Market Data

September 12, 2023

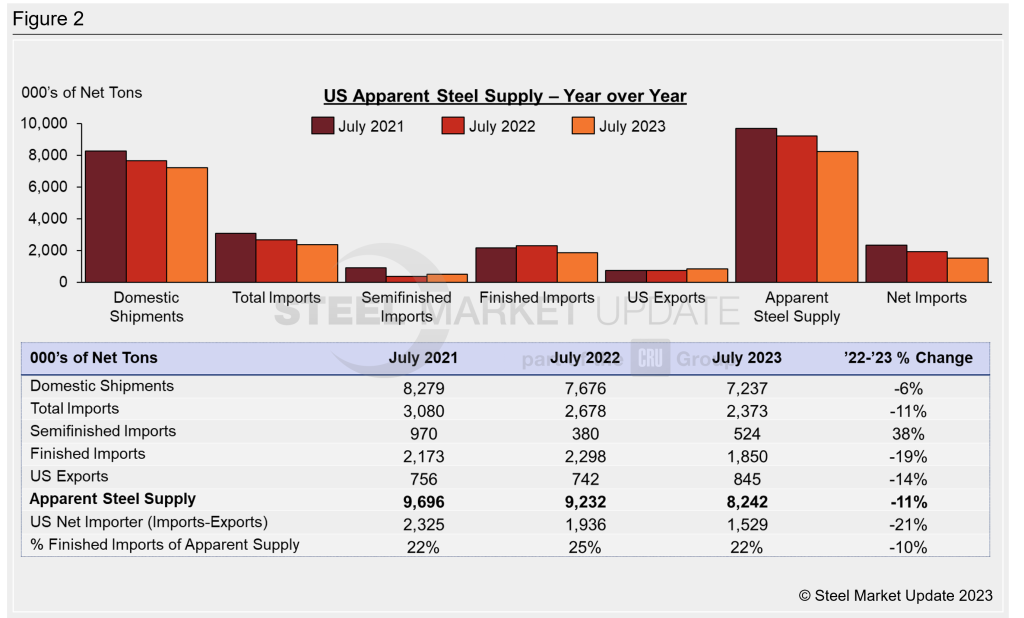

Apparent Steel Supply Edges Down in July

Written by David Schollaert

US apparent steel supply declined 2% in July to 8.28 million net tons compared to the previous month, according to data from the US Department of Commerce and the American Iron and Steel Institute (AISI).

Apparent steel supply is determined by combining domestic steel mill shipments and finished US steel imports, then deducting total US steel exports.

July’s apparent supply total was 952,951 tons lower than the same month one year prior when supply stood at 9.23 million tons. Figure 2 shows July trade statistics year over year (YoY) for each of the past three years.

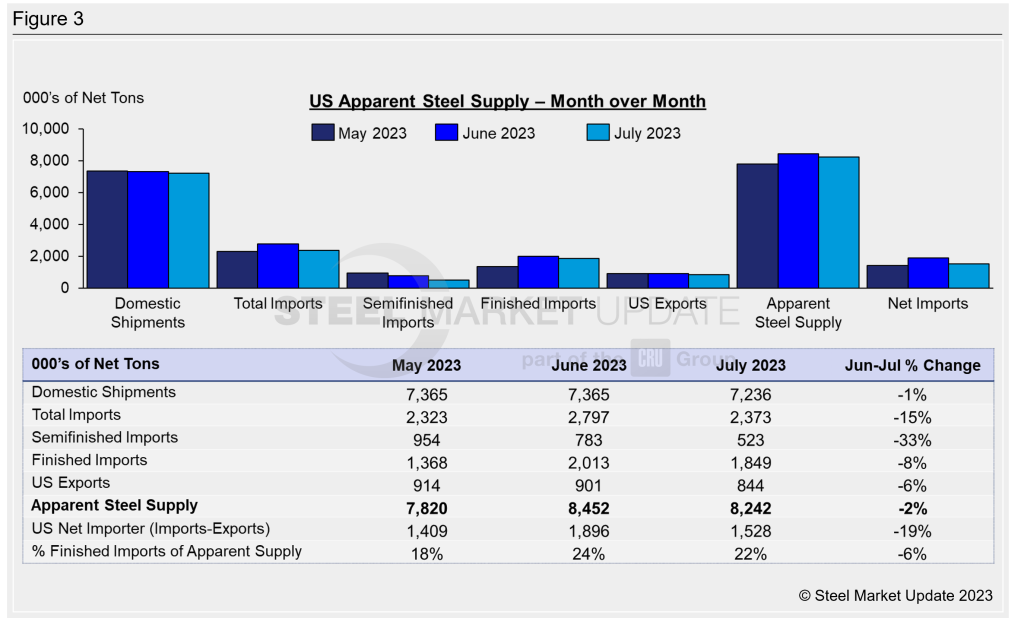

Apparent steel supply has fluctuated for much of the year, ending slightly lower in July. Despite the month-on-month decline, apparent steel supply has remained well above its low of 7.5 million net tons seen in February. Figure 3 shows monthly statistics over the last three months.

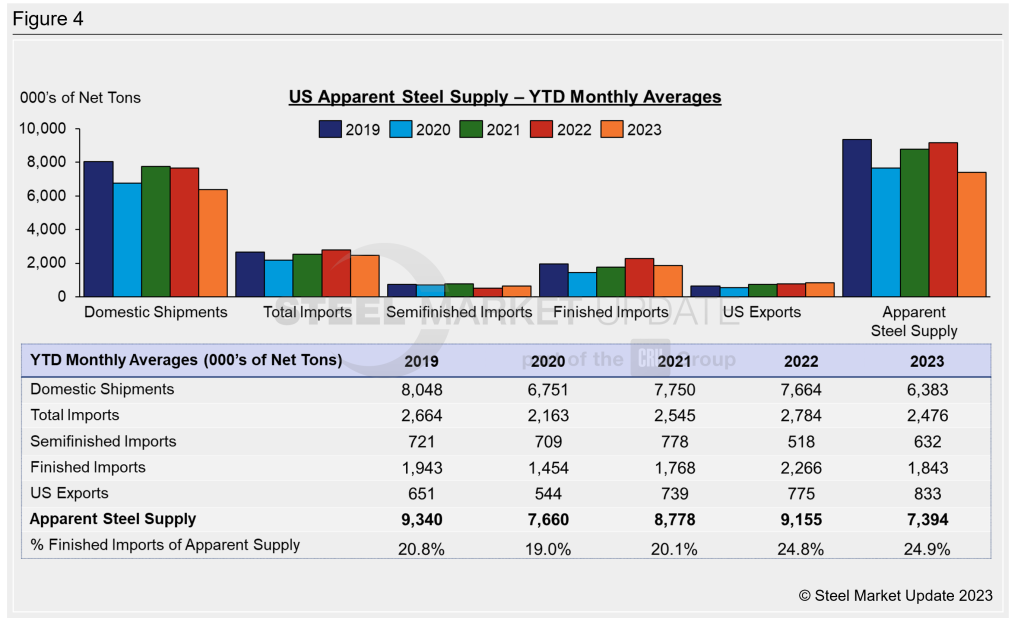

Figure 4 shows year-to-date (YTD) monthly averages for each statistic over the last five years. The average monthly apparent supply level for 2023 thus far is 8.15 million tons.

To see an interactive graphic of our Apparent Steel Supply history, click here. If you need any assistance logging into or navigating the website, contact us at info@steelmarketupdate.com.