Prices

September 18, 2022

Hot Rolled vs Scrap Price Spread Inching Back Up

Written by Brett Linton

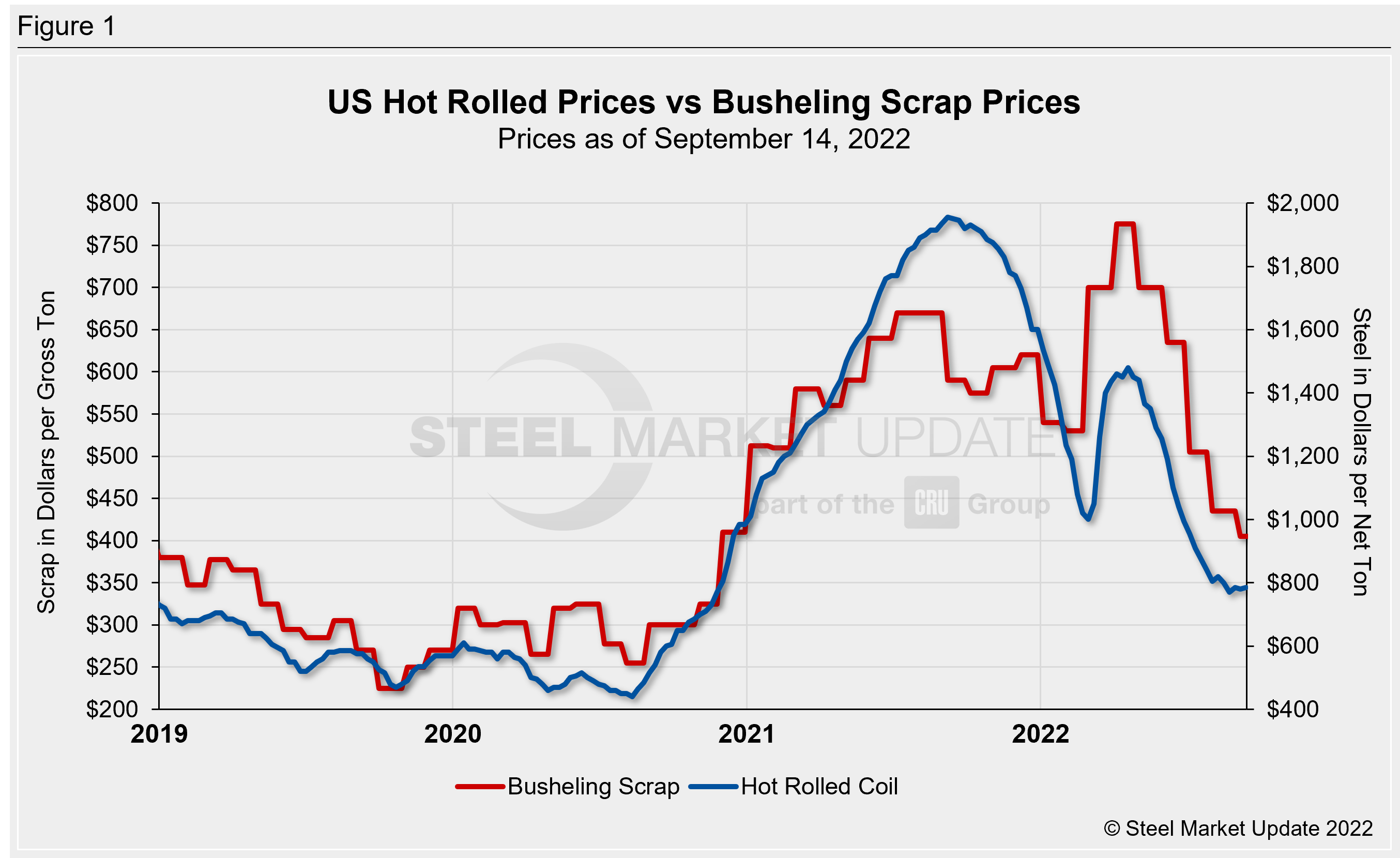

The spread between hot-rolled coil (HRC) and prime scrap prices has changed course in recent weeks, according to Steel Market Update data. Busheling scrap prices declined for the fifth consecutive month in September, while hot-rolled prices have levelled out in recent weeks. Overall, we had seen a shrinking delta between the two products from May through August. After flattening in the last month, the spread has now begun to inch up again. The latest spread is less than one-third what it was this time last year, but it is still higher than pre-pandemic levels.

Our hot rolled coil price average rose $5 per ton last week to $785 per net ton ($39.25 per cwt). HRC prices have increased $15 per ton in the previous four weeks but are down $750 per ton since the start of the year. Prices are also down $1,165 per ton versus levels one year prior. Recall our HRC price peaked around this time last year at $1,955 per ton.

Busheling scrap prices settled last week at $405 per gross ton for September, down $30 per ton compared to August and down $135 per ton from the beginning of the year. August busheling prices are down $370 per ton from April’s historic high, and down $185 per ton versus one year ago. Prior to this year, the previous high for busheling scrap was $670 per ton in July and August 2021. Figure 1 shows price histories for each product.

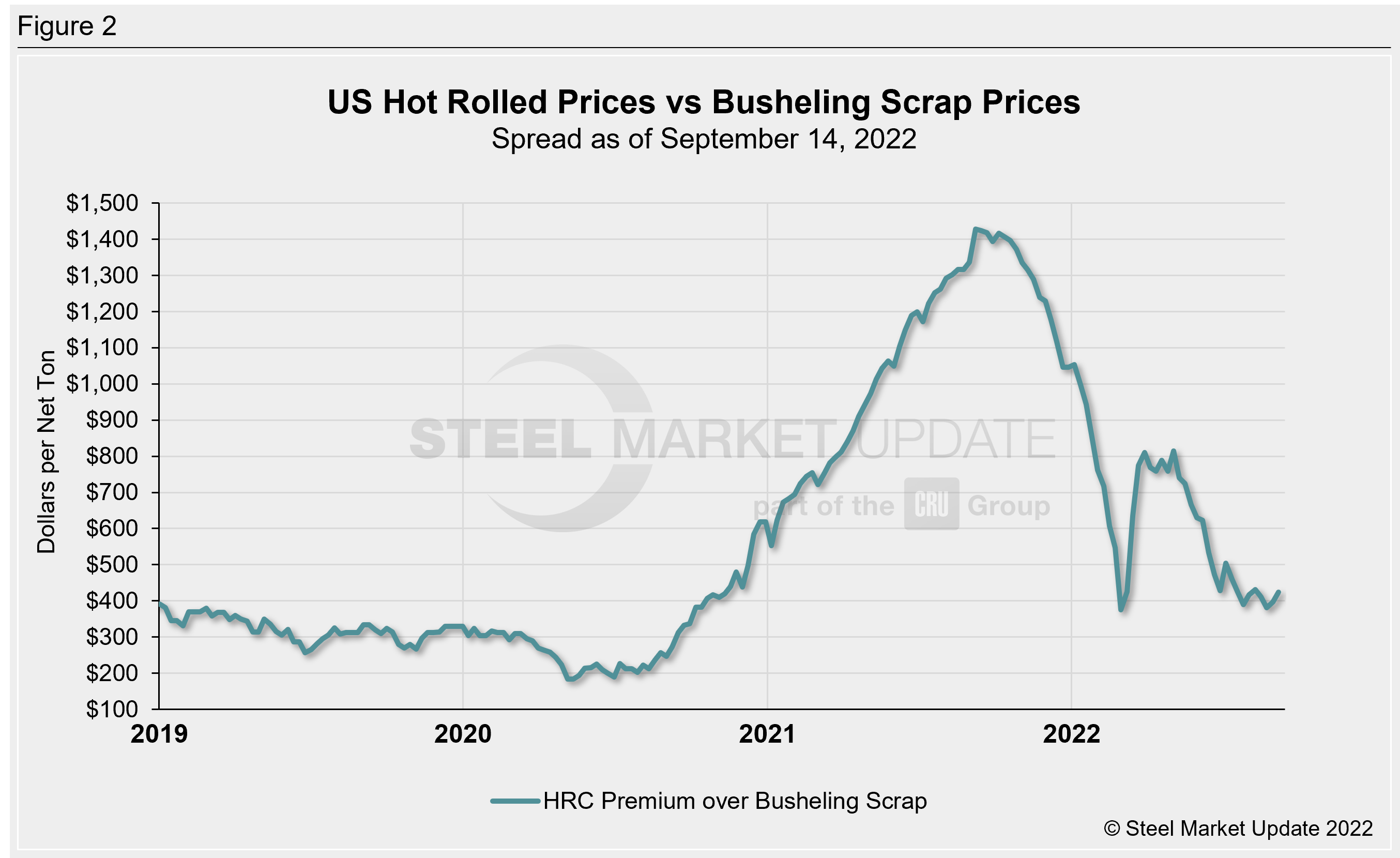

After converting scrap prices to dollars per net ton for an equalized comparison, the differential between hot-rolled coil and busheling scrap prices is $418 per net ton. This is the highest spread seen in the last month, but one of the smaller spreads seen in recent years (Figure 2). In mid August, we saw a spread of $382, the second smallest figure seen since October 2020. The HRC/scrap price spread has averaged $402 per ton over the last four weeks and $436 per ton over the past quarter. Recall that the spread between these two products has been erratic since late 2020. It reached a record-high of $1,428 per ton in September 2021 and fell to an 18-month low of $375 per ton six months later. For comparison, the average spread throughout 2021 was $1,080 per ton, with 2020 averaging $310 per ton and 2019 averaging $324 per ton.

PSA: Did you know our Interactive Pricing Tool has the capability to show steel and scrap prices in dollars per net ton, dollars per metric ton, and dollars per gross ton?

Figure 3 explores this relationship in a different way – we have graphed the spread between hot-rolled coil and busheling scrap prices as a percentage premium over scrap prices. HRC prices now carry a 93% premium over prime scrap, the highest premium seen in the last four months. Over the past four weeks, the premium averaged 83%. Back in early March, the premium reached a multi-year low of 43%, having fallen from a record high 236% premium last October. The same month one year ago, HRC held an average premium of 231% over scrap, while September 2020 saw an average premium of 89%. HRC held the lowest premium over busheling scrap back in November 2011, when it reached 29%.

This comparison was inspired by reader suggestions; if you would like to chime in with topics you want us to explore, reach out to our team at News@SteelMarketUpdate.com.

By Brett Linton, Brett@SteelMarketUpdate.com