Market Segment

March 21, 2023

Final Thoughts

Written by Michael Cowden

This week started without a price increase. Not that we needed another. Still, it felt weird after so many consecutive weeks of them.

Prices continue to move up even without increases and lead times continue to extend. But the pace has moderated.

Our hot-rolled coil price stands at $1,140 per ton ($57 per cwt) this week, up $25 per ton from last week and marking 16 consecutive weeks of gains dating back to the week after Thanksgiving.

A $25-per-ton week-over-week gain would be a big news in most other market cycles. But it’s a lot less than the ~$75-per-ton week-over-week gains we saw between mid-February and mid-March.

The slower pace of gains also squares with what I’m hearing in the market. Namely, that “caution” is the word of the day.

Yes, demand is still good and prices are still elevated. But there is increased concern as we move into the second half of the year that prices could unwind as quickly as they rose.

Such concerns might help to explain why we saw current sentiment strong in our last steel market survey even as future sentiment dipped.

Don’t get me wrong, even future sentiment is still mostly positive. And we’re seeing the continuation of some powerful trends.

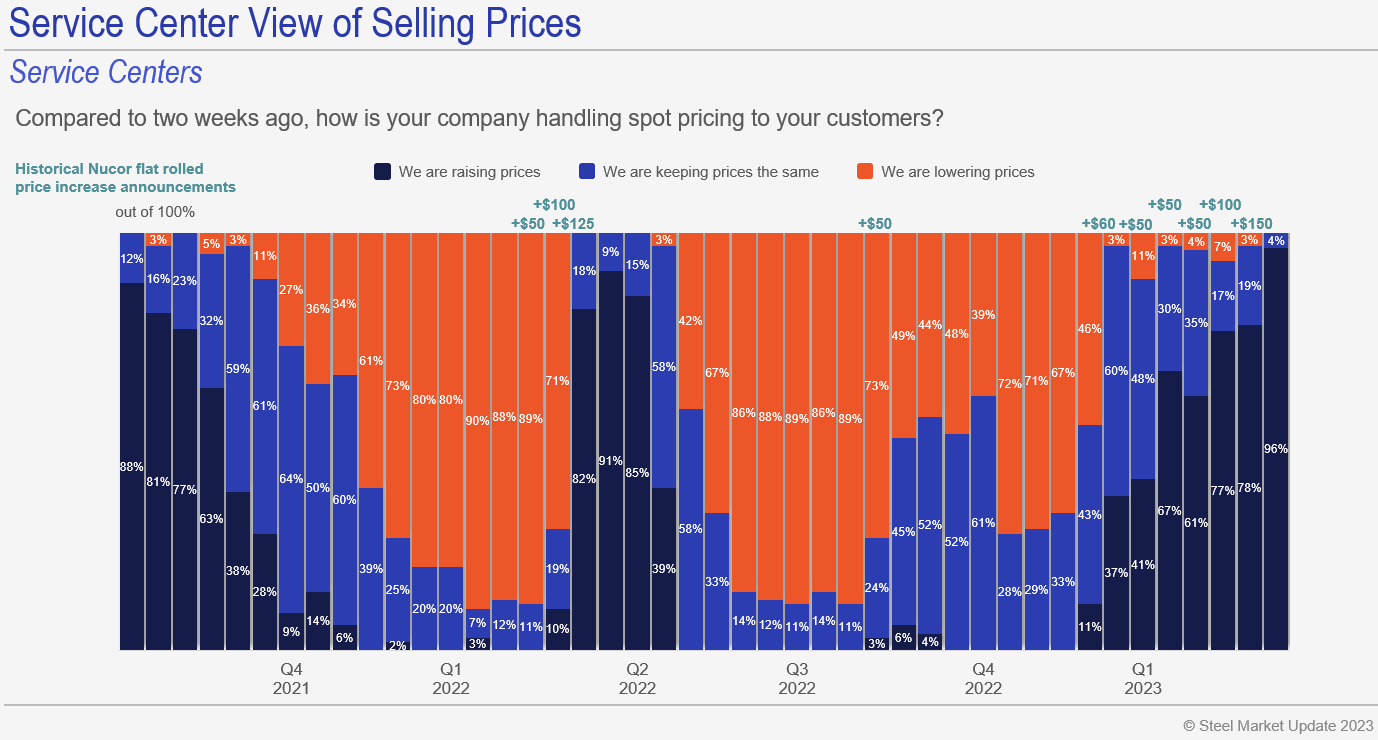

Prices continue to rise along the supply chain. Case in point: Nearly all service centers have been raising prices in tandem with mills:

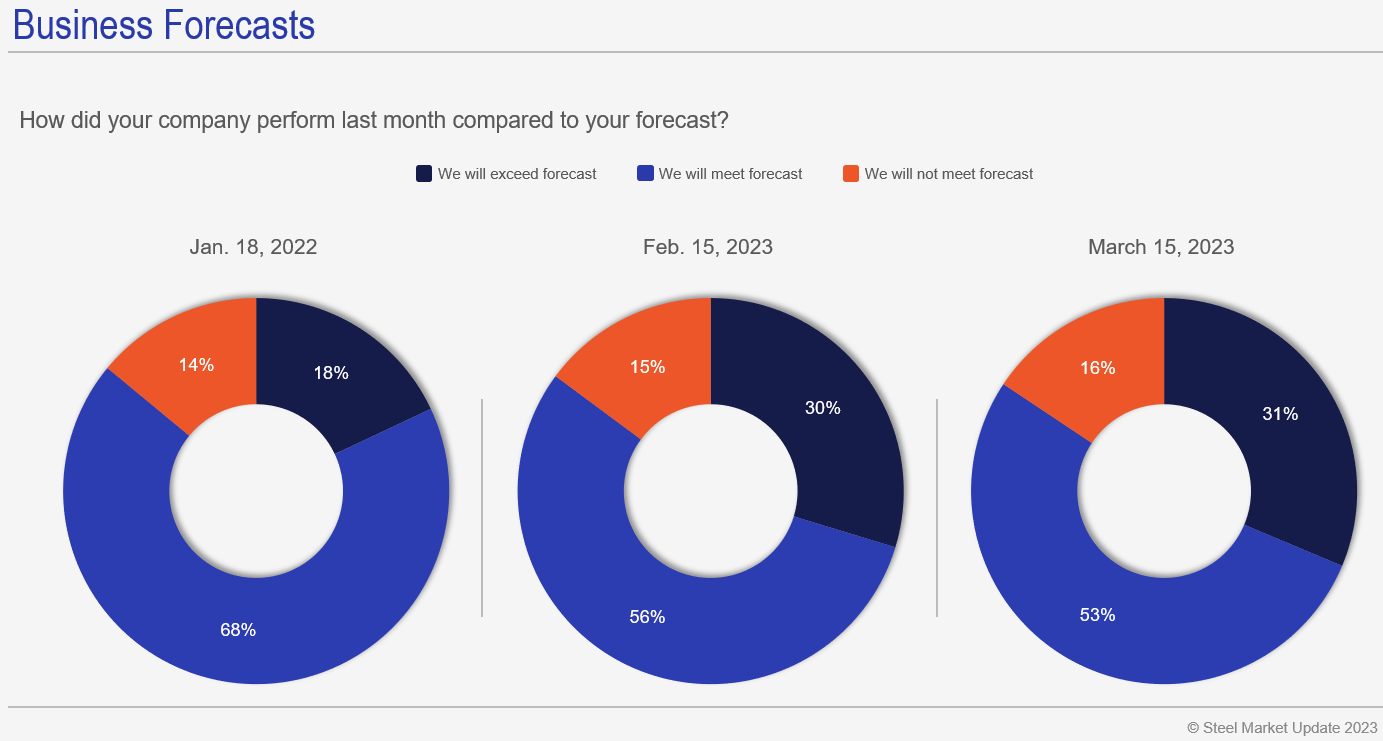

We also continue to see most people reporting back that demand is as good as or better than forecast:

Only a small minority are saying that they’re not hitting their targets. And that’s been the case since December.

We’ve clearly had a good run. The question is whether it will continue.

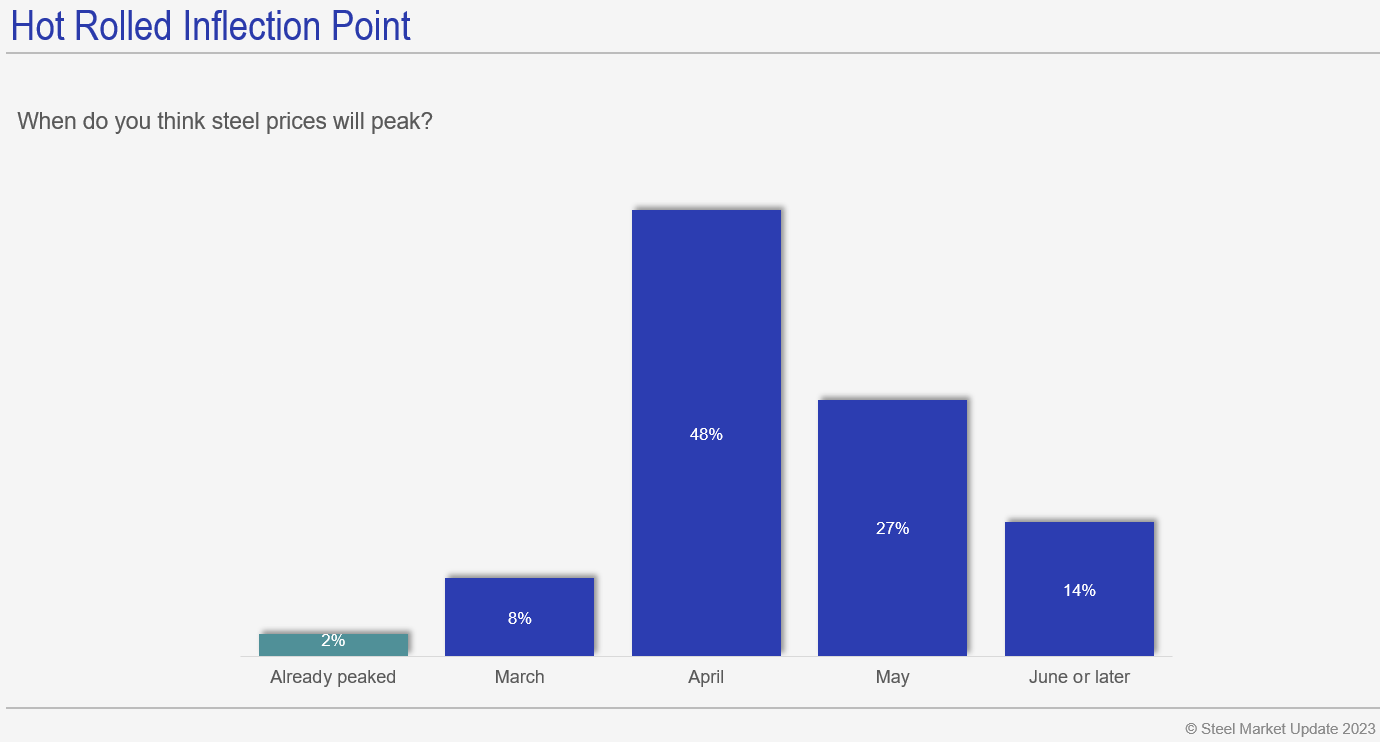

I ask that because of results like this:

Nearly half of our survey respondents think that prices will peak next month. Could the rally that we’ve seen since about Thanksgiving run out of steam?

US Steel alone has restarted two blast furnaces, one at its Mon Valley Works near Pittsburgh and one at its Gary Works near Chicago. That’s what should happen when prices are this high. And it should help alleviate the supply squeeze we’ve seen since the beginning of the year and perhaps bring US prices more back into alignment with world prices.

It seems possible that there might be more import supply on the way as well.

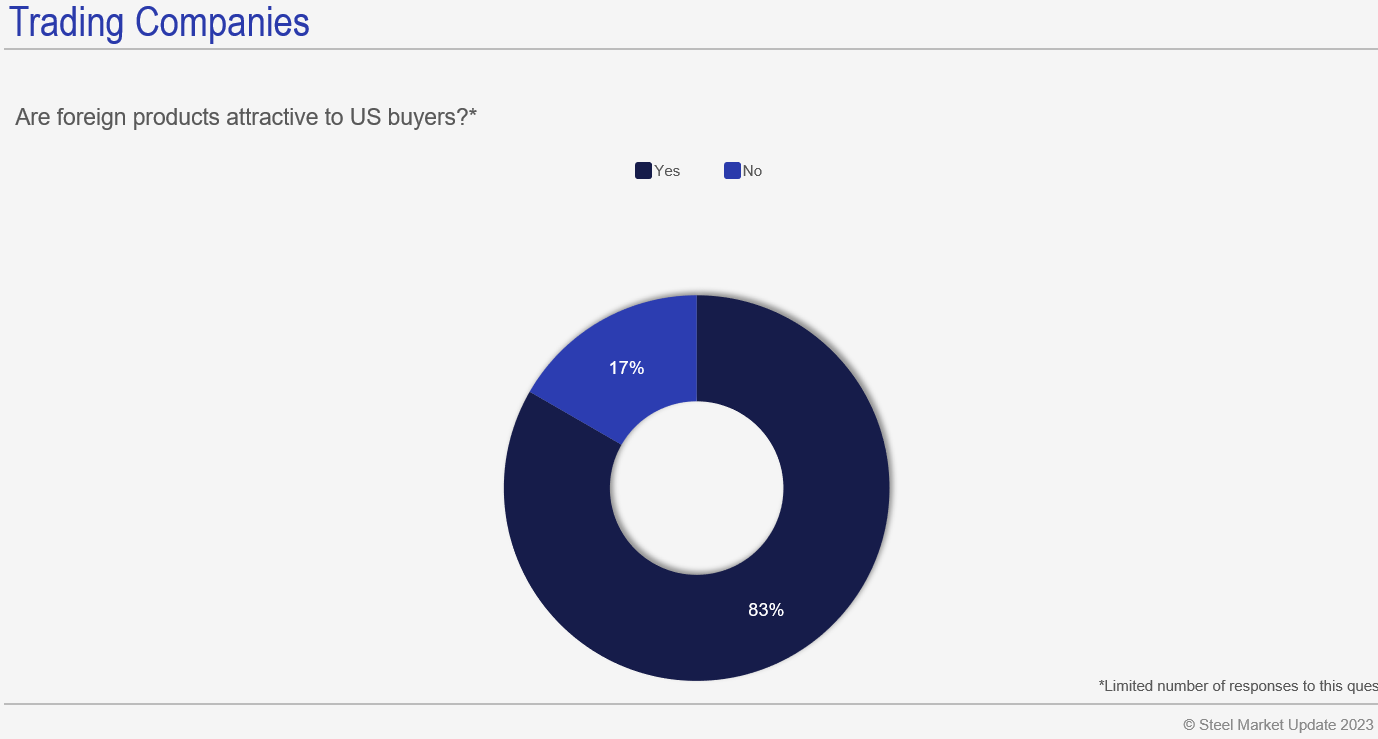

Most of the trading companies responding to our last survey said that imports were again attractive to US buyers:

Recall that US HRC prices fell into the $600s per ton in November, and into the $500s per ton for larger buyers. That in large part explains why we haven’t seen much in the way of imports in the first quarter.

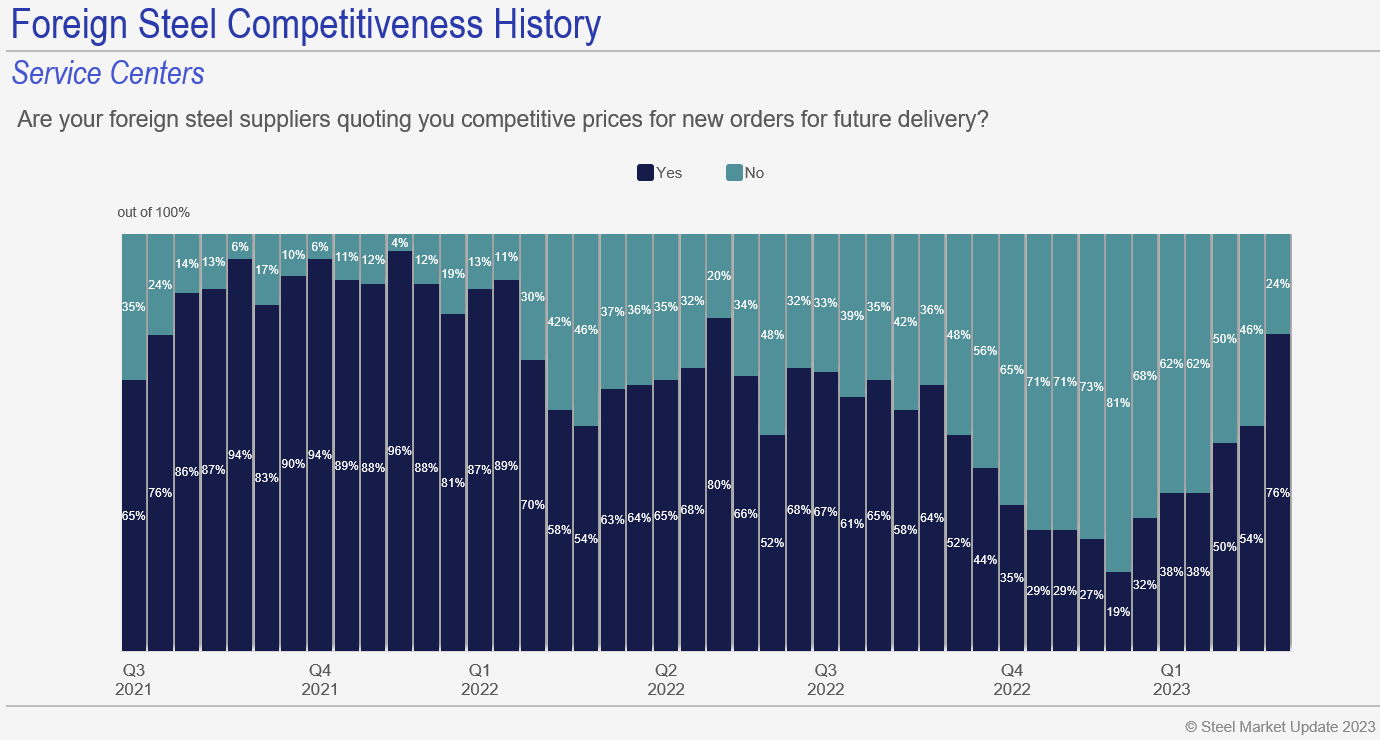

But as US prices have risen faster than global prices over the last few months, so too has the appeal of foreign steel:

Roughly three-quarters of service center respondents to our survey now say they find import pricing compelling. Up from ~50% a month ago and up sharply from ~20% in November of last year.

Offshore steel might not arrive until July or August depending on the product or country of origin. We’ve heard, for example, that hot-rolled coil is available in July at competitive numbers from East Asia, Southeast Asia, and Europe.

It’s a similar story on coated products for August delivery to US ports, with material from East Asia and Southeast Asia said to be much cheaper than domestic offerings.

And with US lead times long, the risk associated with foreign steel is less than it would be normally. Will US mills reduce lead times and prices to be competitive with foreign offerings? We’ll see.

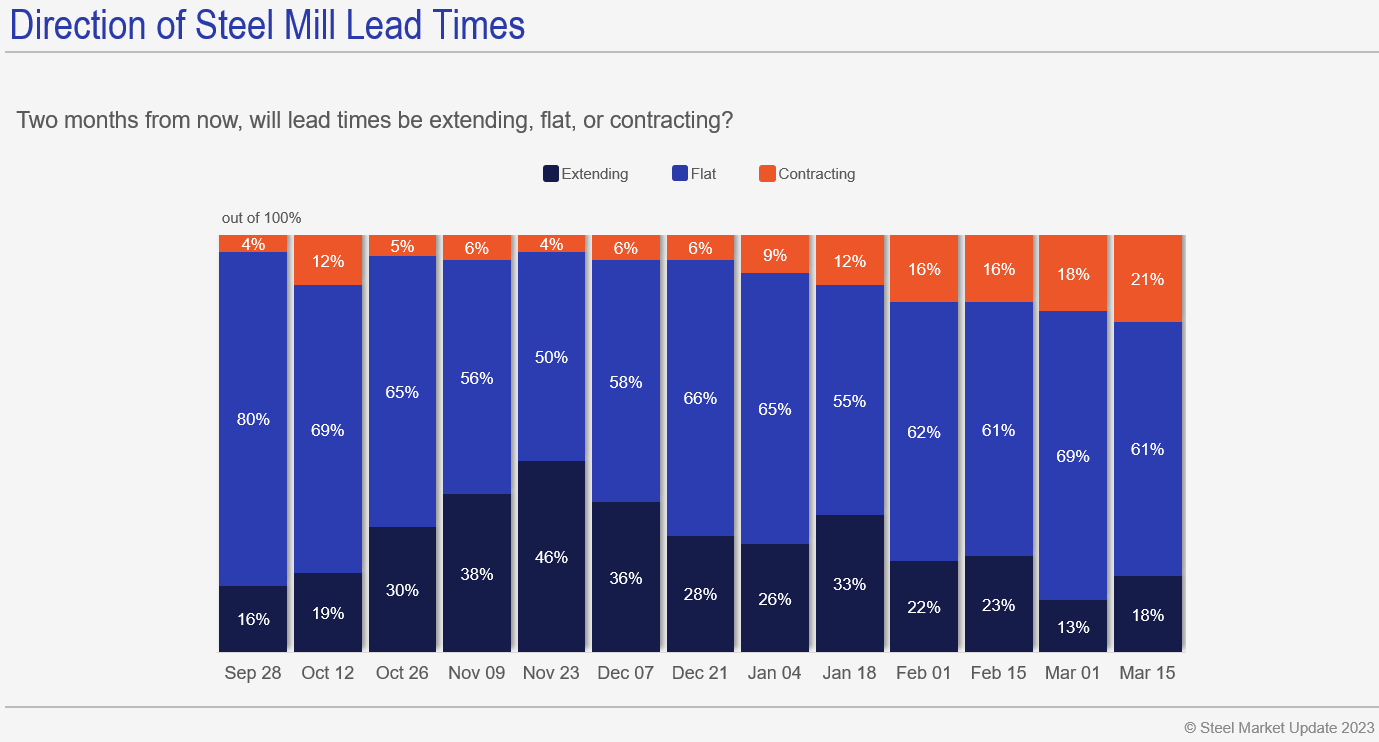

An increasing number of respondents to our surveys think that lead times will be shorter two months from now:

I also like the chart above because you could make the case that it was one of the earliest indicators of the current rally.

In November, even as prices were falling to their lowest point in almost two years, nearly half of respondents were predicting that lead times would be extending in two months. We’ve more recently seen a partial reversal in that trend.

So will US consumers actually pull the trigger on import buys even if they find pricing compelling now? Note I’m talking here about the kind of buys big enough to put a hole in a domestic mill order book.

To answer that, I think we should circle back to some of the concerns about the broader economy.

Take the bailout (let’s call it what it is) of Silicon Valley Bank (SVB) as well as troubles at First Republic and Signature. It’s not just a US story. Abroad, Credit Suisse was taken over by UBS.

SVB is mostly a tech story. You could make the case that Credit Suisse is mostly a European story. But I think it’s fair to say that as scrutiny of regional banks increases in the US, steel might have more exposure.

Even if there are no more runs, it’s probably fair to say that banks will tighten lending standards and slow the pace of lending. Will it be harder for steel consumers to extend lines of credit? And how might that impact a service center trying to restock at higher prices?

I’d be interested to know your thoughts. In the meantime, thanks from all of us at SMU for your business!

By Michael Cowden, michael@steelmarketupdate.com