Prices

February 2, 2023

Lead Times Flat While Prices Rise

Written by Becca Moczygemba

Steel mill lead times have remained flat despite rising prices, according to SMU’s latest market survey.

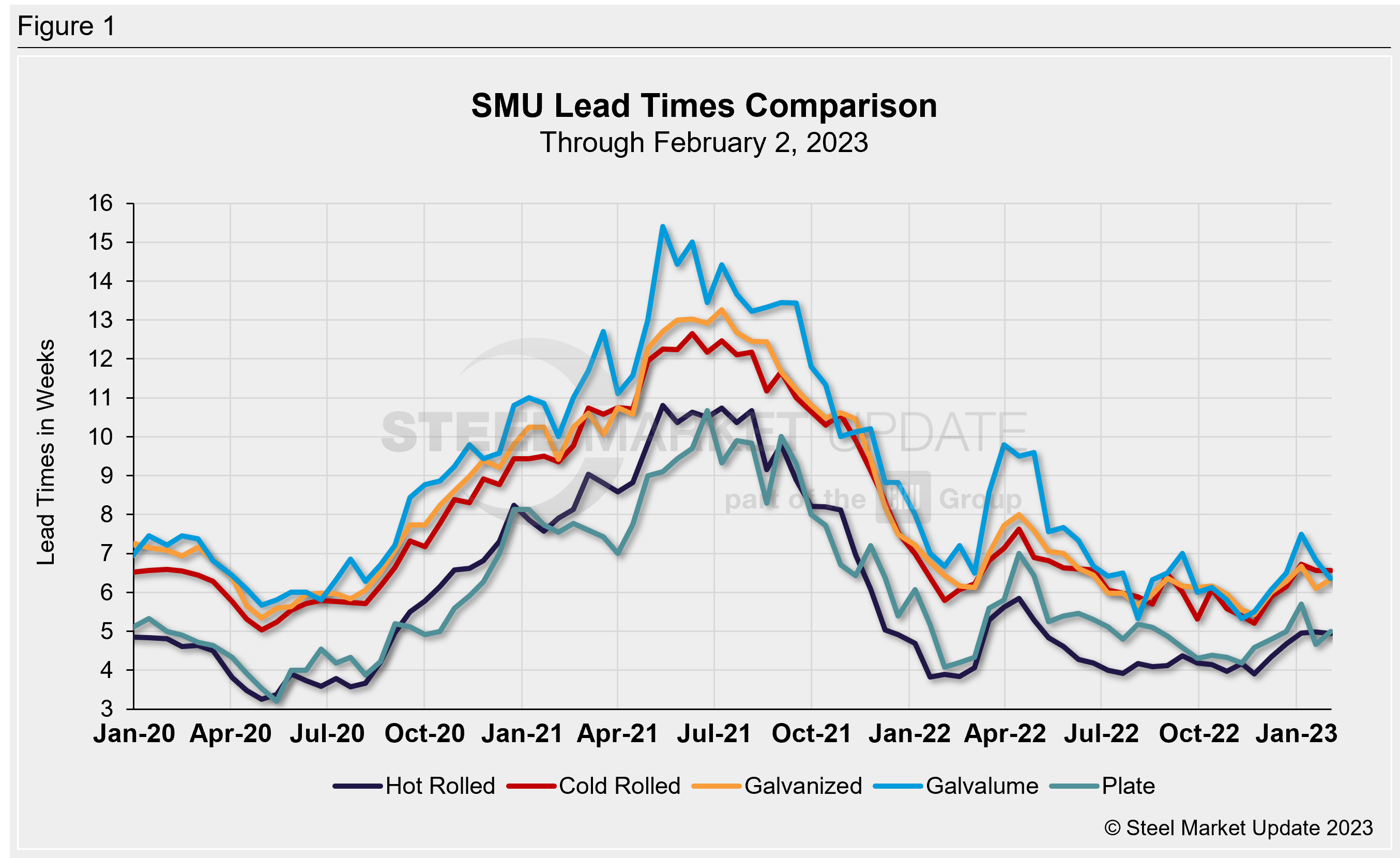

SMU’s hot-rolled lead time is approximately 5 weeks, unchanged from our last check of the market two weeks ago.

Cold-rolled lead times remained at roughly 6.6 weeks, similar to two weeks ago. Galvanized inched up to 6.3 weeks from 6.1 weeks.

Galvalume lead times were 6.4 weeks on average, the lowest since the beginning of the year. Note that Galvalume figures can be volatile due to the limited size of that market and our smaller sample size.

Plate lead times rose to 5.0 weeks, up from 4.7 weeks in mid/late January.

When asked about the future direction of lead times, 63% of executives responding to this week’s questionnaire reported that they expect lead times to be relatively flat into April, up from 55% in the last survey. About 22% percent think lead times will extend, while about 15% think they will contract. Premium members can view a longer history of this data series and others by exploring the market trends report.

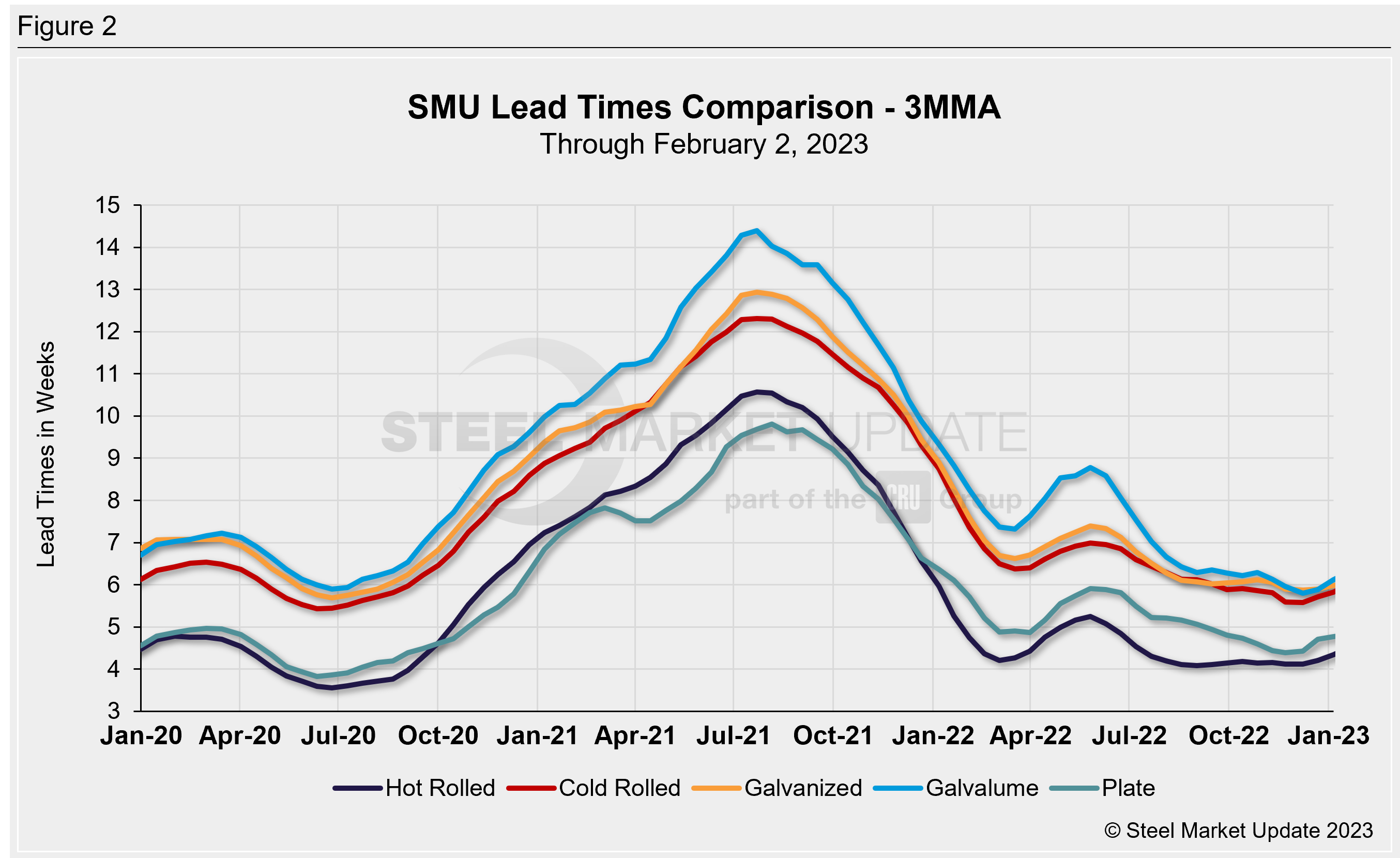

Looking at lead times on a three-month moving average (3MMA) basis can smooth out the variability in the biweekly readings. As a 3MMA, lead times for all products were relatively flat compared to two weeks ago. The latest 3MMA lead time for hot rolled inched up 0.1 week to 4.6 weeks. Cold-rolled lead times moved up to 6.2 week. Galvanized lead times ticked up to 6.1 weeks from 6.0 weeks, while Galvalume lead times increased 0.2 weeks to 6.5 weeks. Plate lead times also rose 0.2 weeks to 5 weeks.

Note: These lead times are based on the average from manufacturers and steel service centers who participated in this week’s SMU market trends analysis. SMU measures lead times as the time it takes from when an order is placed with the mill to when the order is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. To see an interactive history of our Steel Mill Lead Times data, visit our website here.

By Becca Moczygemba, Becca@SteelMarketUpdate.com