, 2022

Ferrous Futures: Rangebound and Itching for a Big Move - Up or Down?

Written by David Feldstein

Editor’s note: SMU Contributor David Feldstein is president of Rock Trading Advisors. Rock provides customers attached to the steel industry with commodity price risk management services and market intelligence. RTA is registered with the National Futures Association as a Commodity Trade Advisor. David has over 20 years of professional trading experience and has been active in the ferrous derivatives space since 2012.

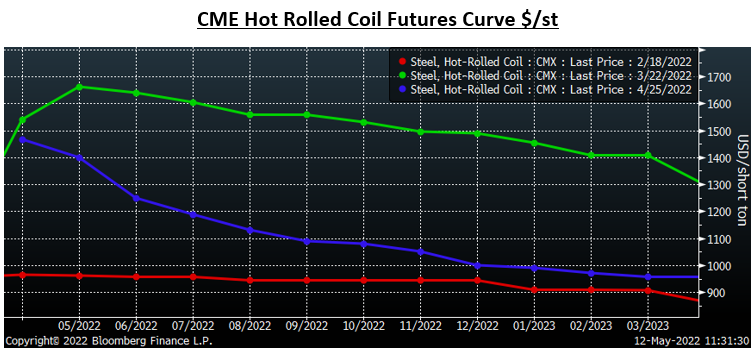

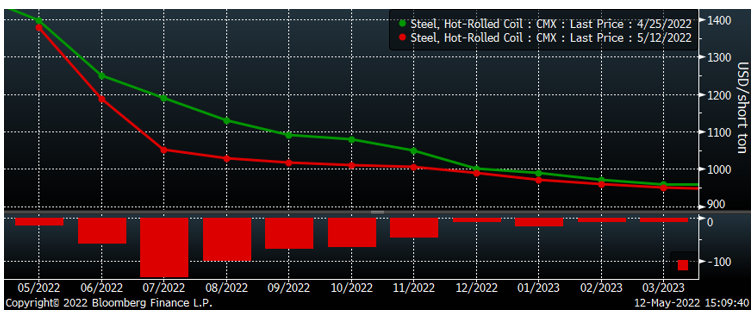

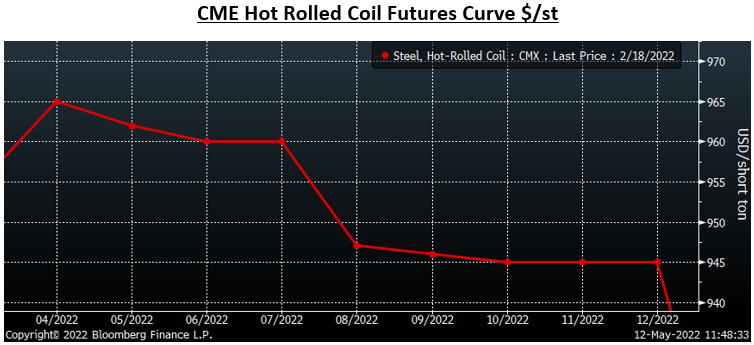

This chart shows the HRC futures curve through March 2023 on Friday February 18, Tuesday March 22, and Monday April 25. February 18 was the Friday before the initial Cleveland-Cliff’s price increase announcement and the Russian invasion of Ukraine. March 22 was the high of the post-invasion short-squeeze rally.

On Monday April 25, the curve fell sharply lower, off $100 to as much as $145 depending on the month, but on light volume (22k tons).

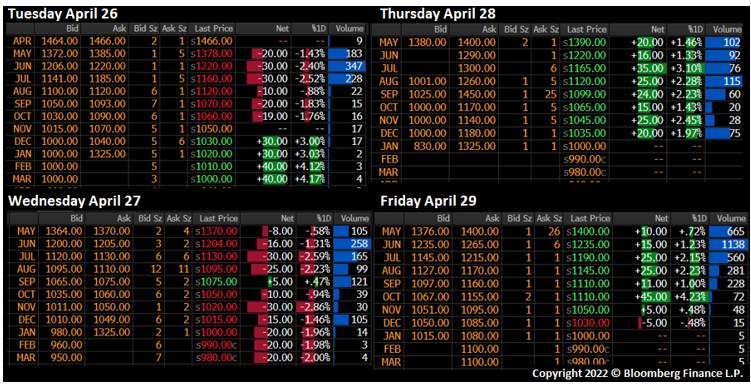

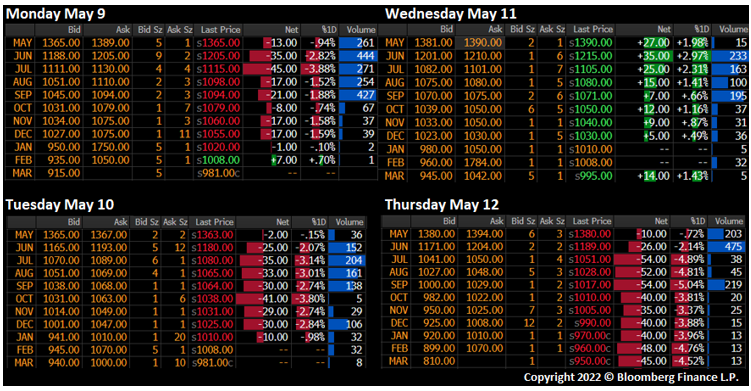

Since April 25, the curve has been directionless and rangebound. The graphics below show each day’s settlements for the rest of that week. The curve was down on Tuesday and Wednesday, but then bounced on Thursday and on Friday.

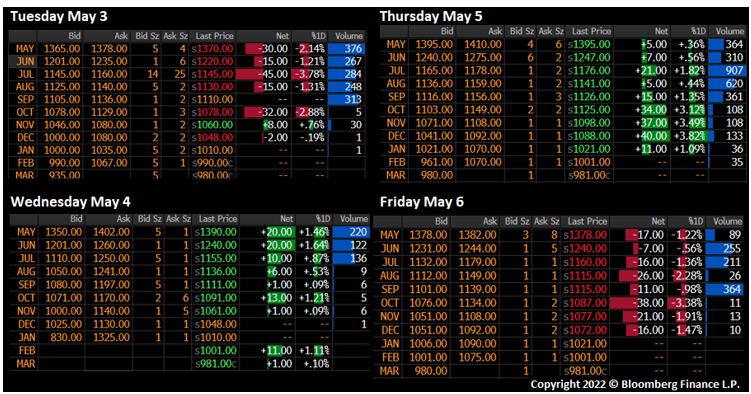

Here are the following week’s settlements. The market was down on Tuesday, up on Wednesday, up on Thursday, and then down on Friday. WoW, the curve was mixed with little change.

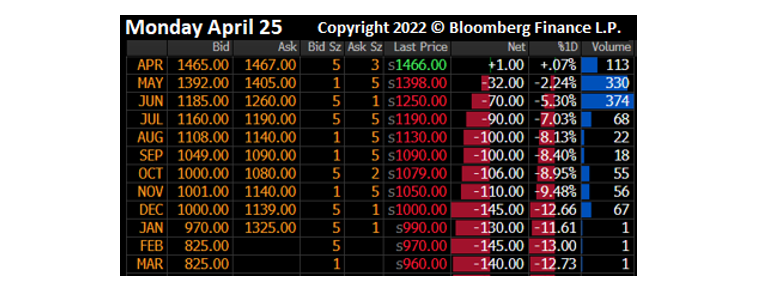

So far this week, the market was down on Monday and Tuesday and then clawed back some losses on Wednesday following the CRU print. Today, there was another round of selling. But like on April 25, it was on light volume with only 21,180 tons trading across the curve. Will buyers come in tomorrow sending the curve back to where it started the week to continue the pattern?

Since April 25, the curve has declined with July and August down the most, $139 and $102, respectively. But the other months’ declines were not as significant. Moreover, the curve flattened. More on this below.

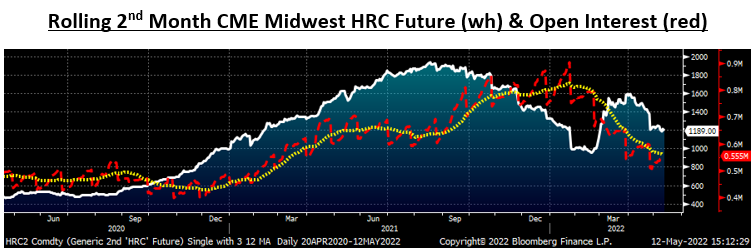

Since peaking at 900k tons, open interest has plummeted, falling to 555k tons as of yesterday. Open interest is the number of open contracts in tons held by market participants.

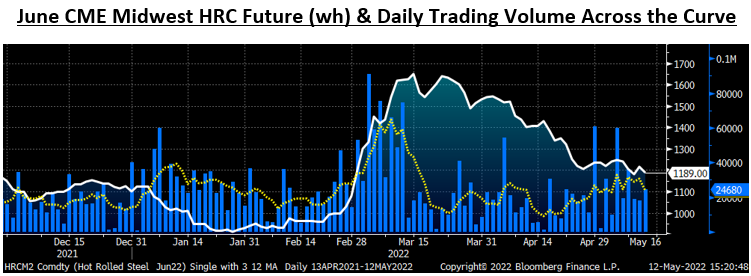

This chart overlays the daily trading volume across the HR curve in blue with a 5-day moving average in yellow. Daily volume exploded in the three-week period following Russia’s escalation in Ukraine, but since has been anemic. As shown above, open interest declined sharply indicating the driver behind the surge in volume was shorts closing out their positions. Those three weeks definitely shook up market participants and the result from that shake up, or shake out, is relatively reduced liquidity. Relatively less liquidity translates into relatively higher volatility as evidenced by the sharp moves on light volume seen on April 25 and again today.

The HRC futures curve shifted from being steeply backwardated in the second half of 2021 to basically flat by February 18, as shown below. Futures fell hard in the first three weeks of January before compressing into a trading range around $950 for the next four weeks. A comparable path has been taken over the past few weeks as shown above with trading remaining directionless and in a range while the curve flattens. Is there a pattern here with the flattening of the curve being analogous to a spring coiling up? Are we in for another sharp move in the weeks ahead as we saw after the curve flattened in late February? If so, in which direction???

Considering the market fundamentals and global macroeconomics, a case can be made that if there was a sharp move in the futures, it would be to the downside. Higher interest rates, falling PMIs, the stock market, Bitcoin, China, the war in Ukraine, I can go on and on.

However, a case can also be made for a sharp rally. (Insert Scooby Doo “WHHHAAAT????” here.) This might sound illogical or crazy to you given the macroeconomic backdrop, but hear me out. Purchasing managers have been holding back placing orders for almost two months following the surge of orders in late February/early March. The heavy ordering back then gave buyers time to hold off. And then with the futures market and now physical indices falling, they have continued to hold off placing orders – expecting the price to be lower tomorrow, next week or next month. Nevertheless, every day that goes by, tons are being consumed across the manufacturing industry, which is chewing through inventory. Without new orders being placed, an accumulated deficit builds while the third quarter is just around the corner. If buyers are in fact collectively holding back orders, then that could lead to another wave of orders similar to what we saw in March 2021 and late February of this year. Moreover, are buyers considering locking forward buys in via the future curve’s backwardated discounts of $350 – $400/st to this week’s CRU print?

It seems to me that steel buyers would almost rather pay $1,200/st than $950/st for hot rolled. This might sound ridiculous, but there is no doubt a herd mentality exists amongst the buying crowd. It seems that once the collective starts buying tons, the rest will follow as if everyone else buying gives them cover – and makes them feel more confident about their decisions. I get it. No one wants to catch the falling knife.

It will be interesting to see if the steady OEM forward buying of the futures curve seen throughout last year and again in March returns. If it does, they will find a relatively less liquid futures market than before; one that may be less than forgiving and quickly rip higher in response to an influx of buy orders.

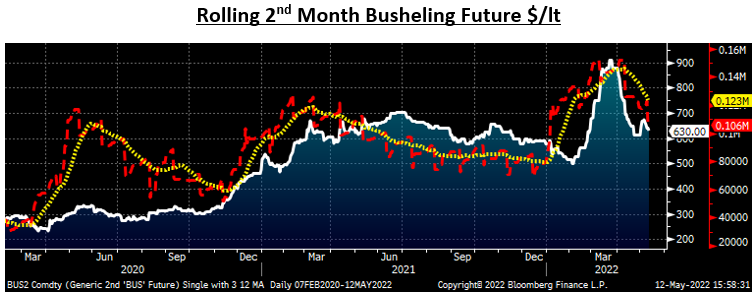

Earlier this week, the May busheling future expired settling down $73.57 MoM to $705.08/lt. Open interest has retreated back to 118k along with the price.

The path of the busheling futures curve has been near identical to that of the HRC futures curve. After February 18, the busheling curve exploded higher eventually trading above $900. Since peaking on March 23, the busheling curve has also watched its meteoric rally rapidly evaporate with the curve falling almost all of the way back to where it started.

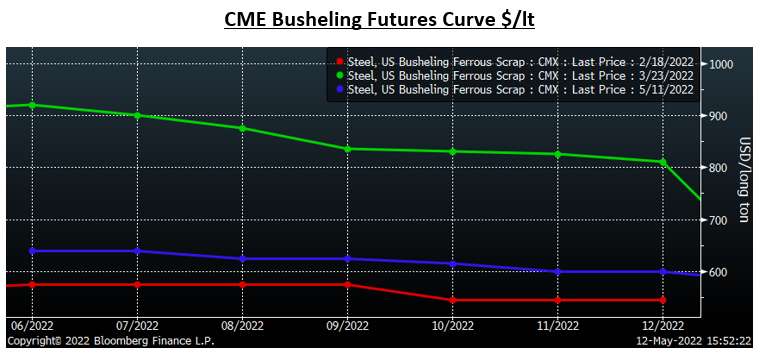

What gives? I thought busheling was the new precious metal? Isn’t EAF demand supposed to outstrip the available prime scrap supply? Wasn’t the war in Ukraine going to block 60% of pig iron imports, leaving domestic EAF mills scrambling for tons? Apparently the mills have been able to acquire plenty of feedstock because AISI production has remained strong at 81.4% capacity utilization while the June busheling future settled today at $630, pricing in another $75 MoM decline. Is this illogical or crazy? Is this ridiculous? No, it’s just the nature of the always interesting and unpredictable steel business. Stay tuned!

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Feldstein should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.