Market Segment

December 15, 2022

Hot Rolled Futures: Dead Cat Bounce or Trend Reversal?

Written by Michael D'Angelo

Editor’s note: SMU Contributor Michael D’Angelo is a researcher and trader at Marex. In his role, Mike performs fundamental and quantitative analysis, which directly leads to actionable trading/risk management strategies across the base, precious, and ferrous metals derivative spaces. Prior to joining Marex, Mike received a BA in economics with a minor in finance from Princeton University. Mike can be reached at mdangelo@marex.com for comments/questions.

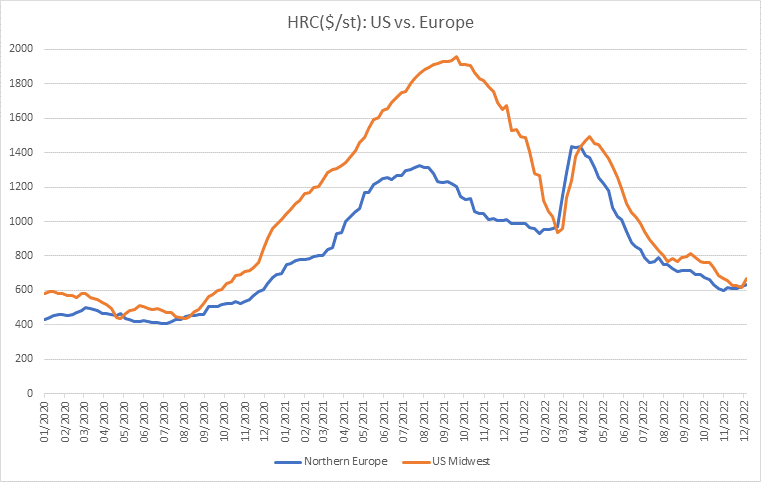

CRU’s weekly Midwest hot-rolled coil (HRC) index came in at $667 this week, up $49 (8%) from last week. This marked the index’s first increase since Oct. 19, which was a $1 increase, and Sept. 21 before that. This week’s rise was the largest since March 20, when the Russia/Ukraine conflict cut off pig iron from the two largest global exporters and caused a massive price spike.

The gap between US and European HRC converged, and Europe actually printed at a slight premium last week before the recent recovery in US prices. Now Europe is trading at about a $30 discount, depending on which assessment you look at.

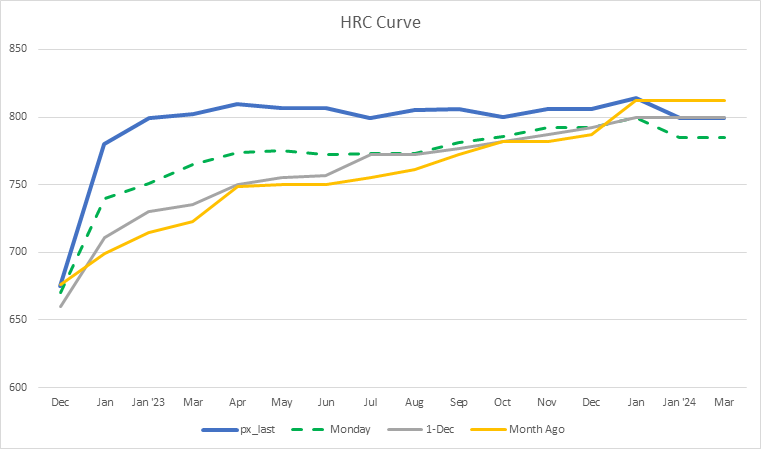

Cleveland-Cliffs announced a second price increase on Tuesday of $50/ton, making their minimum base price for HR $750/ton. However, many folks are skeptical about whether or not the market will accept the full $50 increase, although most market participants agree that average prices next year will be higher than where they are now. Sentiment is quite similar in Europe, with most expecting some price hikes soon, as demand is beginning to pick up from end-users and specifically from the auto industry.

On the economic data front, factory orders (0.7% vs. survey 1.0%), University of Michigan Consumer Sentiment (57.0 vs. survey 59.1), and empire manufacturing (-11.2 vs. survey -1.0) all missed expectations. Consumer Price Index (CPI) beat expectations (0.1% vs. survey .3%), which caused a knee jerk rally across the board, but it was short-lived as Federal Reserve Chair Jerome Powell woke up feeling a smidge hawkish on Wednesday.

Steel imports for November are projected to be 1.9M mt based on licensing data, which would be the lowest since February 2021.

December/January has melted down to about $100 contango over the past few days, while the rest of the curve has become essentially flat. The market’s best guess right now is that HR prices will hang out around $800 for the entirety of 2023.

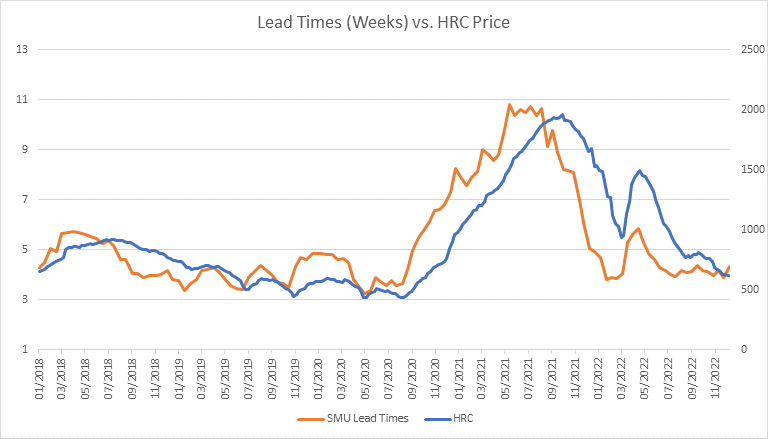

SMU steel lead times inched up to 4.35 on Dec. 8, the highest reading since Sept. 15. Buyers have slowly been returning to the market, and this trend is expected to continue into January, which is reflected in the futures curve.

SMU mill’s willingness to negotiate survey fell to 71 on Dec. 8. The prior survey number was 95, and the average of the last 5 readings was about 93. The sharp decline signals power shifting from buyers to sellers.

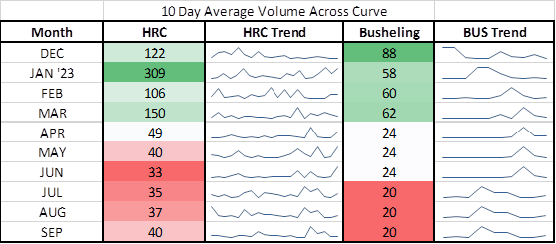

Above are the average 10-day volumes for the HRC and busheling contracts. Trading activity has dipped as we approach the holidays.

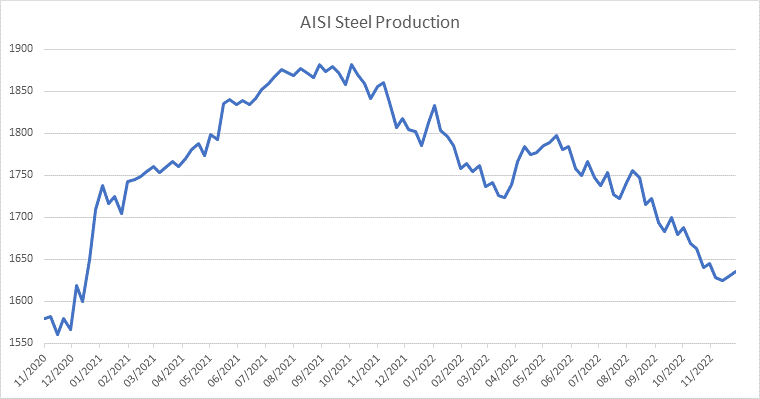

US Steel Production (AISI) rose for the second consecutive week by 5,000 tons to 1.635 million tons, while Steel Capacity Utilization inched up to 73.3 from 73.1. Could we be seeing the end of what has been a prolonged downtrend?

By Michael D’Angelo, Marex, mdangelo@marex.com