Analysis

May 22, 2025

CRU: Global sheet prices remain under pressure as exporters undermine domestic markets

Written by Ryan McKinley

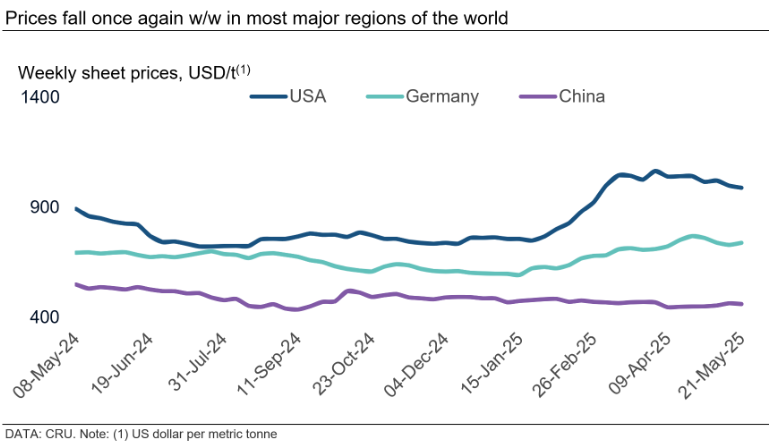

Global sheet prices in many major markets were again under pressure this week.

One cause of this was increased competitiveness from imports that have put pressure on some domestic producers. The European market was a good example that highlighted this trend. There, a variety of competitive import offers from both Turkey and countries in East Asia have helped add pressure to an already weak market.

Indian producers likewise faced increased competition from exporters in other countries in Asia despite safeguard duties, and discounted Russian material is also making its way into that market.

Meanwhile, attractive import offers played a more limited role in price falls seen in the USA. While import offers into the country are lower than current domestic pricing, there is hesitancy among buyers to strike import deals as domestic prices continue falling and because lead times from domestic mills are very short.

In China, value-added product prices rose due to ongoing government stimulus measures that has supported demand across key industries.

USA

Sheet prices fell this week in the US on plentiful supply availability and weakening demand. Our third May assessment for HR coil was down by $8 /short ton (st) week over week (w/w) to $898/st, while CR coil declined by $16/st to $1,109/st. HDG coil base prices fell again w/w, dropping $22/st w/w to $1,032/st.

Purchasing activity has continued to wane, and this trend is expected to continue over the near term. With demand from end users weakening, buyers are limiting purchases in anticipation of further price falls and because of short mill lead times.

Market participants report that HDG coil availability remains particularly high, especially for HR-coil based products. This trend appears to be reflected in the pace of price declines during the past month. Indeed, compared to four weeks ago, HDG coil prices have dropped $90/st, while those for HR coil and CR coil have fallen by $48/st and $11/st, respectively.

The general sense among market participants is that demand is unlikely to pick up over the near term, thus generating rather bearish market sentiment among buyers and producers alike. As domestic producers increase competition for deals, import offers simultaneously remain attractive relative to current domestic price levels, adding to downward pressure in the market.

Our view is that while prices will drop over the near term, the floor of the market has been reset to a higher level due to tariffs. Inventory levels will take a while to work lower, but eventually will reach a point where restocking activity will need to occur. At that point, a buying resurgence should begin supporting the market. The question now is when this next phase of the restocking cycle will occur.

Europe

European sheet prices were stable-to-down this week as weak spot market activity and competitive import offers weighed on the market. German and Italian HR coil were assessed at €657/t and €621/t, down by €1/t and €5/t, respectively.

Prices remained mostly stable, though downward pressure is mounting in both northern and southern Europe. Buyers largely held off on purchases, limiting activity to immediate needs only.

On the supply side, availability remains sufficient. Some domestic mills have short lead times (3-4 weeks) for June delivery. The import market has also picked up, with attractive offers available at low prices.

Indonesian HR coil offers were reported at €530/t CIF into Italy, Spain, Poland, and Romania. This is approximately €100/t lower than current Italian spot market prices. These competitive offers continue to gain ground across Europe, adding further downward pressure on prices.

Vietnamese HR coil has been offered at similar levels, with offers heard at €550/t CIF Italy and actual transactions occurring around €530/t CIF. Some Vietnamese mills continue to benefit from no anti-dumping duties, which makes the country more attractive despite being viewed as developing sources with a limited track record in Europe.

Turkish HR coil offers were reported at around €550–€560/t CIF Italy. While no longer the cheapest option, Turkish material remains widely accepted due to its reliable quality, including for automotive applications. Delivery times from Turkey are also shorter than from Asia. For the former, shipments are expected in late-July or early-August, while shipment times for the latter span later into August.

China

Domestic sheet prices were mostly up this week apart from HR coil prices, which fell by RMB20/t w/w. CR coil prices and HDG coil prices edged higher by RMB30/t w/w and RMB10/t w/w respectively. Prices were mainly affected by restocking demand for each product.

With the off-seasonal construction period approaching, restocking demand for HR coil fell, which led to downward pressure on prices. In addition to lower capacity utilisation rates w/w, the output of HR coil output has fallen as a result. Even so, this supply limitation provided only limited upside support and was offset by falling demand.

On the other hand, for CR coil, downstream demand remained robust amid ongoing stimulus support measures. This support from the durable goods trade-in policy has allowed sales in the auto sector to continue showing robust growth in May. Additionally, the 90-day deal on tariffs with the US caused restocking demand for CR coil to pick up, and provided some upside support for overall CR coil prices.

Asia

Prices of imported sheet products in Asia decreased this week on very limited trading activity.

Chinese HR coil was offered at $465-470/t CFR Vietnam for pipe making and commercial grade material, while offers for SAE1006 grade were around $485/t CFR Vietnam. However, there was no buying interest heard in the market. According to market contacts, most buyers booked large volumes of Chinese material ahead of the temporary anti-dumping duties, and rerolling mills have been operating at a low rate because of poor sales in the domestic market. They have also lost out in the export opportunities due to trade barriers.

Some producers are still looking SAE1006 HR coil supply outside of China, but their offers are only at $505-$510/t CFR Vietnam. This was considered to be too low for Japanese and Korean mills.

CRU assessed HR coil at $495/t CFR Far East, down by $5/t w/w. CR coil and HDG coil prices were at $565/t and $585/t CFR Far East, also down by $5/t w/w.

India

Indian domestic sheet prices fell by INR300–700 ($4–$8)/t w/w as traders started offering discounts in response to a fall in spot market activity. The price premium of drawing grade CR coil over base grade was unchanged w/w at INR1000–1200 ($12–$14)/t.

CRU understands from market contacts that key buyers in the automotive and appliance segments have sufficient inventory on hand and are thus slow to restock. Meanwhile, some buyers are hopeful of a price reduction in the near term after ongoing maintenance outages at some mills end.

Market participants are also watching trends in the Asian import market, where prices have stayed subdued and have now turned to a discount compared to domestic prices even when factoring in the safeguard duty. A couple of import deals for Russian-origin HR coil were also reported in the middle of May, taking place at a lower price than offers from China. Such bookings have also started putting downward pressure on local prices, alongside persistent weakness in Indian exports.