Prices

May 25, 2023

Midwest HRC Futures Hit Lower Lows as Global Ferrous Complex Dives

Written by David Feldstein

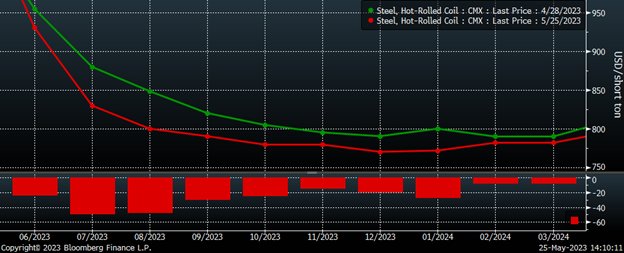

CME Midwest HRC futures continue to be under pressure. Every month from June through March has declined since the start of May. The July and August futures were hardest hit, dropping $50 and $53, respectively, through today’s close. These two months outpacing the others lower has flattened the curve.

Editor’s note: SMU Contributor David Feldstein is president of Rock Trading Advisors. Rock provides customers attached to the steel industry with commodity price risk management services and market intelligence. RTA is registered with the National Futures Association as a Commodity Trade Advisor. David has over 20 years of professional trading experience and has been active in the ferrous derivatives space since 2012.

CME Hot-Rolled Coil Futures Curve $/st

The charts of the July, August, and September futures have broken below their respective uptrends that were established following last November’s low. The July and August futures continue to make lower lows, while the September futures is sitting at its May 11 low at $790.

August CME Hot-Rolled Coil Future $/st

Prices of steel and ferrous raw materials are crumbling globally. This chart shows the North European and Chinese HRC futures as well as LME zinc futures. As you can see, they are trading to lower recent lows, having fallen dramatically over the past few weeks.

Rolling 2nd Mo. North European HRC (wh) $/st, Chinese HR (red) $/st & LME 3-Mo. Zinc

After attempting a rally that took it just above $108/t last week, the rally in iron ore failed quickly diving back to $95. The rolling second month Turkish scrap future fell to a lower recent low on Wednesday, settling at $358/t. Optimism that Europe and China would rebound in 2023 has been slowly on the slide, but this week that slide has shifted to more of a chute. It didn’t help that Germany announced earlier today they have officially entered into a recession, with output contracting in Q4 2022 and Q1 2023.

Rolling 2nd Month Iron Ore (wh) & Turkish Scrap (red)

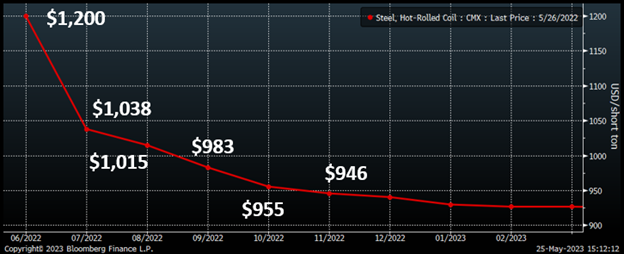

Midwest spot prices are declining while mill lead times shrink. Rumors of sharply discounted tons have been well documented in SMU. However, the HRC futures curve is at $800, which means the CRU has to drop $250-300 just to get to where the futures from July forward are trading at today. So where do we go from here? For some insight, let’s take a look at what happened last year.

One year ago, the July future was $162 below the June future, which was at $1,200. However, the space between each month after July quickly narrowed. The August future was $23 below the July future and $32 above the September future.

CME Hot-Rolled Coil Futures Curve $/st

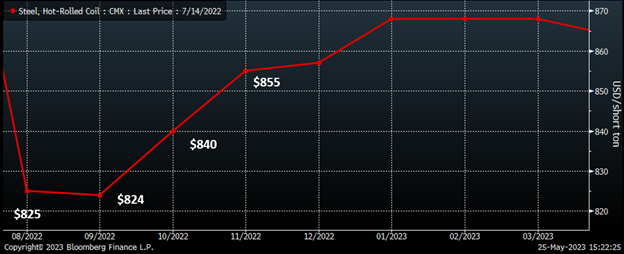

One month later on June 28, the curve had flattened from August forward. August had dropped $130 from May 26 to June 28. August would then decline another $60 by July 14 to $825, $190 in all. During that seven-week period, the curve had shifted from backwardation to flat to contango. The August future was $69 above the November future on May 26 and $30 below the November future on July 14 for a $99 swing in the relationship between these months. This is an example of basis risk. Will we see it play out like this again in 2023?

CME Hot-Rolled Coil Futures Curve $/st

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Feldstein should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.

By David Feldstein, Rock Trading Advisors