Plate

October 17, 2022

August Import Share of US Sheet and Plate Markets

Written by David Schollaert

Imported sheet and plate products arrived at US ports at a slower clip in August, resulting in them accounting for a lower share of the domestic market for the second straight month, according to a Steel Market Update analysis of import data from the US Commerce Department and domestic shipment figures from the American Iron and Steel Institute.

Imports’ share of US sheet and plate markets recent peak was in December, with sheet reaching its highest level in the past 4.5 years. The trend was driven by the need for buyers to find relief from inflated domestic steel prices. As the market slowed at year-end, so did imports. Since then, the arrival of foreign material has ebbed and flowed. August’s were down again after June’s were a most recent high.

Imports’ share of total sheet shipments in the US was 17% in August, down from 17.5% in July. The decline was driven by a 3% decrease in foreign sheet while domestic shipments were largely unchanged at just 0.5% above July’s total. The market share of plate product imports also dipped in August, to 20.1% from 22.1% the month prior.

August’s sheet imports totaled 806,871 tons, down from 832,243 tons in July. Overall sheet product shipments (domestic shipments plus imports) were nearly unchanged in August, just 0.1% below July’s total. They totaled 4.749 million tons in August, down from 4.755 million tons in July, and were driven by a 25,372-ton decrease in foreign sheet while domestic shipments were sideways.

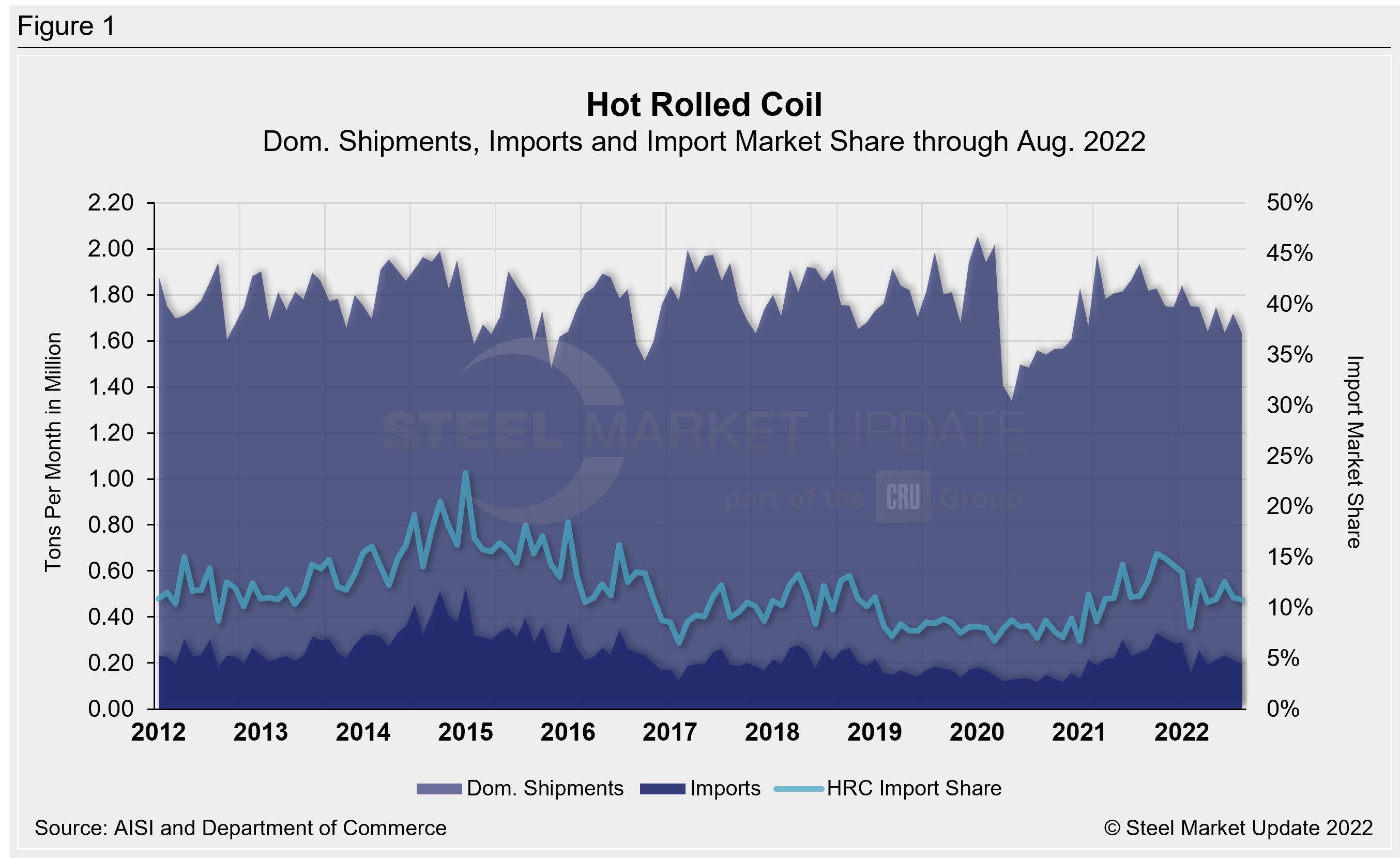

Hot-rolled coil (HRC) imports edged down 7% month-on-month (MoM) in August, totaling 198,062 tons versus 213,013 tons in July. Domestic shipments of HRC were down 5% or 85,874 tons less MoM. The details are below in Figure 1.

The import share of HRC fell 0.2 percentage points to 10.8% in August — still a historically healthy share but below the recent high of 15.3% set last October. The decreased share was driven by a MoM decline in both domestic shipments and in foreign material. HRC apparent supply totaled 1.83 million tons in August, down from 1.93 million tons the month prior.

Imports of galvanized (hot dipped and electrolytic) were down 16.4% in August, while cold-rolled coil (CRC) rose 18.5% in July, and other metallic coat (OMC) increased by 12.8% MoM.

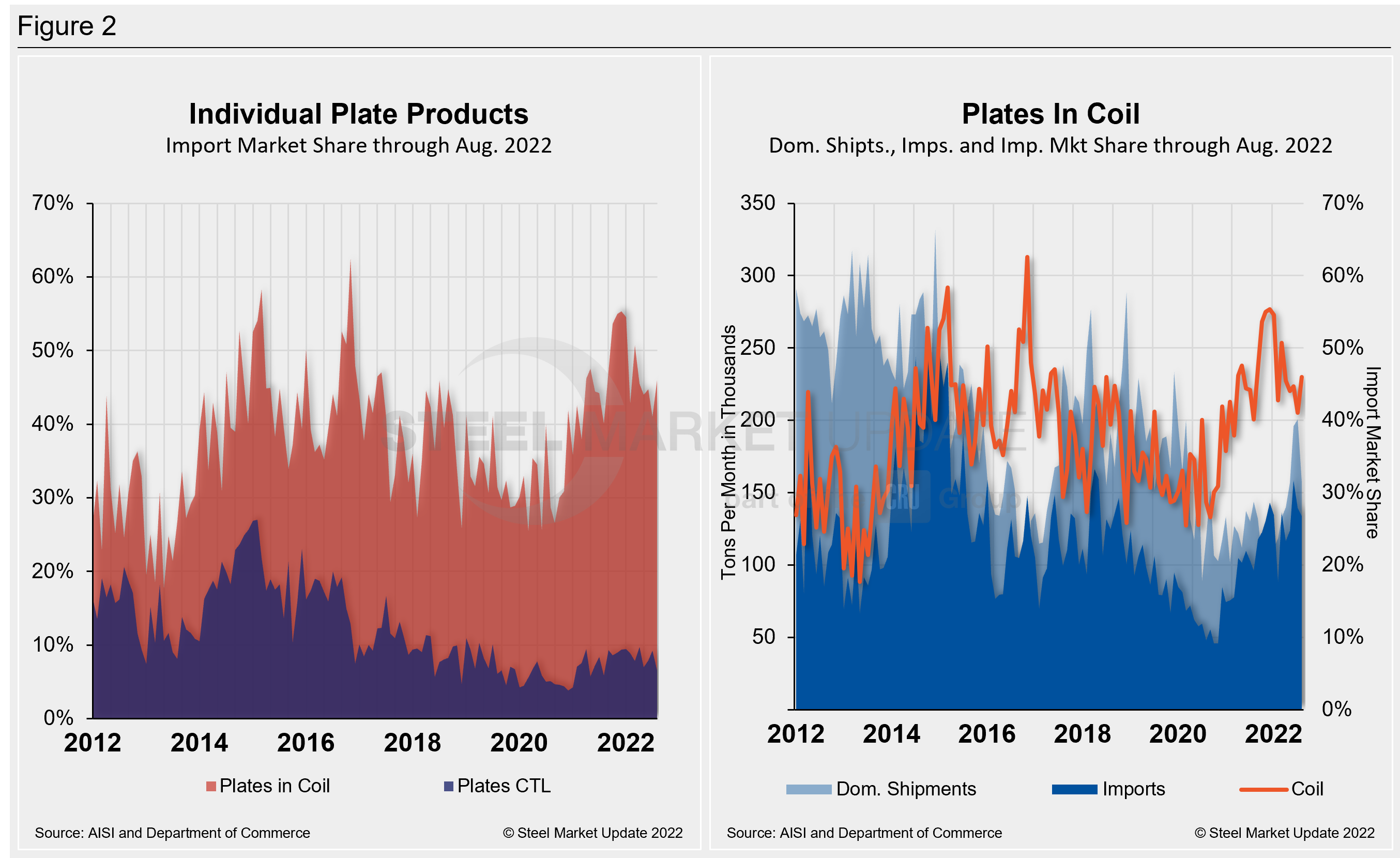

Plate products in August saw an overall decrease in shipments as apparent supply slipped by 0.8% MoM. The decrease was driven by a decline of 8.3% in plate imports, while domestic shipments were up just 3.4% MoM. Despite the decline, plate imports were still the fourth highest YTD at 170,566 tons.

All told, total plate shipments, including foreign and domestic, were 849,139 tons in August, up from 842,379 tons the month prior.

The import market share for plates in coil rose to 45.9% in August, a 4.9 percentage point gain MoM. The increase in market share was driven by a 21.5% dip in domestic shipments, even though imports edged down 4.1% MoM. Total imports of plates in coil were 133,696 tons in August, down from July’s 139,391 tons.

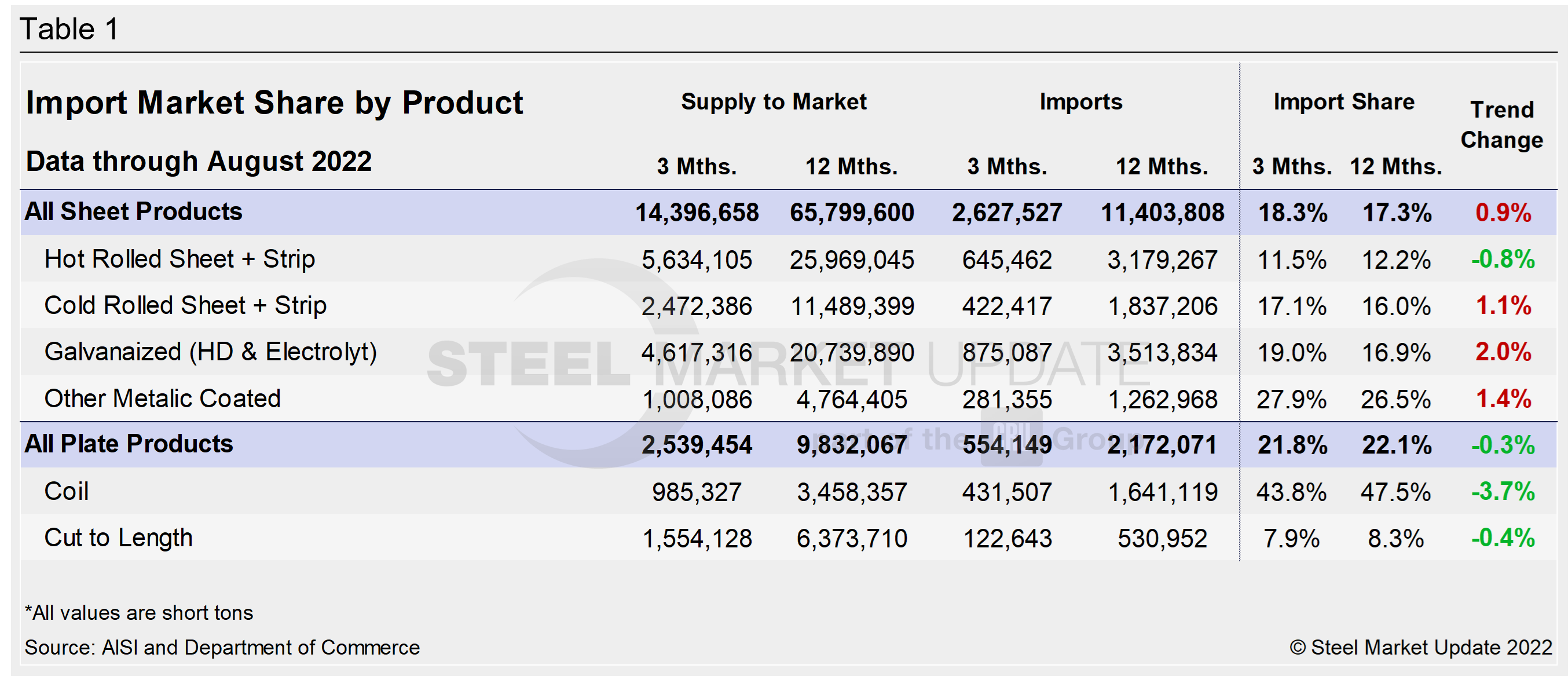

The table below displays the total supply to the market in three months and 12 months through August 2022 for sheet and plate products and six subcategories. Supply to the market is the total of domestic mill shipments plus imports. It shows imports on the same three- and 12-month basis and then calculates import market share for the two time periods for six products. Finally, it subtracts the 12-month share from the three-month share and color codes the resulting green or red according to gains or losses. If the result is positive, it means that the import share is increasing, and the code is red.

The big picture is that imports’ share of US sheet sales grew in August while plate declined. The big second-half jump in total imports in 2021 was the result of historically and disproportionately high domestic steel prices. The influx of foreign material had been declining, coinciding with lower domestic prices. The war in Ukraine shifted that dynamic temporarily, pushing prices higher, and foreign steel quickly arrived at US ports again. Now that prices have declined at a rapid pace, imports have become more balanced.

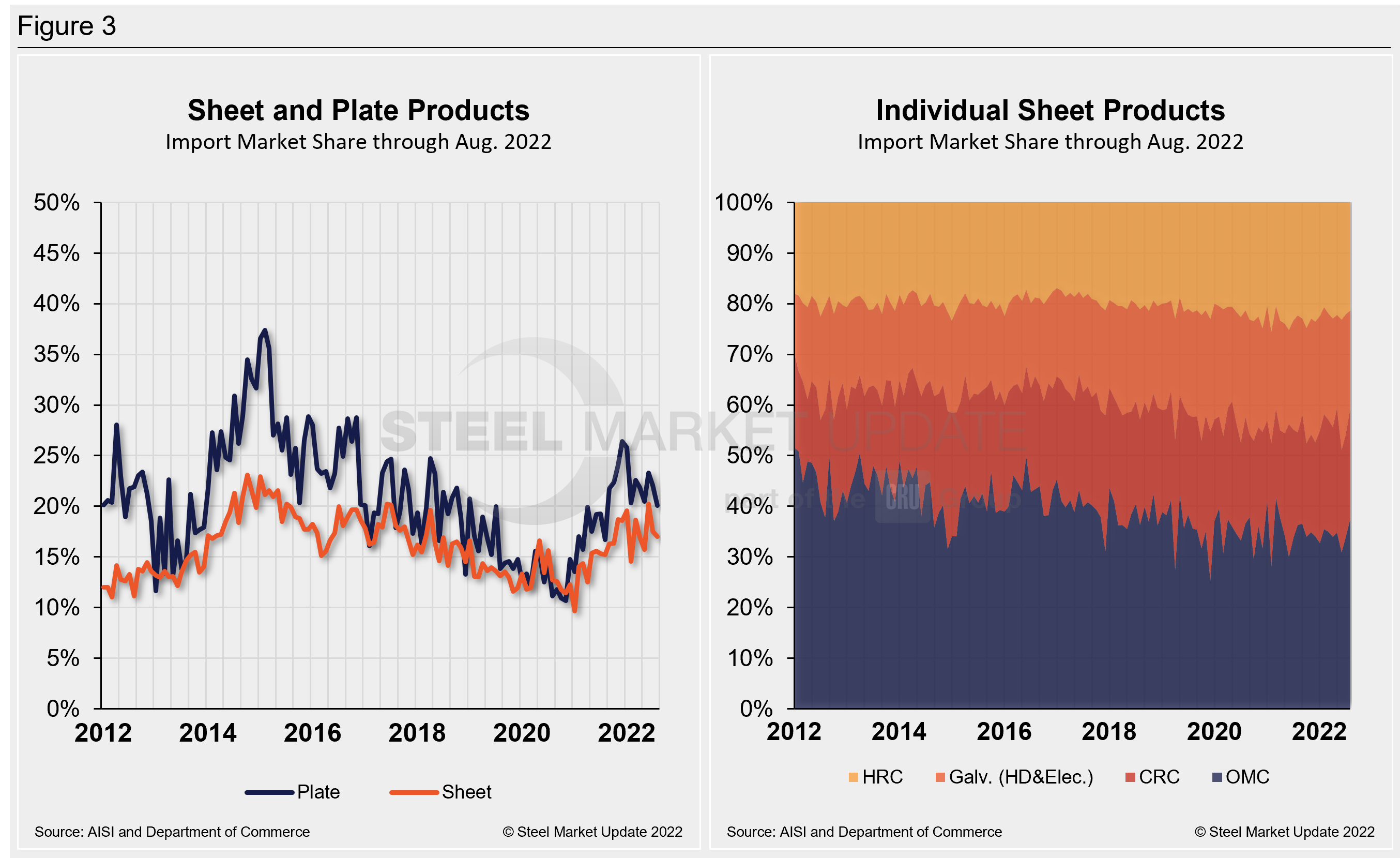

Hot-rolled and cold-rolled sheet and strip have seen a trend shift along with plate products, illustrating how import competition is impacting domestic products in three months compared to 12 months. HRC imports, along with plate imports, lost ground, while CR, galvanized, and OMC all gained ground. The most notable of those subcategories is HRC and plate in coil, which have both seen declining import market shares through August.

The import market share of individual plate products and a breakdown of the market share for plates in coil are displayed together in Figure 2. The historical import market share of plate and sheet products, and the import market share of the four major sheet products, are shown side-by-side in Figure 3.

By David Schollaert, David@SteelMarketUpdate.com