Prices

June 28, 2022

Preliminary Import Data: May In Line With April, June Licenses Down

Written by Brett Linton

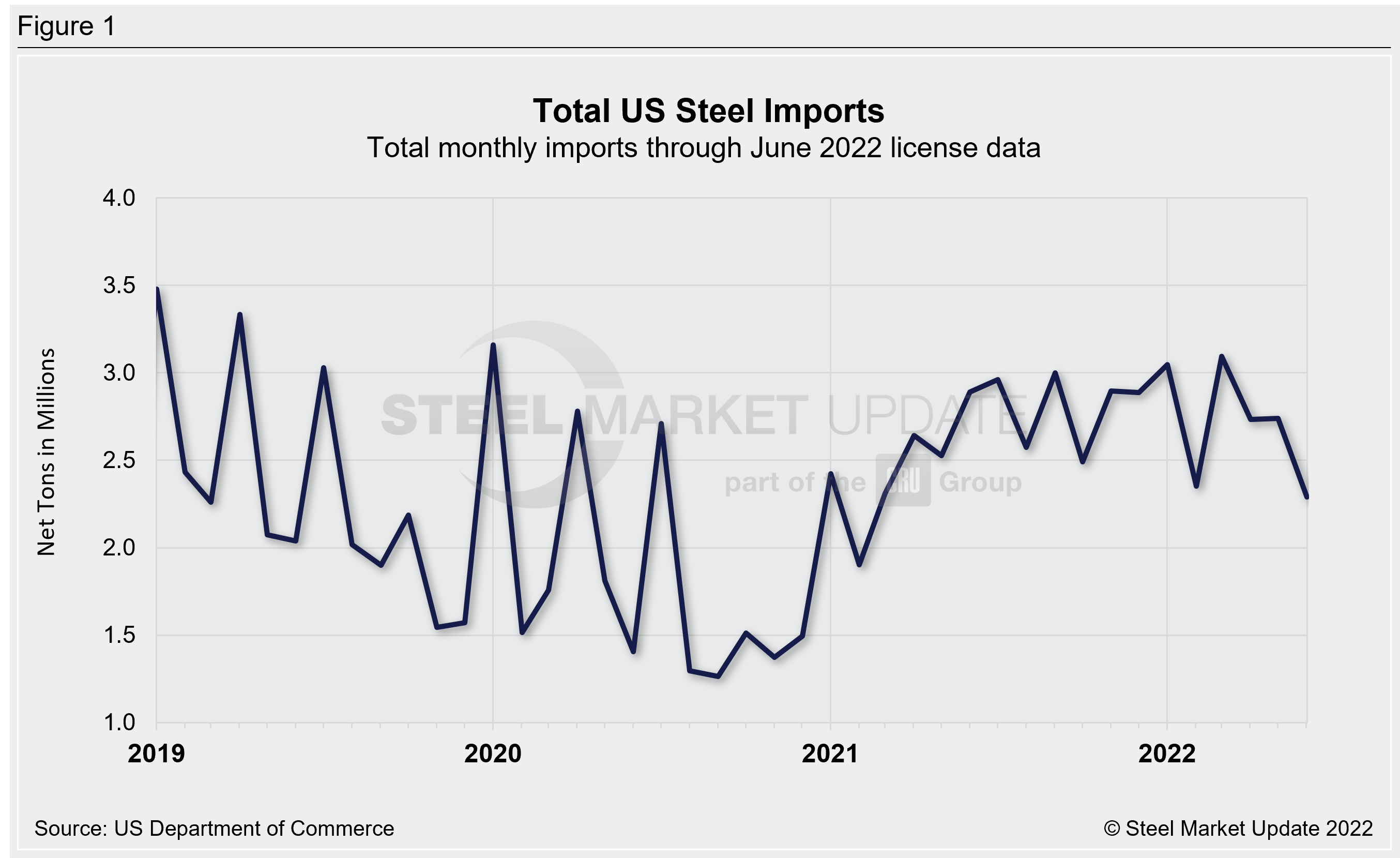

Preliminary Census data shows that steel imports in May currently total 2.74 million net tons, 6,000 tons higher than April, but down 11% from March’s 26-month high of 3.09 million tons. June import licenses are now at 2.29 million tons, 16% less than April and May levels, and potentially the lowest level seen since Feb. 2021.

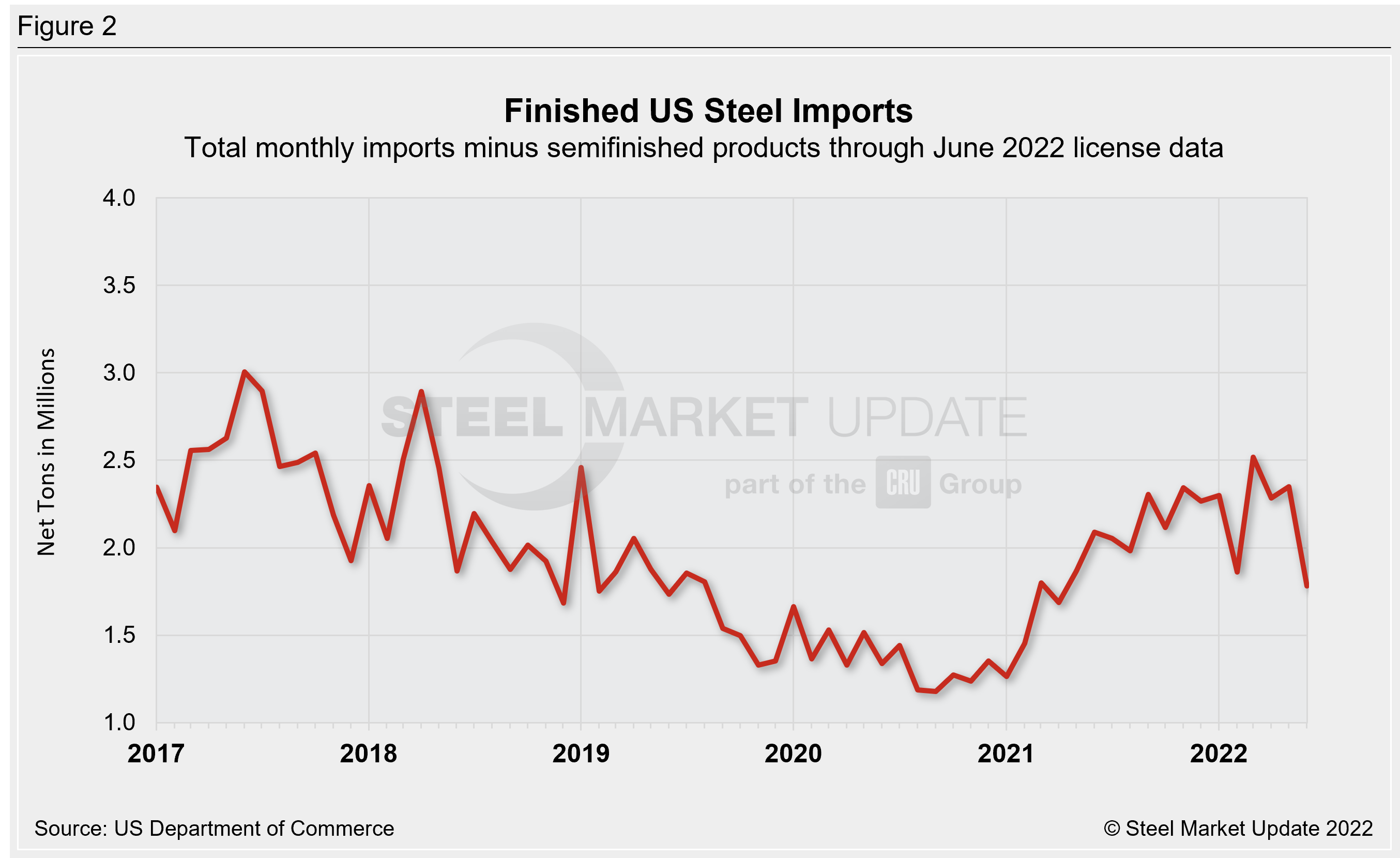

Total finished steel imports are preliminarily at 2.35 million tons in May, 3% higher than April but 7% less than March’s 46-month high. License data shows June finished steel imports are now at 1.78 million tons, potentially the lowest level since April 2021.

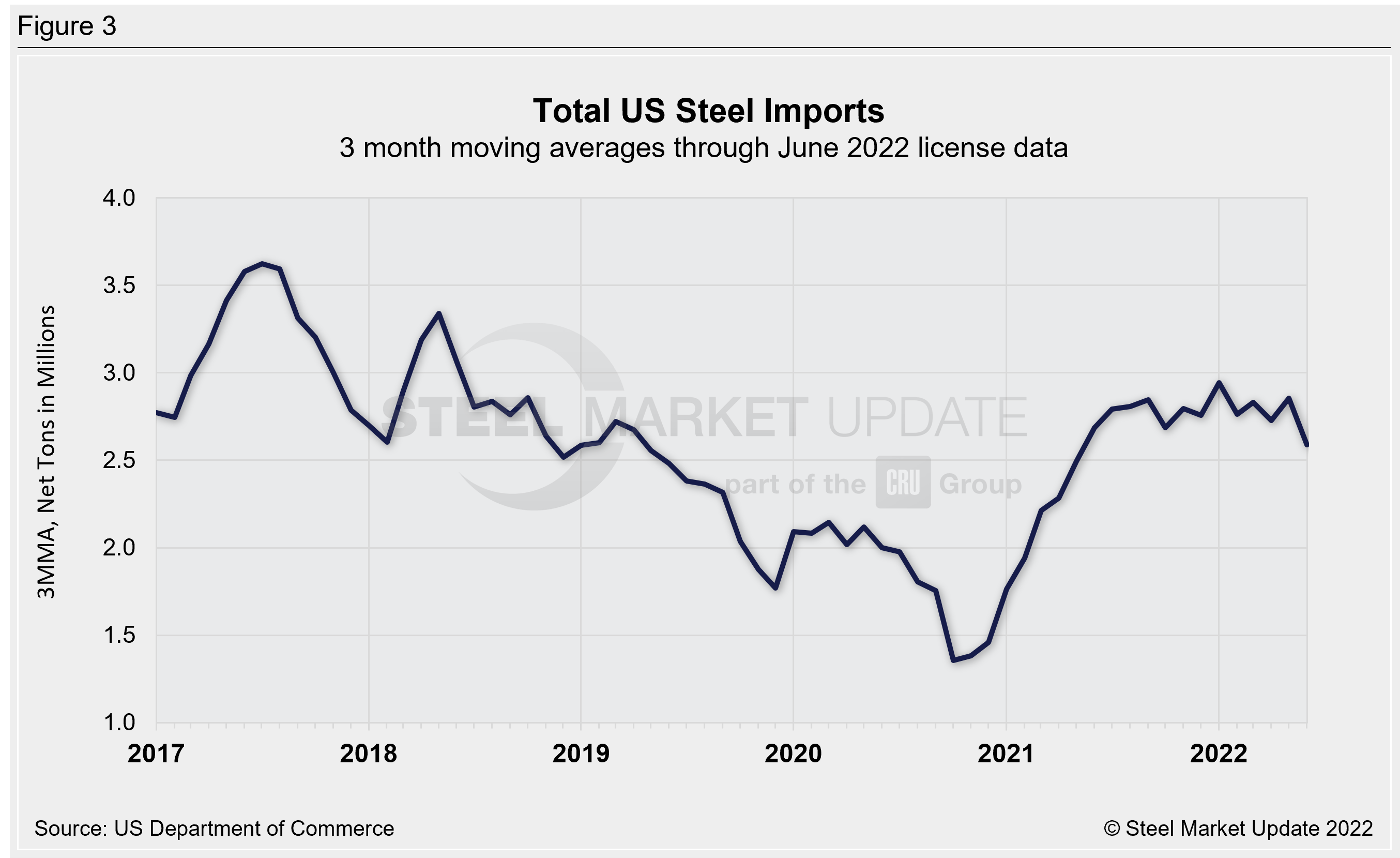

Due to large month-on-month (MoM) swings in semifinished imports, the chart below shows total imports on a three-month moving average (3MMA) basis in an attempt to more accurately display trends. Through preliminary May figures, the 3MMA is up to 2.86 million tons, now the second highest level in the past 3.5 years. Current import levels remain strong compared to recent years: recall 2021 averaged 2.63 million tons per month, 2020 averaged 1.84 million tons per month, 2019 averaged 2.32 million tons per month. In January 2022 the 3MMA had reached a 42-month high of 2.94 million tons. The lowest 3MMA level in SMU’s recent history was October 2020, at 1.36 million tons. The latest June license data suggests that the 3MMA will decline to 2.59 million tons, the lowest level since May 2021.

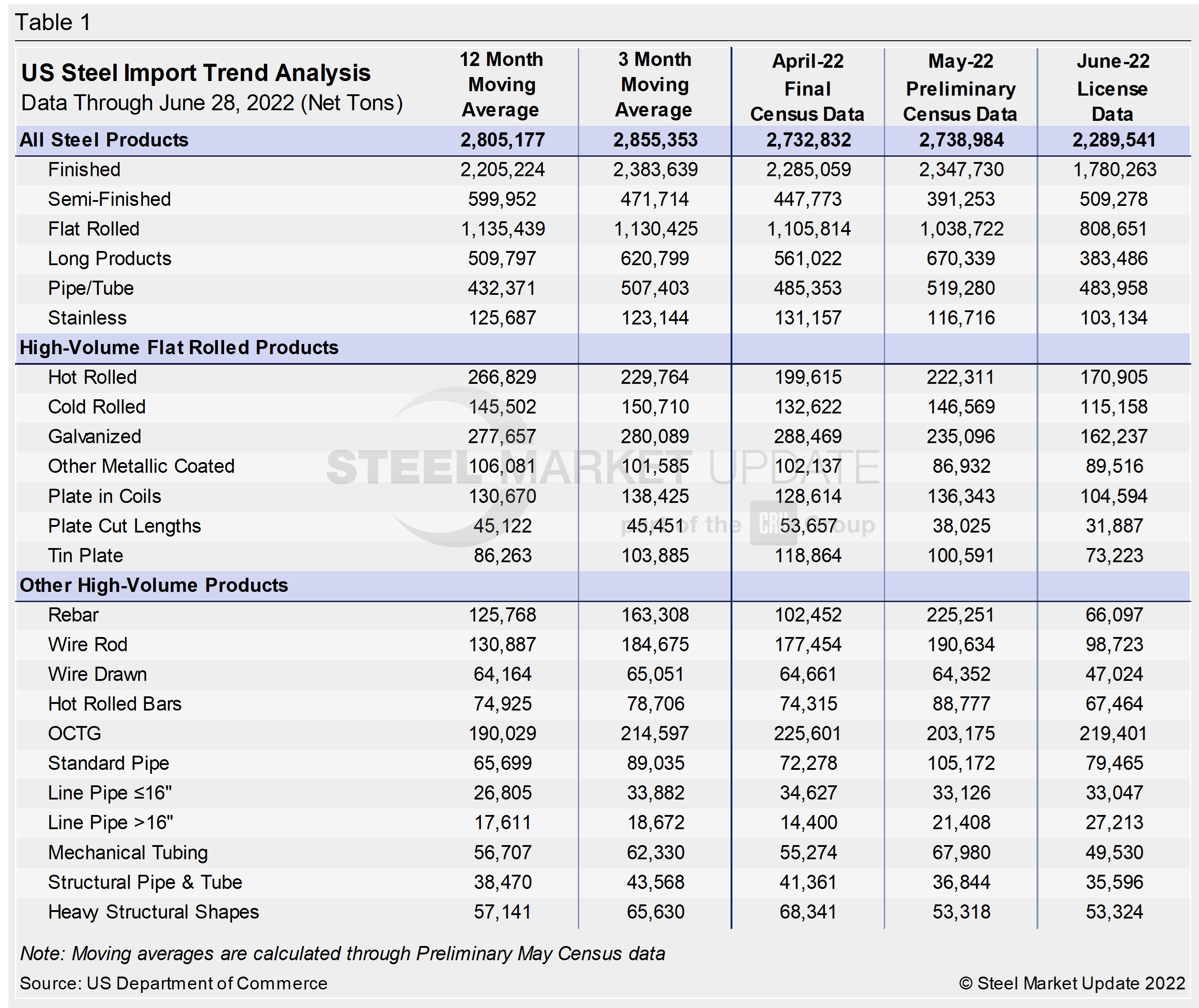

The table below displays flat-rolled product imports as well as other high-volume products, including rebar, tin plate, wire rod, structural pipe and tube, and other long products. We also provide data on imports divided into semifinished, finished, flat rolled, longs, pipe and tube, and stainless products.

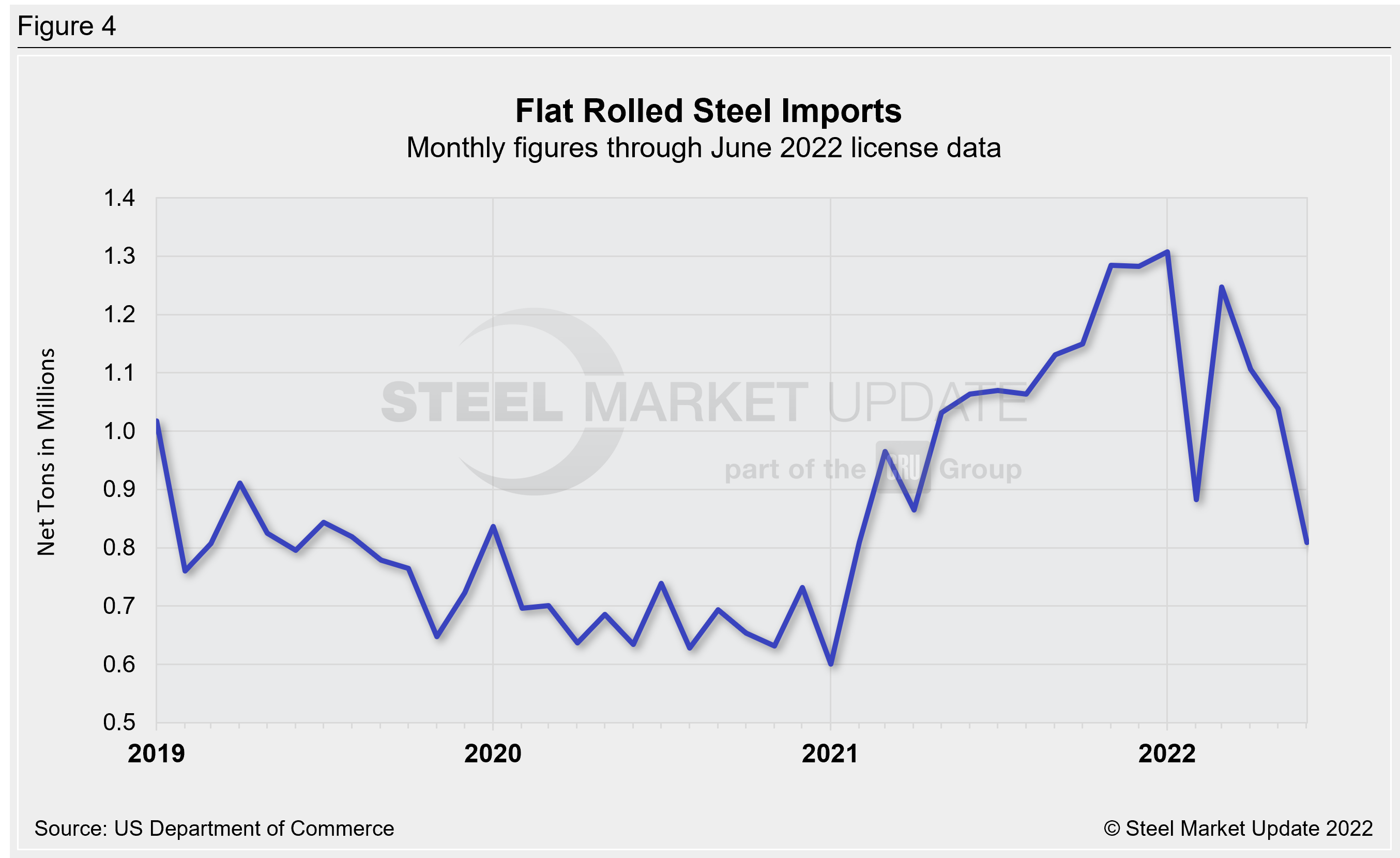

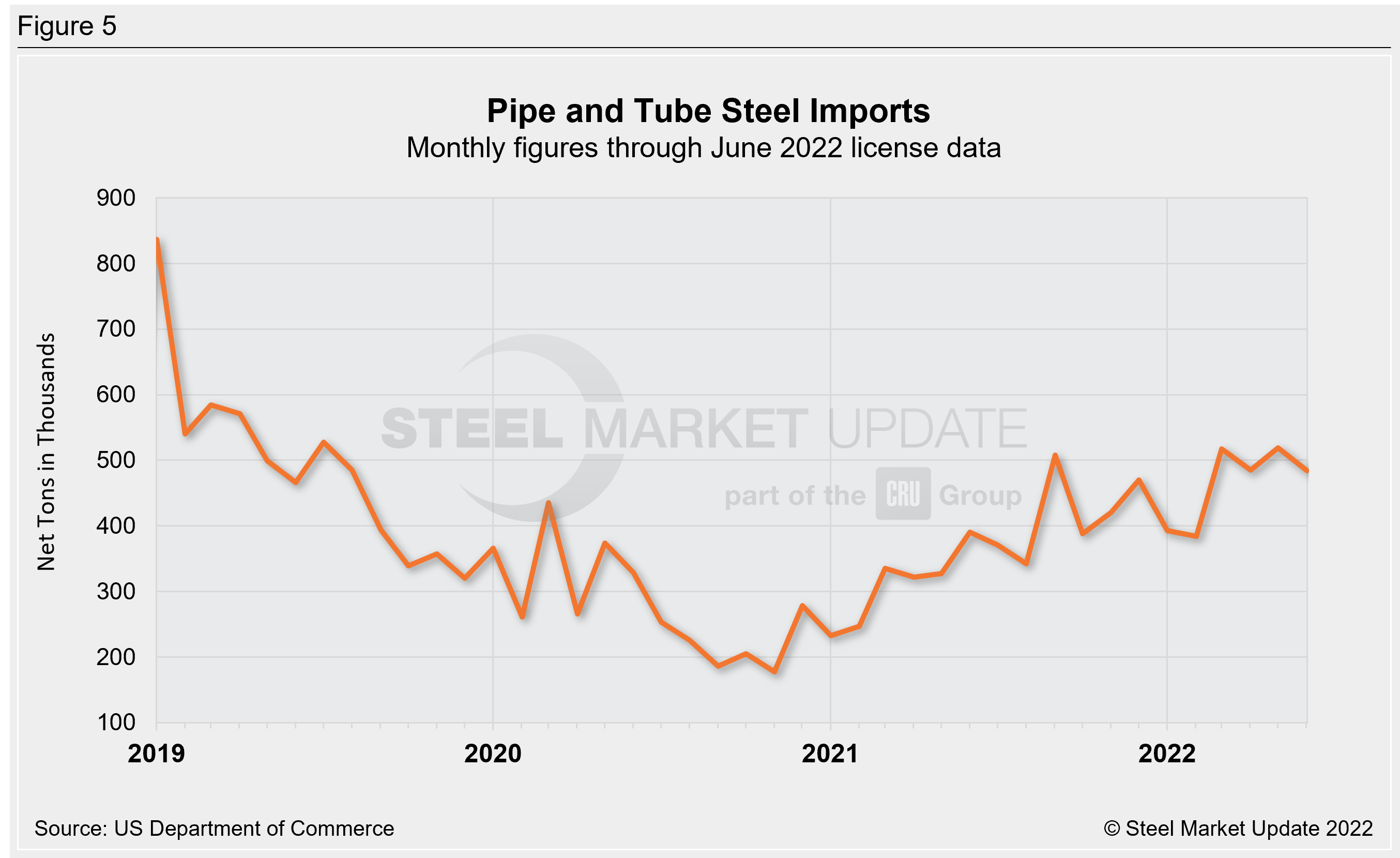

The two charts below show monthly imports grouped by product category: flat-rolled imports and pipe and tube imports. Preliminary May flat rolled-imports eased to 1.04 million tons, down 6% from the month prior. June licenses show a further decline of 22%, with 809,000 tons of flat-rolled imports coming into the country. Pipe and tube imports are expected to be 519,000 tons in May, now at a 2.5-year high. June pipe and tube import licenses are currently down 7% from May to 484,000 tons.

We have an interactive graphing tool available on our website here. Readers can explore historical import data, in total and by product. If you need assistance logging into or navigating the website, contact us at Info@SteelMarketUpdate.com.

By Brett Linton, Brett@SteelMarketUpdate.com