Prices

June 8, 2023

Futures: HR Prices Continuing Sluggish Reversion to the Mean

Written by Jack Marshall

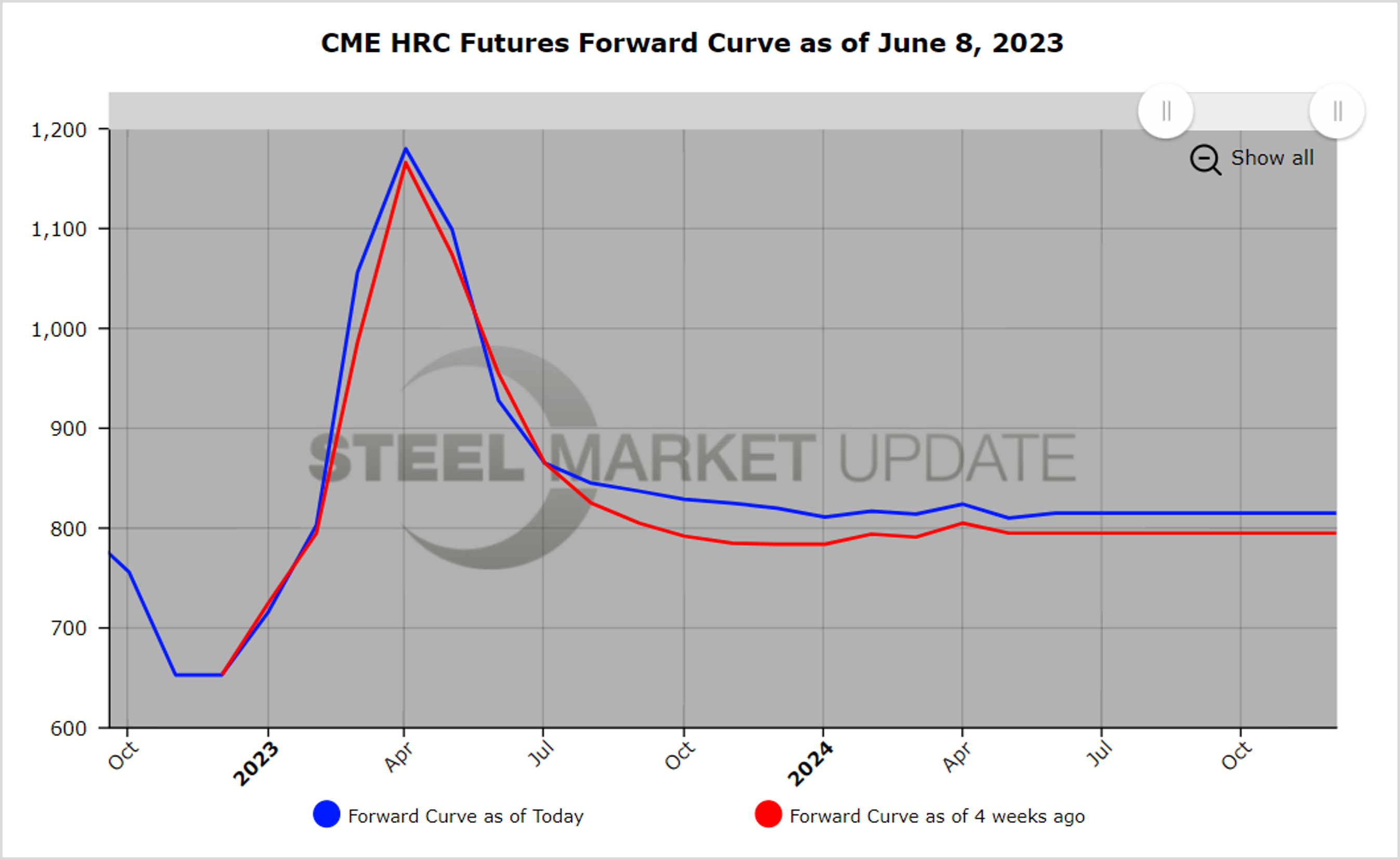

Go figure, in the last month, HR spot has continued to decline. The index tied to CME HR futures has given up $140/ST ($1,130/ST to $990/ST). A look at the fundamentals would appear to support the latest market direction. The list includes declining steelmaking component prices (zinc, coking coal, iron ore and scrap), a sharply lower May Chicago PMI—down for the seventh consecutive month (40.4)—another down month for ISM Manufacturing in May (46.9), and a tepid Fed Beige Book.

Of particular concern from May ISM was the new order component, which contracted at a faster rate and the continuing contraction of the backlog orders component. The data seem to bear out Q1 concerns that the demand in the middle of 2023 would contract due to Federal Reserve tightening and reduced liquidity. While automotive demand might be a bright spot year to date, along with a slow uptake on steel imports due to fear of continued price declines, the HR curve still is pricing in a further $150-$200/ST decline.

However in the last month settlements for the Jul’23 to Jun’24 HR strip average have increased over $20/ST ($803/ST to $825/ST) as macro buyers come in on the back end of the curve.

Will demand going into the latter half of the year match up with the additional steelmaking capacity that should be coming online? The latest American Iron and Steel Institute production figures suggest the producers are managing outputs to match current sluggish demand. With the exception of a few pockets, it appears that commercial demand has been slow and inventories remain fairly tight.

Commercial HR hedge interests have been pretty light this past month, with a slight uptick in volumes in the first week of June. The flat nature of the curve and the rising back end of the curve will further contract HR hedge volumes from commercial interests. Open interest reached almost 30,000 contracts in May before the front month rolled off.

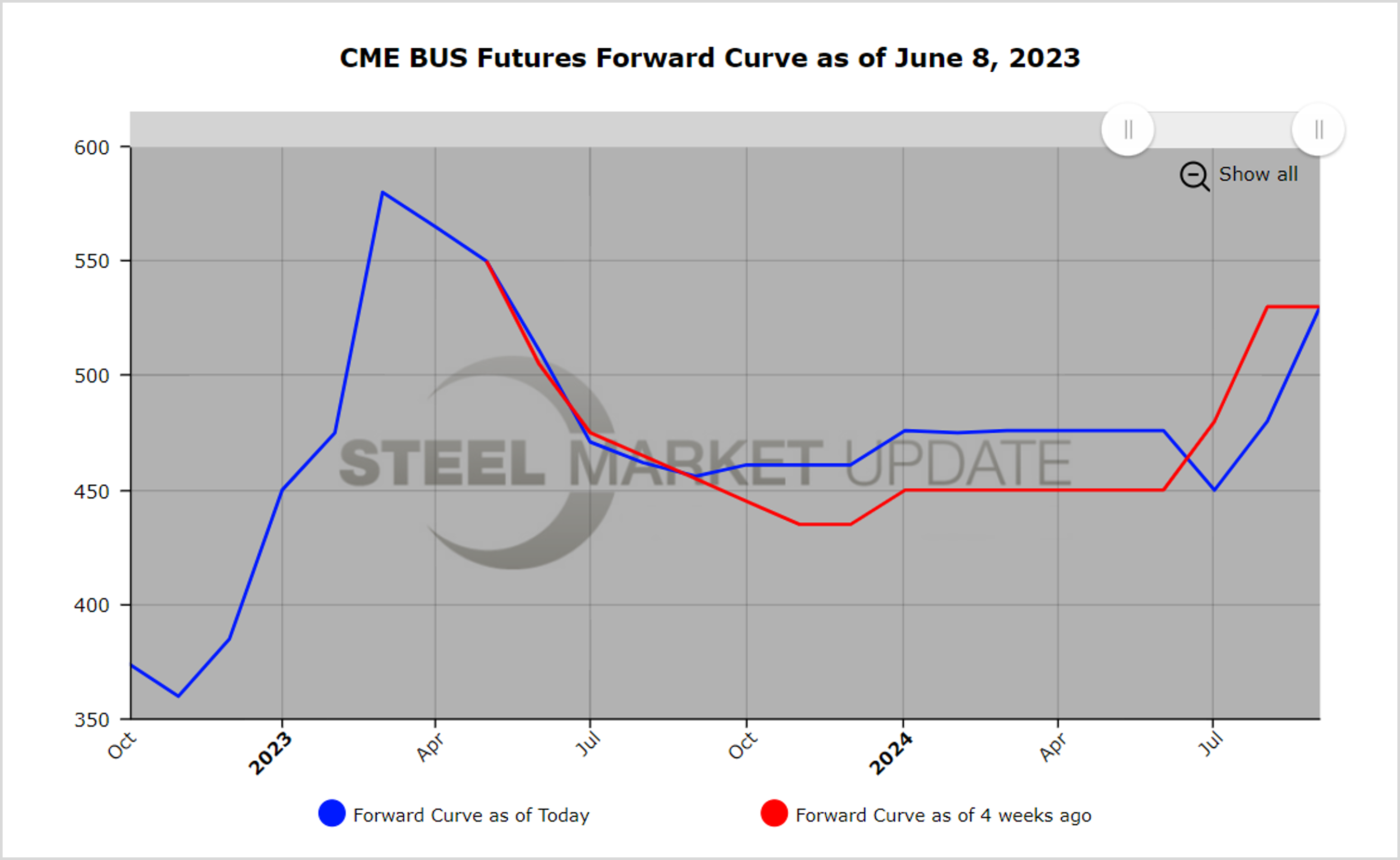

Initial expectations for Jun’23 BUS settle suggested soft sideways to down slightly, but over the last few weeks a more bearish sentiment kicked in, and current Jun’23 BUS futures are trading at $511/ST ($550 -$511 = down $39/GT from May’23 settlement). This year BUS spot has been slow to retrace after the first quarter. It has proven to be very sticky at the mid-$500 level, but with pig iron trading at the $515-520/ST recently and slow demand for scrap exports some gradual decline is expected.

Recent lower prices for obsolete scrap are hurting scrap collections, and new production capacity could limit the price declines in BUS going forward should HR demand pickup. Some of this expectation can be seen in the uptick over the last month in average price of the H2’23 BUS futures, which on a settlement basis are up just shy of $15/GT.

Editor’s note: Want to learn more about steel futures? Registration is open for SMU’s Introduction to Steel Hedging: Managing Price Risk Workshop. It will be held on April 26 in Chicago. Learn more and register here.

By Jack Marshall of Crunch Risk LLC