Analysis

January 15, 2023

CRU: What Our Clients Expect For 2023

Written by Alex Tuckett

By CRU Principal Economist Alex Tuckett, from CRU’s Global Economic Outlook

In December we conducted our annual macroeconomic survey, asking our clients to look into the future of the global economy. As we look back on a year full of challenges for the global economy and head into 2023 full of uncertainty, we explore the key findings from our client survey, including questions on global growth, inflation, key risks, and the war in Ukraine.

On average, our clients share our view that inflation will fall sharply in 2023. However, they continue to see stubborn inflation – together with high energy prices and the war in Ukraine – as the biggest risks to the outlook. And overall, clients are slightly more pessimistic about growth than we are – at least in Europe and North America.

105 clients responded to the survey in December 2022 with 39% Europe based, 37% in the Americas, 22% in Asia, and 2% in Africa. Out of the 105 respondents, 49% worked in the metals industry, 13% in mining, 13% in fertilizers, and 6% in financial and trading industries, with the remaining 19% in other sectors (energy, end-use, or other).

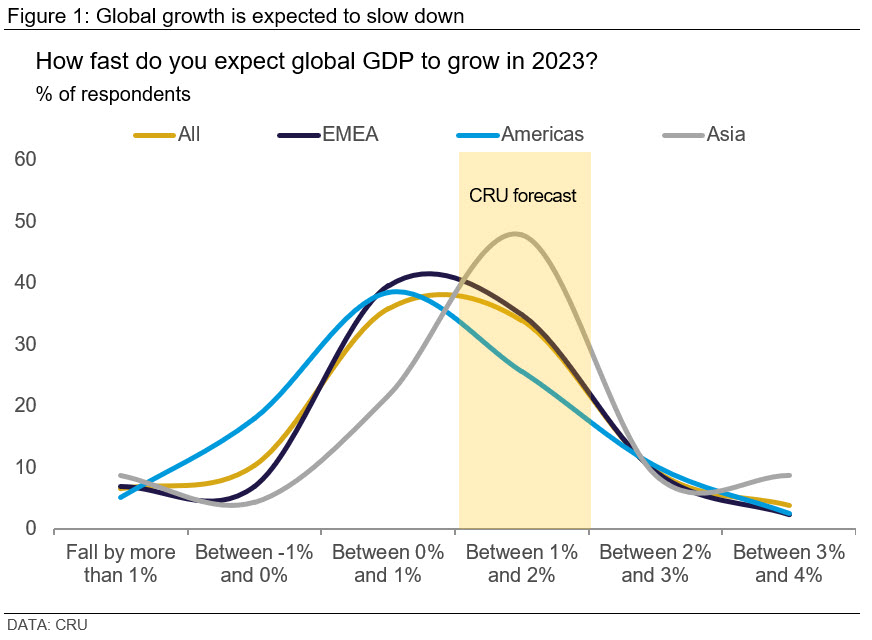

Our Clients Expect Global Growth to Slow Down in 2023

CRU forecasts global growth of 1.6% in 2023, with Europe and the US sliding into a mild recession. Our clients are, on average, slightly more pessimistic. 40% of clients expected growth between 0% and 1%, with a further 17% expecting GDP to see an outright fall. Only 13% expect growth to be higher than 2%. There is some regional variation in the responses; clients in Asia are on average notably more optimistic, and those in the Americas are more pessimistic, about growth in 2023 (Figure 1).

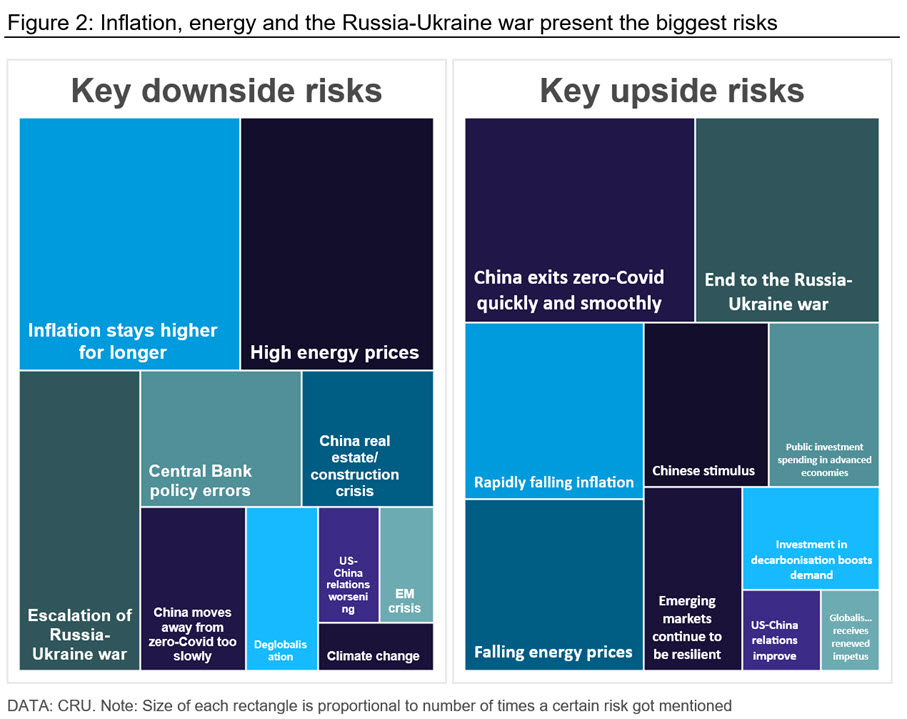

Uncertain Times with Inflation, Energy, and War in Minds

We asked our clients to name their top three upside and top three downside risks for the new year. The results are shown in Figure 2. Prolonged inflation was the most widely cited downside risk, with 68% of clients choosing it, followed by high energy prices (59%) and an escalation of the Russia-Ukraine war (44%) (Figure 2, left-hand side). The main risks identified by our clients are closely related to each other, with energy prices driving inflation and the Russia-Ukraine war leading to higher energy prices. Clients are less concerned about the impact of climate change in 2023 or a further deterioration in US-China relations. We agree that prolonged high inflation and continued high energy prices are major downside risks, which we have discussed in a recent blog post and insight.

The related issues of the war, energy, and inflation also provided some of the most cited upside risks (Figure 2, right-hand side). However, the upside risk named by most clients was a quick and smooth exit by China from its zero-Covid policy, which 57% of respondents choose. Although China’s exit from its zero-Covid policy has certainly been quick, it has not so far been smooth.

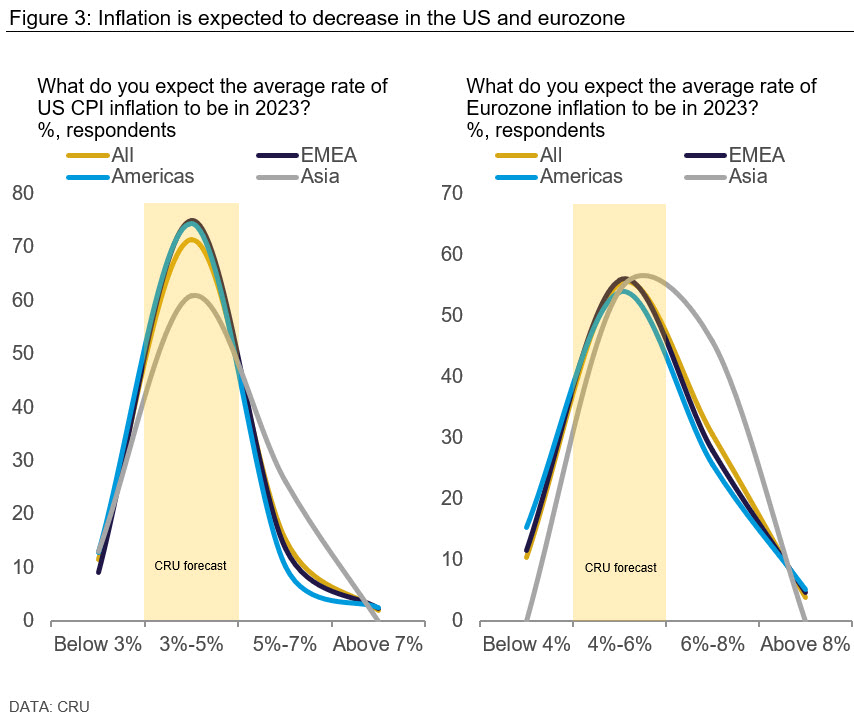

Clients Expect Inflation to Fall – But How Fast?

High energy prices, supply chain problems, and strong demand have led to levels of inflation unseen in recent history, peaking at 9.1% in the US and 10.6% in the eurozone. With moderating energy prices, easing supply problems, and tighter monetary policy, we expect inflation to fall sharply in 2023, averaging 4.1% in the US and 5.5% in the eurozone. Most of our clients agree with our view, expecting inflation of between 3-5% in the US and 4-6% in the eurozone (Figure 3). Clients see more upside risk to inflation in the eurozone, with a greater skew in the distribution. Clients based in Asia are more cautious, with a greater proportion expecting inflation to fall more slowly in both the US and the eurozone.

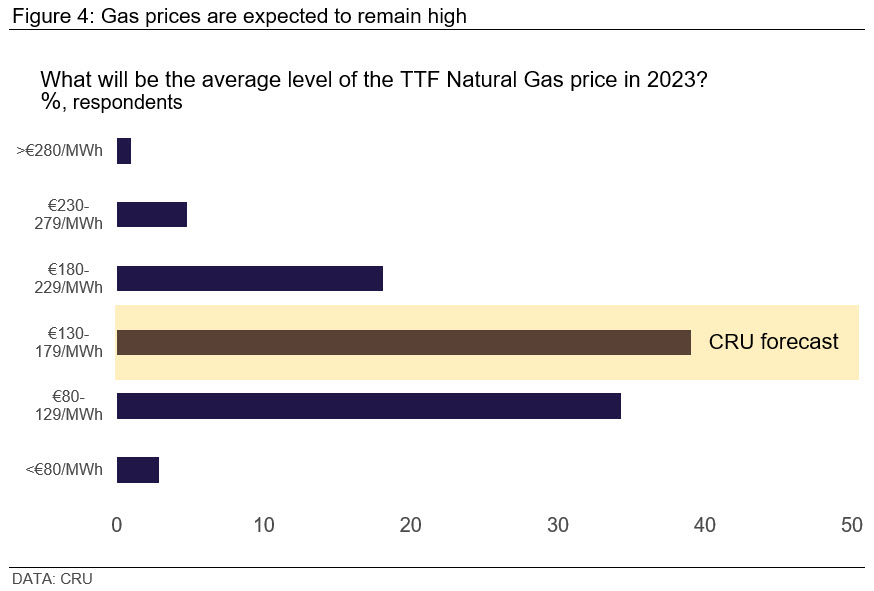

Gas Prices are Expected to Remain High

The Russia-Ukraine war has disrupted global energy markets with TTF natural gas prices reaching a record high of €277 per MWh in August 2022. Recently, the price of gas has fallen below pre-war levels due to the mild winter, weaker industrial demand, and strong flows of LNG into Europe. We expect an average TTF gas price of €150 per MWh in 2023.

Similarly, our clients expect gas prices to remain elevated for 2023. Only 3% of customers expect the TTF natural gas price to be below 80 euros, while 39% expect it to be between €130 and €179. Although a significant minority of respondents (34%) expect prices to be in the €80-129 range, this is still very high relative to pre-2021 levels. For oil, the majority of our respondents (52%) expect brent oil prices to be between $70 and $89 per bbl in 2023, which is slightly below our own forecast of $95 per bbl.

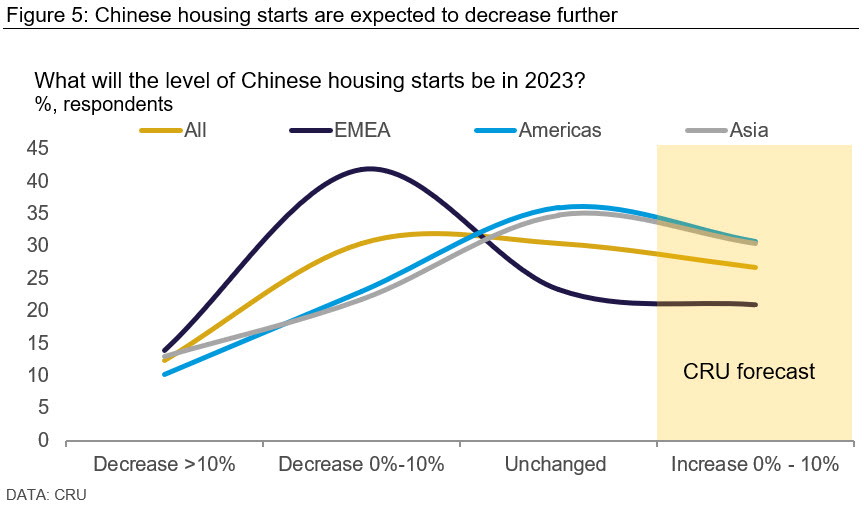

Clients Expect Further Decline in the Chinese Housing Market

As of November 2022, Chinese housing starts decreased by 50.8% year-on-year (YoY). The downturn in the Chinese property sector was triggered by Evergrande’s default in late 2021 and extended throughout 2022 due in part to China’s zero-Covid policy.

With China loosening its policy, we predict Chinese housing starts to recover in the second half of 2023, with a modest increase of around 4% YoY for 2023 as a whole. Our clients foresee difficult times ahead for the Chinese housing market. Most respondents forecast either negative growth or stagnation in 2023. Only 27% of respondents expect housing starts in China to increase in 2023. Respondents from EMEA are far more pessimistic than those in Asia and the Americas (Figure 5).

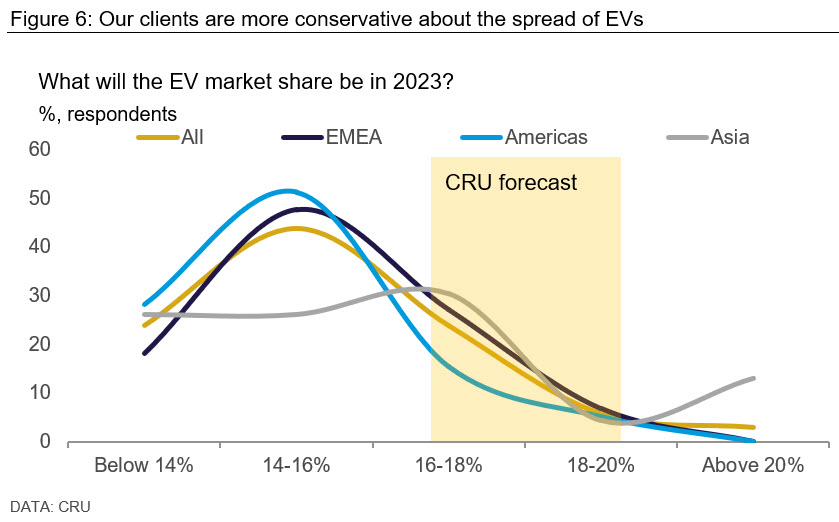

Our Clients Expect Slower EV Adoption than we do

The market share of electric vehicles (BEV and PHEV) doubled in 2021, reaching 8%, and is expected to increase further to 14% in 2022. CRU forecasts that EV sales will account for 18% of the market by 2023. Most respondents to our customer survey expect EV market share to grow more slowly, with 44% expecting the share of electric vehicles to be 14-16% in 2023, 24% believe it will be even lower, and another 24% expecting it to be between 16-18%.

Customers may be mindful of the risks to electric vehicle adoption, such as the energy crisis, lack of chips, and lack of charging infrastructure. Customers in Europe and Asia are more optimistic about the introduction of elective vehicles than customers in the Americas. This probably reflects the higher existing EV market share in Europe and China, but it could also indicate that the US green policy agenda has only partly filtered through perceptions.

The Russia-Ukraine war will continue to shape global markets and represent a major uncertainty for the near future. We asked our clients when they expect the Russia-Ukraine war to end. Responses were evenly distributed, indicating the high degree of uncertainty: 35% expect it to end in the second half of 2023, 30% expect it to end in 2024, 18% expect it to end in the first half of 2023, and 17% expect it to end later than 2024.

Overall, our survey paints a picture of a metals and mining sector that is cautious about the global economy in 2023, and mindful of the downside risks. This is unsurprising given the series of economic and political shocks that hit the world in 2022. Let’s hope 2023 brings more positive surprises.

This article was originally published on Jan. 9 by CRU, SMU’s parent company.

By CRU Principal Economist Alex Tuckett, Senior China Economist Henry Hao, End Use Economist Arthur Wang, and Economist Veronika Akhmadieva from CRU’s Global Economic Outlook

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com