Market Data

November 9, 2022

Manufacturing Update: Indicators Strong Through September

Written by Brett Linton

Data on US industrial production, capacity utilization, orders and inventories remained strong through September, indicating a healthy manufacturing sector. The health of the manufacturing economy has a direct bearing on the health of the steel industry.

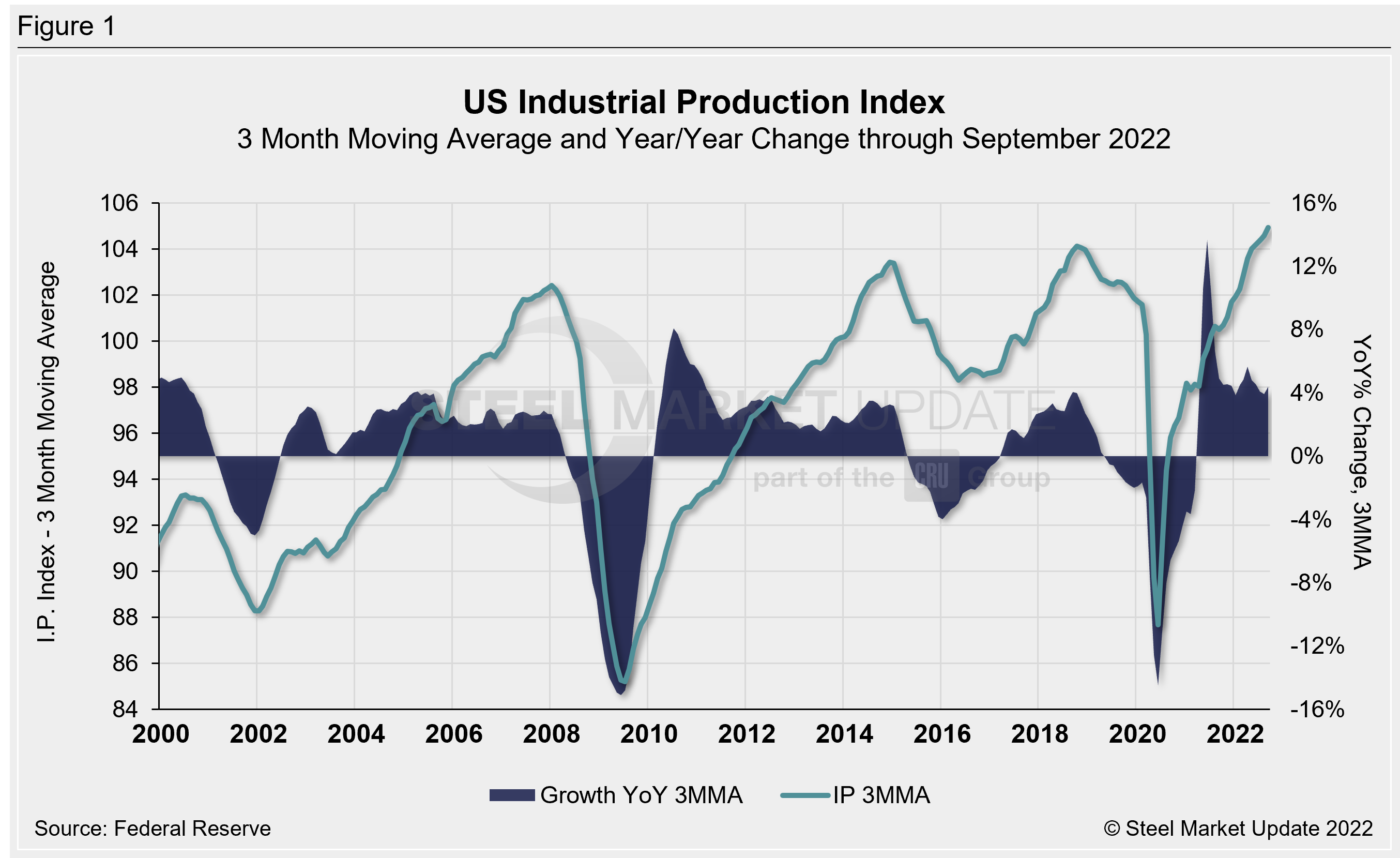

![]() The Industrial Production (IP) Index

The Industrial Production (IP) Index

The IP index is a gauge of output from factories, mines and utilities. Figure 1 shows the IP index since 2000, graphed as a three-month moving average (3MMA) to smooth out some of the monthly variability. As a 3MMA, the IP index reached a 10-year low of 87.7 in June 2020, recovering nearly each month since then. The 3MMA through September is 104.9, up 4.4% over the same period last year and the highest measure in the Federal Reserve’s 103+ year history.

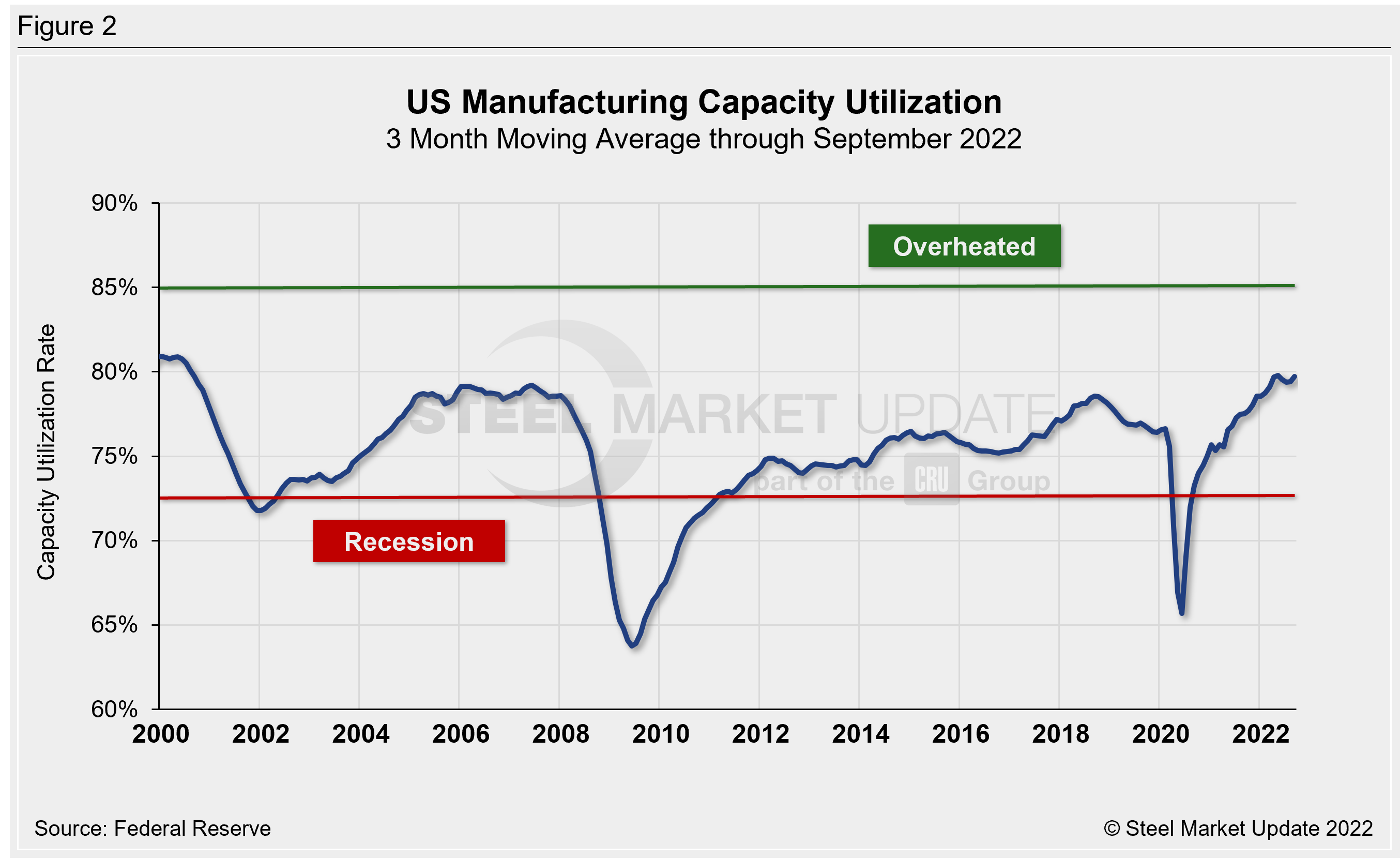

Manufacturing Capacity Utilization

Manufacturing capacity utilization through September was measured at 79.7% as a 3MMA, now at a two-year streak above recessionary territory. September represents the second highest 3MMA rate recorded in over 20 years, just behind May 2022 at 79.8%. Capacity utilization had hovered around 74–78% for most of the 2010s, stalling in April 2020 to reach a low of 66% in June 2020 (Figure 2).

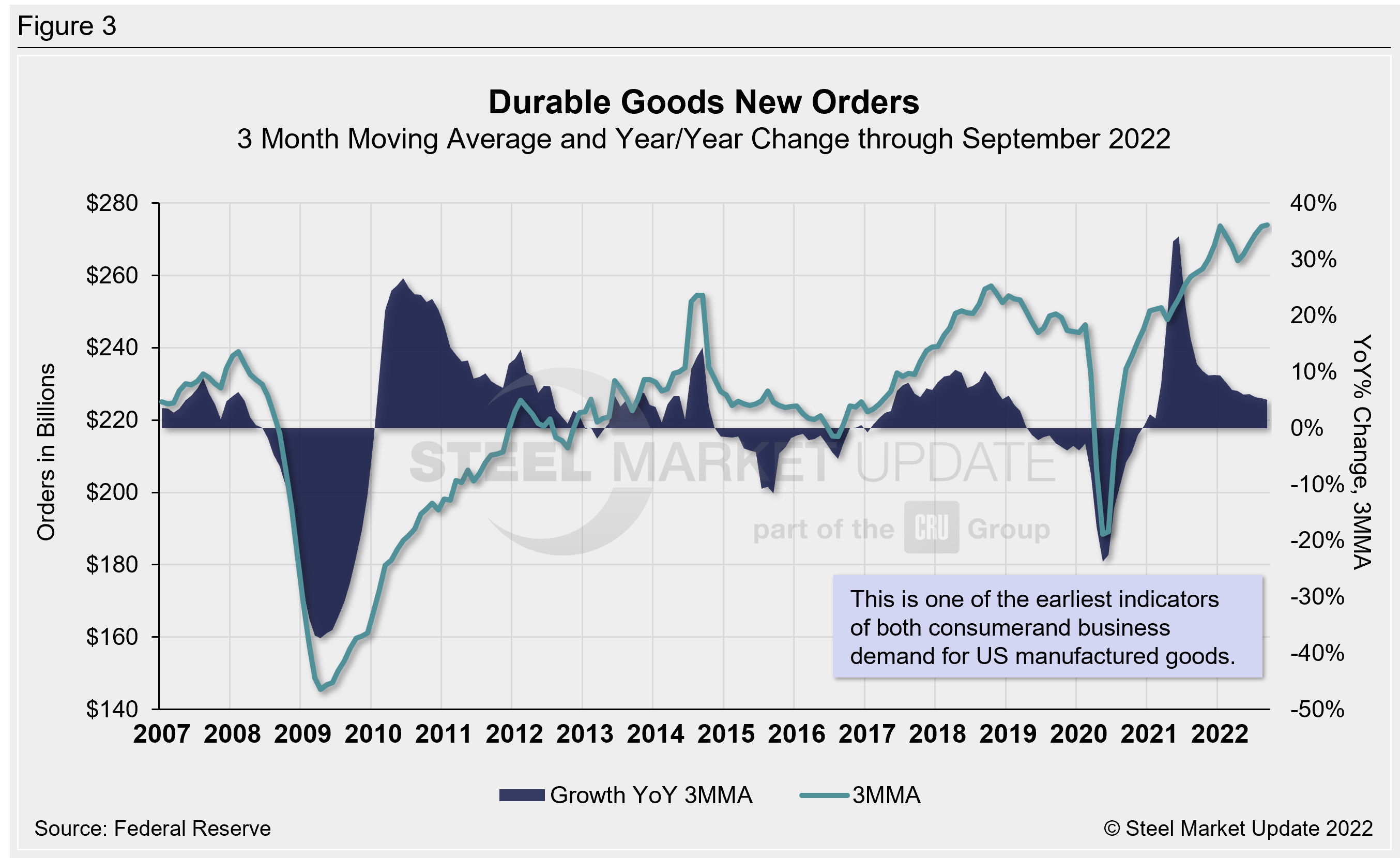

New Orders for Durable Goods

New orders for durable goods are an early indicator of consumer and business demand for US manufactured goods. Levels continue to recover from the 2020 shock, reaching a record high through the latest data (Figure 3). New orders are at $273.9 billion as a 3MMA through September, up 5.0% over the same period in 2021. This is now the highest level in our history dating back to 1992. Recall the 3MMA had dropped by 23% from February through May 2020, reaching a 10-year low of $188.4 billion.

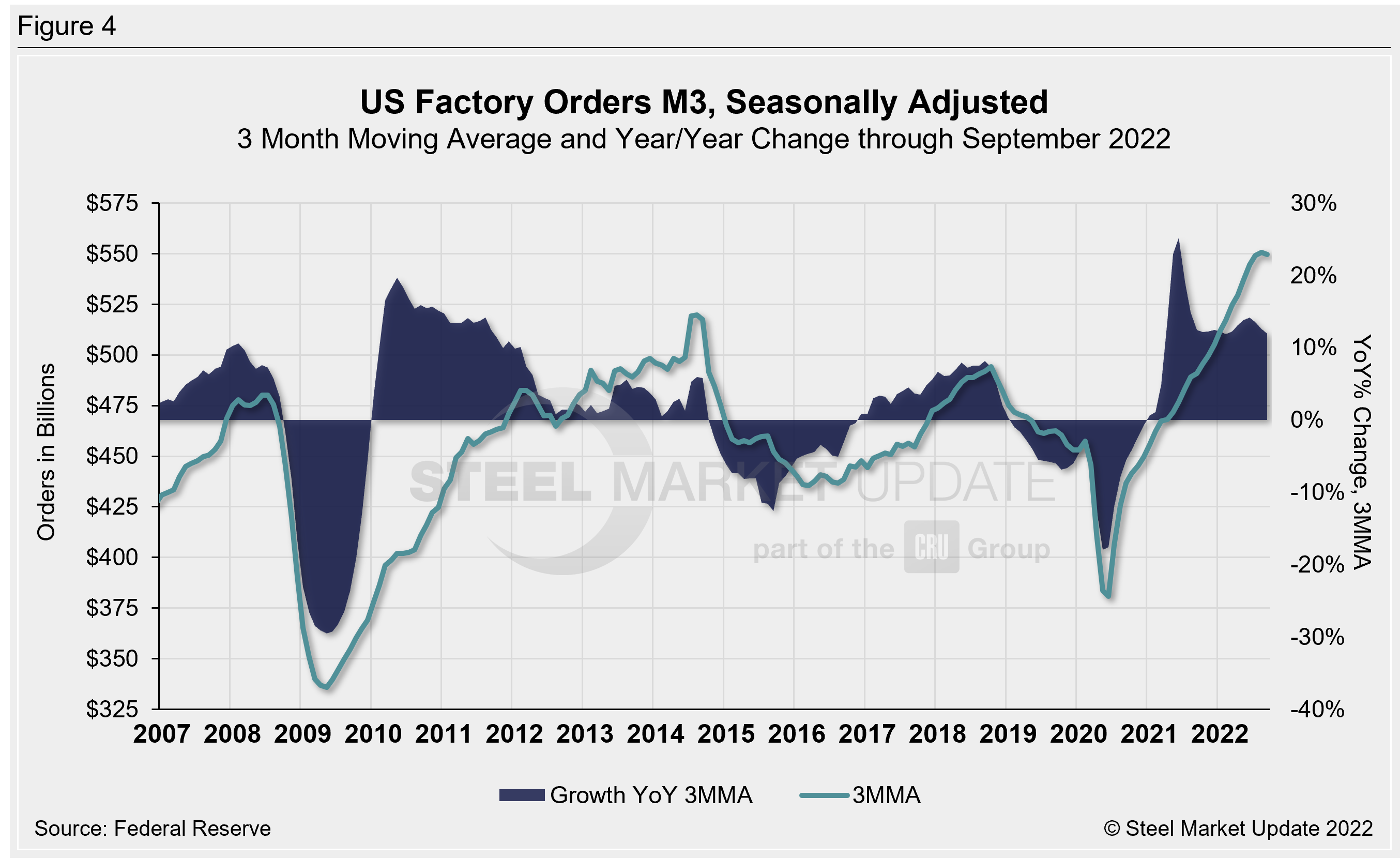

New Orders for Manufactured Products

The growth rate of new orders for manufactured products as reported by the Census Bureau was slightly negative for most of 2019, then declined sharply from March to July 2020 (Figure 4). On a 3MMA basis, factory orders increased each month after that through August 2022 to reach $550.7 billion, the highest level in our 30-year data history. Factory orders eased slightly to $549.7 billion in September, up 11.9% compared to levels one year earlier.

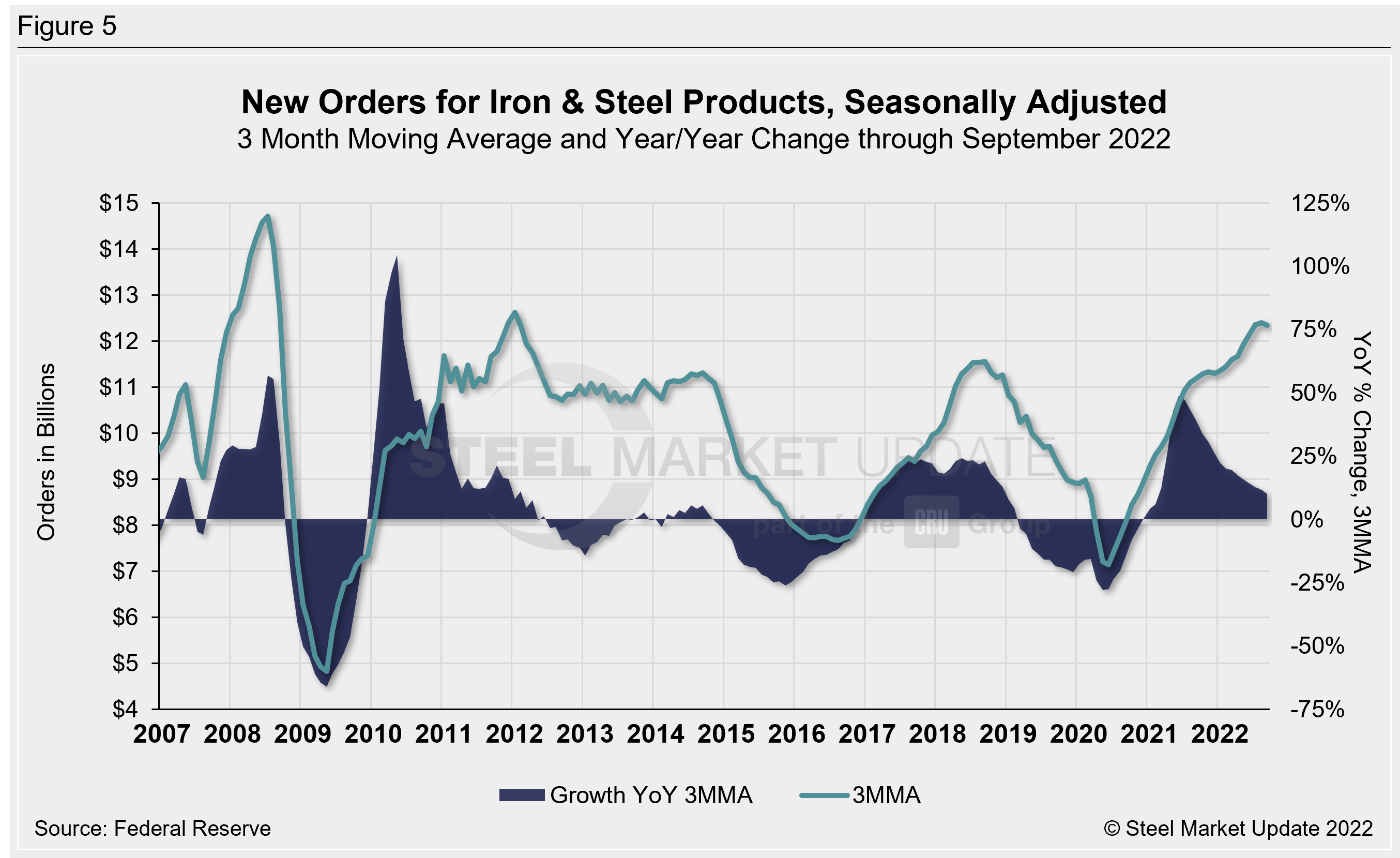

New Orders for Products Manufactured from Iron and Steel

Within the Census Bureau M3 manufacturing survey is a subsection for iron and steel products. Figure 5 shows the history of new orders for iron and steel products as a 3MMA. The 3MMA new order level is now at $12.3 billion through September, having reached a 10+ year high of $12.4 billion one month prior. The 3MMA year-over-year growth rate through September is 10.2%, the smallest growth rate recorded since February 2021. Recall this rate reached an 11-year high of 49.0% in June 2021, following a 10-year low of negative 27.8% in May 2020.

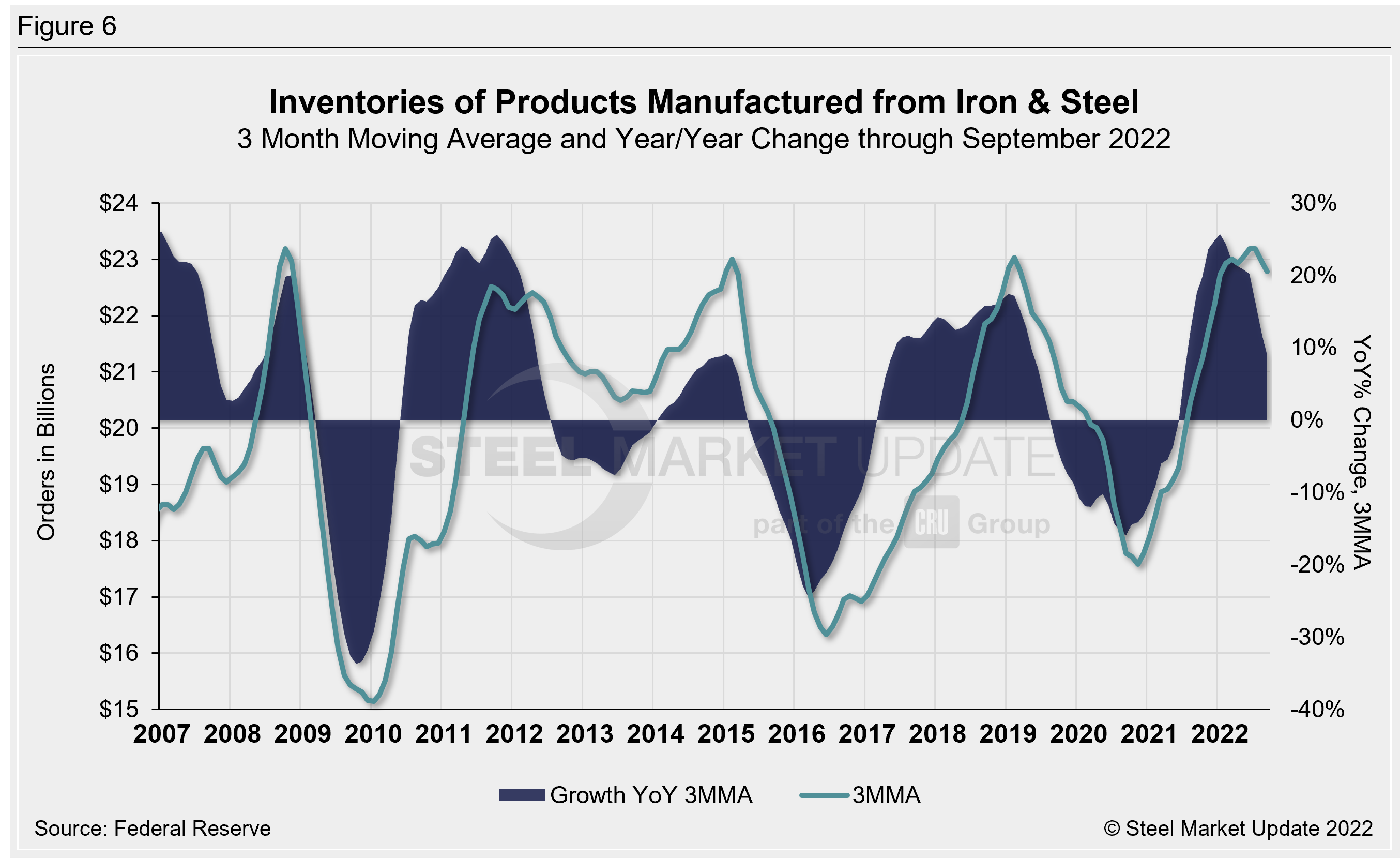

Inventories of Products Manufactured from Iron and Steel

Inventories of iron and steel products broke their multi-month decline streak in November 2020, rising each month through May 2022. The latest iron and steel inventory levels totaled $22.8 billion on a 3MMA basis in September, up 9.0% compared to the same period the year prior (Figure 6). Inventory levels totaled $23.2 billion in May of this year, the highest 3MMA measure in our 30-year history.

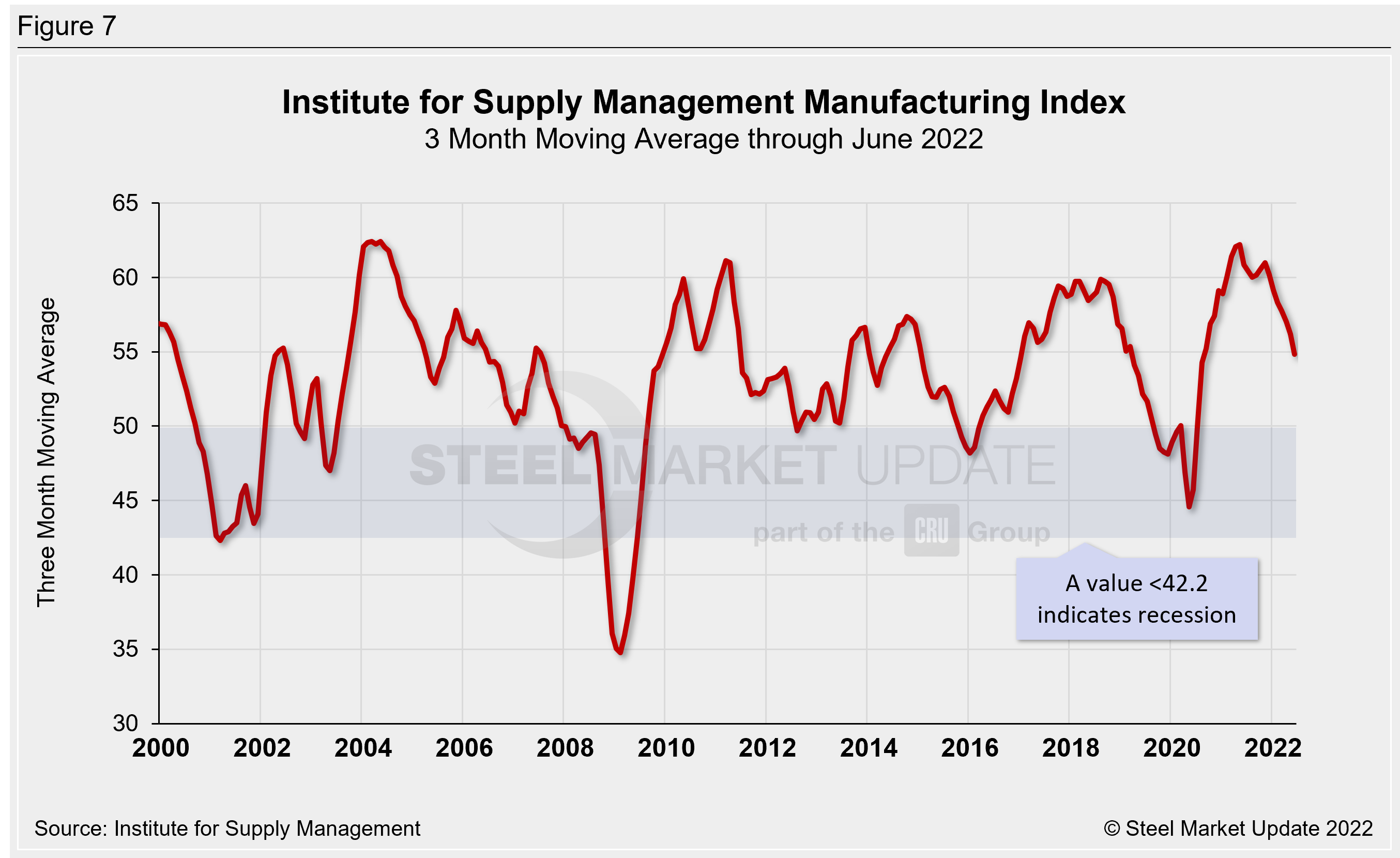

The ISM Manufacturing Index

The Institute for Supply Management® Manufacturing Index is a diffusion index. An index value above 50 indicates that the manufacturing economy is expanding. As Figure 7 shows, the index on a 3MMA basis was in contraction territory from September 2019 through July 2020, peaking in May 2021 at 62.2. The index has eased since but remains in expansion territory, now standing at 51.3 as a 3MMA in October. This is down 0.9 percentage points from the month prior, down 7.8 percentage points from the beginning of the year, and down 10.9 percentage points from the May 2021 peak.

“Manufacturing expanded for the 29th straight month in October. Panelists’ companies continue to carefully manage hiring, month-over-month supplier delivery performance was the best since March 2009, and the Prices Index indicated decreasing prices for the first time since May 2020. Like in September, mentions of large-scale layoffs were absent from panelists’ comments, indicating companies are confident of near-term demand,” said ISM business survey committee chairman Timothy Fiore.

By Brett Linton, Brett@SteelMarketUpdate.com