CRU

March 3, 2024

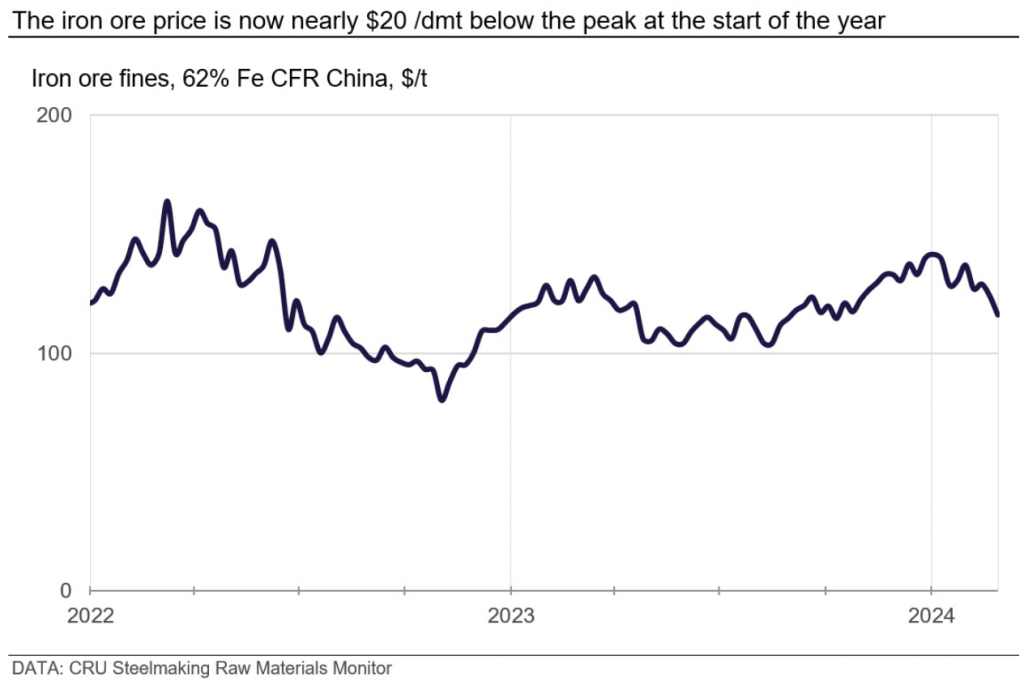

CRU: Iron ore prices down to four-month low on growing pessimism

Written by Liz Gao

Price update

The strong resilience of iron ore prices has come to an end with the weak steel performance worldwide and significantly improved iron ore availability in China. This price fall has occurred as we have seen plenty of short-term iron ore supply disruptions, but the market remains well supplied, especially considering the rising inventory in China. As much of this this supply returns to the market in the coming months, we expect further pressure on iron ore prices, and we have lowered our 2024 price forecast from $117 per dry metric ton (dmt) to $115/dmt.

Iron ore prices were lower than expected in February, and the market is considerably more bearish than one month ago. There are a few reasons for this shift:

- Market conditions in the global steel industry have remained poor. Southeast Asian mills are struggling and steel prices in both Chinese exports helped to keep steel production elevated in 2023, but with weakening global demand for steel, it is making it more challenging to maintain this high level of steel exports.

- Diminishing optimism in China. Continued pessimism in China has pushed steel prices down further in the weeks between Chinese New Year (CNY) and the ‘Two Sessions’ meeting in early March. Consequently, iron ore prices have declined due to the weak steel demand and continued poor margins. Steelmakers are losing confidence in whether possible stimulus measures in the ‘Two Sessions’ would provide any boost to the market. As a result, they are hesitant to place orders on iron ore, contributing to weak buying activities in the spot market.

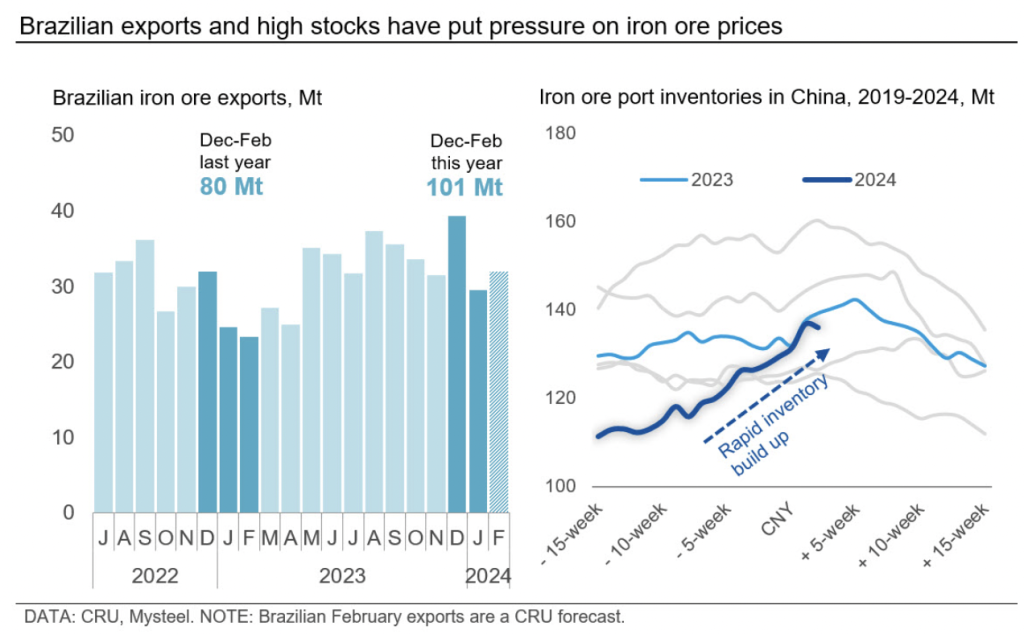

- As for iron ore availability, there is currently no shortage of the material accessible to steelmakers in China despite ongoing supply disruptions. In 2024, iron ore inventories in China have risen rapidly, both at ports and mills. In addition, offshore inventories outside the Chinese coast is now at its highest level since February 2022 due to poor weather conditions disrupting offloading activities. What is even more interesting is that this price fall has occurred despite numerous reported supply disruptions, mainly in Australia and Sweden. This is a sign that the market is currently well supplied and steelmakers are now less concerned about iron ore availability in the short term. Another factor alleviating the pressure on iron ore availability is Brazil’s outstanding export performance in recent months.

Outlook: Prices to be rangebound in coming months

In our view, iron ore prices are expected to be rangebound in March, given the weak demand, ample supply, and high inventory levels in China. These are things to pay attention to in March:

- Expected supply returning from Australia. As peak months of cyclones have passed, the likelihood of cyclones is decreasing as we approach the end of Q1. Improved weather conditions will likely facilitate iron ore shipments in March.

- The upcoming ‘Two Sessions’ (March 4-5) remains the swing factor for iron ore prices. Upside risks exist if China introduces robust stimulus measures. However, we remain cautious regarding the cascading impact on steel demand.

- The construction season in China typically starts around March, with steel and iron ore consumption expected to seasonally recover. Therefore, iron ore consumption in China will certainly be higher in March compared with February.

The next edition of CRU’s Iron Ore Market Outlook will be published at the end of March 2024. Until then, subscribers to the publication can monitor the latest developments in the iron ore market through CRU’s weekly Iron Ore Dashboard.

This article was first published by CRU. Learn more about CRU’s services at www.crugroup.com/analysis.