Prices

March 2, 2023

HRC Futures: Sellers Take Control of Market

Written by Michael D'Angelo

Editor’s note: SMU Contributor Michael D’Angelo is a researcher and trader at Marex. In his role, Mike performs fundamental and quantitative analysis, which directly leads to actionable trading/risk management strategies across the base, precious, and ferrous metals derivative spaces. Prior to joining Marex, Mike received a BA in economics with a minor in finance from Princeton University. Mike can be reached at mdangelo@marex.com for comments/questions.

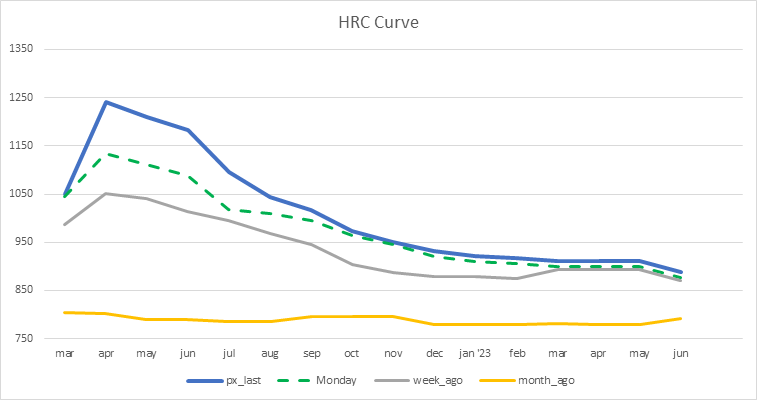

On Monday morning Cleveland-Cliffs yet again raised flat-roll steel prices by $100 per short ton (st). Since then, the CME April contract is up over $100 to about $1,240. The price hike marked the seventh increase by major steel mills since November. The justification seems to be filled order books and a tightening scrap market. However, many buyers are skeptical that input costs have risen enough to justify these prices, and feel that sellers are trying to extort them. Many are even calling the market a bubble.

While many market participants are in absolute disbelief over the aggressive price hike, there are very few import offers to compete with the domestic mills. Nonetheless, consensus seems to be that these price levels are unsustainable, and will likely correct shortly.

Recent economic data has been nothing spectacular. GDP quarter over quarter came in at 2.7% (Est. 2.9%), durable goods orders -4.5% (Est. -4%), construction spending -0.1% (Est. 0.2%) and consumer confidence 102.9 (Est. 108.5). New home sales (670k vs. Est. 620k) and Wards Total Vehicle Sales (14.89 million vs. Est. 14.68 million) were slight beats.

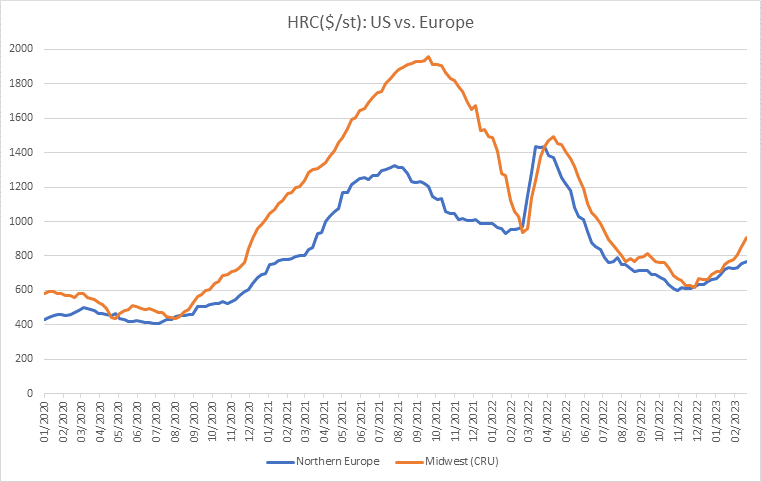

According to the latest CRU print of $908 (a $56 increase from the previous week), the US premium over northern European prices is about $150, which is a level that has not been seen since roughly a year ago. However, if the futures curve has any merit, the true premium is likely larger.

Order books in the European Union have been pretty strong and supply is not plentiful. Many are anticipating further price hikes as is occurring in the US, although there is disagreement about the general market trend. Some European mills are scheduled to restart capacity, and demand from key sectors such as automotive and construction have been unimpressive.

The front month spread blew out this week. See above how March/April is valued at about $200 contango.

While we saw some serious moves in the front end of the curve this week, the back end has been stable.

The busheling curve looks quite similar. April saw about a $50 rally this week, and is now valued at a $60 premium to March.

Key steel equities have rallied this week by about 10% on average, but they are certainly not pricing in sustained $1,250 HRC.

Domestic steel production jumped to 1.674 million metric tons last week to the highest level since October, an 18,000 metric ton increase from the previous week.

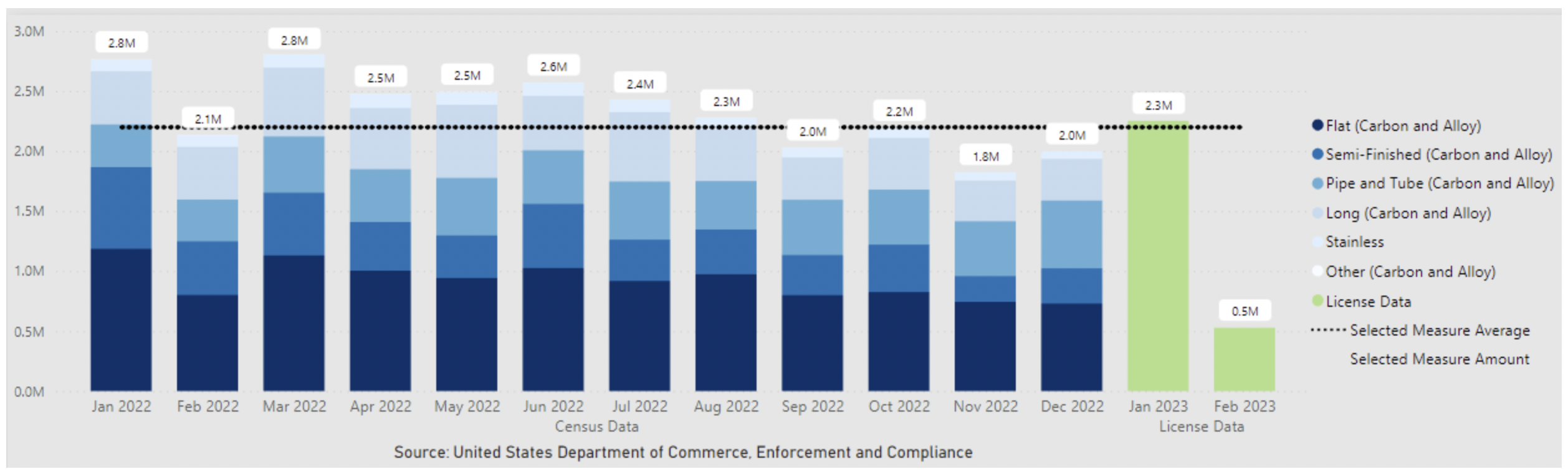

Imports for February are expected to be weak. However, February is a short month.

The market has not been seeing many import offers as much of the material is being used abroad, which was a significant reason why mills were able to get away with the price hikes. The next few weeks will be key to see if buyers can regain any control in this market.

By Michael D’Angelo, Marex, mdangelo@marex.com