Prices

September 8, 2022

HRC Futures: Post Wednesday CRU Print Rally Picks Up Steam

Written by David Feldstein

Editor’s note: SMU Contributor David Feldstein is president of Rock Trading Advisors. Rock provides customers attached to the steel industry with commodity price risk management services and market intelligence. RTA is registered with the National Futures Association as a Commodity Trade Advisor. David has over 20 years of professional trading experience and has been active in the ferrous derivatives space since 2012.

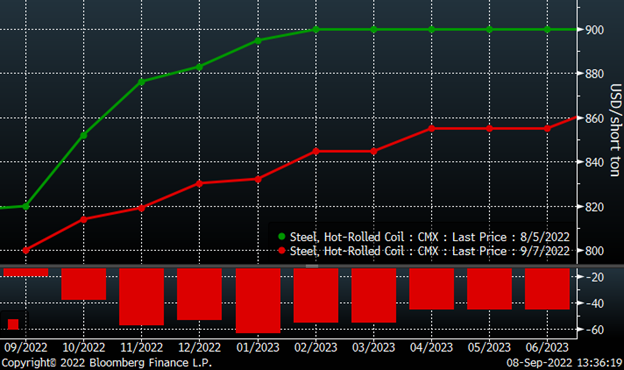

Nucor announced a $50-per-ton flat-rolled price increase on Monday, August 8. This chart shows the CME Midwest HRC futures curve settlements on Friday August 5, the day before the increase, and as of Wednesday night. In the days following the announcement, there was a brief, $30-$50/ton burst higher across the futures curve. But there was no follow through, and the rally failed. In the bottom panel, you can see the HRC futures curve had declined $40-$60/ton per month through Wednesday’s settlement. You could say the price increase was ineffective. You could also say the price increase was simply meant to set the floor.

CME Hot Rolled Coil Futures Curve $/st

Then Cleveland-Cliffs announced a $75/ton flat-rolled price increase on August 25, and NLMK USA followed with a $75/ton price increase the day after. But still the futures sank further. Last week, news of planned outages at various domestic furnaces made the rounds. Then there is the USW contract expiration. And while US Steel and the USW continue forward without a contract, there is some serious assymetric upside price risk if there were to be any kind of disruption.

And that’s not specific to the US. There were ArcelorMittal’s announcements that they were shutting down blast furnaces across Europe along with other European steelmakers. And let’s not forget the typhoon that hit South Korea’s southern coast Tuesday, forcing Posco to suspend operations at three of its blast furnaces at its Pohang facility, which produced 16.85m tons in ’21. This is another instance of a string of market tightening events clustered in a short period. This clustering of events happened in the winter of 2014 and again starting in August 2020. Massive rallies followed both of those instances.

US consumer sentiment has been dreadful while the stock market’s sell-off that started in June weighed on overall sentiment over the summer. “The recession is coming” rang out throughout July. But then there was a shift in August to “maybe things aren’t as bad as feared.” Since August 1, there have been two better-than-expected ISM Manufacturing and Services PMIs, two incredible US employment reports, a better-than-expected inflation report, and a bounce in consumer confidence.

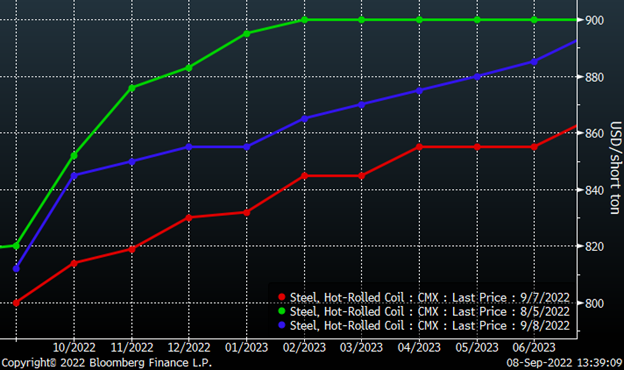

As the industry returns from Labor Day and firms start to pull together their forecasts/budgets for ’23, will forward buying start to emerge in the futures market? Since Wednesday’s +$25 CRU print, the futures have caught a bid. Yesterday, the curve gained $20-$25/ton in the front months on light volume. Today, the volume came through with the curve gaining $20-$30/ton per month.

Revisiting the curves from above, the moves over the past two days have clawed back a decent chunk of the decline seen over the last month. How can that be?

CME Hot Rolled Coil Futures Curve $/st

Open interest, the number of outstanding futures contracts, or tons in this case, has plummeted to 413,000 as of last night. This is the lowest open interest has been since December 2020.

Rolling 2nd Month CME Hot Rolled Coil Future $/st & Open Interest

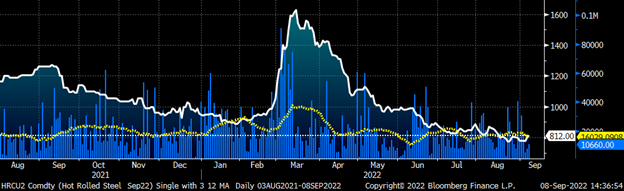

Daily trading volume across the curve has also been sluggish. In the chart of the September future below, the blue vertical lines show the daily trading volume across the curve, while the yellow dotted line is the 22-day moving average of the volume. The white dotted line is at 16,000 tons, yesterday’s 22-day moving average, to show current daily trading volume plumbing the lows seen over the past few years.

September CME HRC Future $/st w Aggregate Curve Volume & 22-Day Avg.

From a trading standpoint, this data tells us there is a relatively low level of liquidity in the market. That means if a surge of volume were to enter the market and there was an imbalance in said surge (i.e., to the sell-side or buy-side), then a sharp price move should result. Today, we saw a small wave of buying across the curve that pushed it up $20-$30/ton per month. If more buyers, especially forward-looking OEM buyers seeking to fix prices for instance, were to enter the market, then we could see a rapid move higher in the futures curve. Perhaps back to the $100/ton weekly moves seen in the first half of the year.

Perception is reality. If the US manufacturing economy performs at a “maybe things aren’t so bad” rate instead of a “the recession is coming” rate, then will we see upward revisions to tonnage forecasts? It’s a tricky moment as domestic supply appears to be “sneaky tight” with inventory at average levels, tons on-order with the mills ultra-low levels, and imports in steep decline. How will ’22 end?

At the 2020 SMU Steel Summit, most participants in a live poll predicted that HRC prices would below $550 per ton the following August. The HRC price in August 2021 turned out to be $1,900. At the 2021 Summit, most voted for above $1,000 and it was $790 this year’s conference. This year, most voted HRC prices next August would be between $700 and $999, so we know, with certainty, it will be either below $700 or above $1,000 by next summer. So at least we got that going for us, “which is nice.”

Can somebody from the mill flat-rolled department call over to the scrap-buying department and tell them to stop negotiating so hard with the scrap yards? We’re trying to get a price increase through over here, and it doesn’t exactly make the buyers feel all warm and fuzzy when they see scrap prices down $20-$40/ton! After four straight down months, how about a nice flat MoM? Go work on your golf swing or fantasy football team. It’s the winners curse folks. In busheling futures, we’re seeing a resurgence of open interest and a continued downtrend in price. Not a good look for higher busheling prices. But they do have had to contend with weak iron ore and Turkish scrap prices along with China’s zero-COVID policy and property market weighing on commodities.

Rolling 2nd Month CME Busheling Future $/lt & Open Interest (red)

The North European futures have been rallying over the past two weeks, gaining $90/ton as the furnace shutdowns refered to above roll out. Do you hear the echoes from Q4 2020? Since March of 2020, massive volatility and price swings in flat rolled as well as a challenging, almost impossible, forecasting atmosphere have been among the few consistent factors.

Rolling 2nd Month North European HRC Future $/st

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Feldstein should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.

By David Feldstein, Rock Trading Advisors