Market Data

January 18, 2024

SMU survey: Sheet buyers find mills more willing to talk price

Written by Ethan Bernard

Domestic buyers of steel sheet said mills were much more willing to negotiate spot pricing this week, according to our most recent survey data.

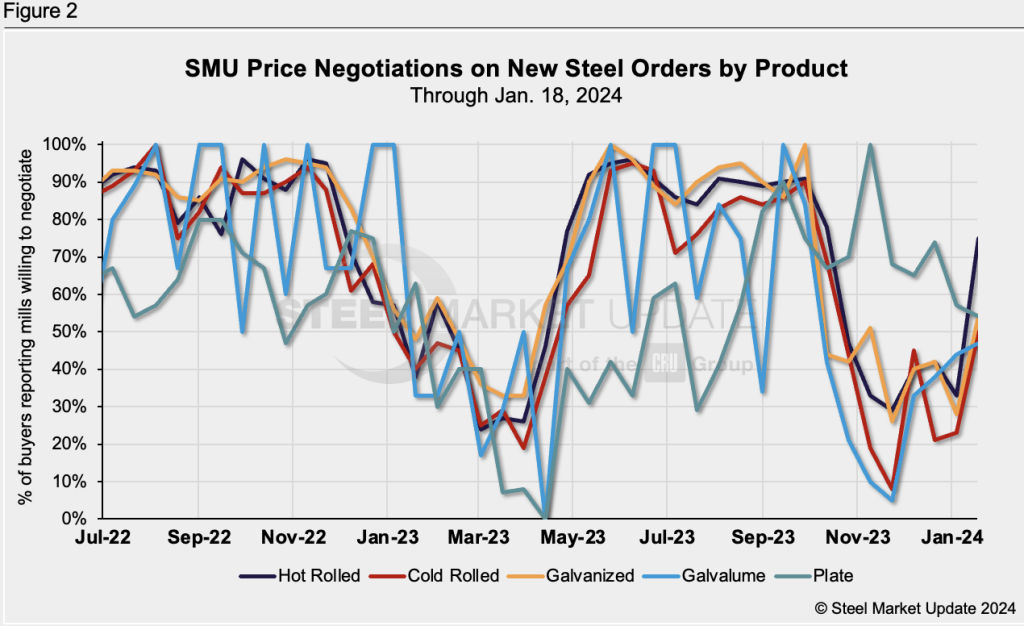

Hot rolled’s negotiation rate jumped a whopping 42 percentage points to 75% from two weeks ago. This comes amid falling hot rolled prices. This week, hot rolled tags tumbled $25 week over week to an average of $1,025 per ton as of Tuesday, according to SMU’s most recent pricing.

Meanwhile, buyers of plate products said mills were slightly less willing to talk price. The mill negotiation rate for plate fell three percentage points to 54% vs. two weeks earlier.

Every two weeks, SMU asks steel buyers whether domestic mills are willing to negotiate lower spot pricing on new orders. This week, 56% of participants surveyed by SMU reported mills were willing to negotiate prices on new orders, soaring from 40% at the last market check (Figure 1). We have to go back to October to find a rate above 50%.

Figure 2 below shows negotiation rates by product. Cold rolled’s rate jumped 27 percentage points to 50% from two weeks earlier, galvanized’s rate increased 26 percentage points to 54%, and Galvalume’s rate inched up three percentage points to 47% in the same comparison. We have averaged Galvalume with the previous market check because of fewer market participants and to reduce volatility.

Here’s what some survey respondents had to say:

“(Mills are willing to negotiate on hot rolled) but quietly, and not across the board.”

“I think for larger buyers (of hot rolled), you can find an opportunity to be better than the advertised spot.”

“(Mills are willing to negotiate on hot rolled), depending on thickness and quality.”

“Large volume buys (on galvanized) may be open to negotiation.”

“Sitting out Galvalume peak of market.”

“(Mills are willing to negotiate on hot rolled), and getting more aggressive.”

Note: SMU surveys active steel buyers every other week to gauge their steel suppliers’ willingness to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website.