Analysis

August 24, 2025

Final Thoughts

Written by Michael Cowden

The big show is here again. SMU Steel Summit begins on Monday. This year, like last year, more than 1,500 people will be joining us. And I couldn’t be more excited to have everyone here in Atlanta.

Usually, I’d use my column just before the kick-off of the conference to go through the agenda. This time, I want to draw your attention to a print magazine, which we’re calling a yearbook, you’ll receive when you check in on Monday.

You’ll find exclusive interviews with industry leaders like U.S. Steel President and CEO David Burritt, Reliance Inc. President and CEO Karla Lewis, and Barry Zekelman, CEO and executive chairman of Zekelman Industries.

You’ll also see an article featuring some of our survey work on President Donald Trump’s tariffs. Spoiler alert: They’re not very popular among the steel buyers whom we poll.

The political divide last year was marked by whether you supported Donald Trump or Kamala Harris for president. This year, at least in steel, it seems like the divide might be just as sharp between those for and against tariffs – with mills generally applauding them and steel consumers, not so much.

Speaking of U.S. Steel, I find myself thinking back to past Steel Summits – August 2023 in particular. That year, news that U.S. Steel was for sale exploded into public view just days before Summit started.

The topic was so sensitive that executives from the Pittsburgh-based steelmaker understandably couldn’t speak about it. Not on record on stage. And not off record off state either. By December 2023, the steel world learn that Nippon Steel had submitted the winning bid at nearly $15 billion.

Initially, most analyst reports said the only hurdles to the deal were the usual procedural ones – it was a foregone conclusion. And then it became a political football in 2024, a presidential election year. In fact, it was all but pronounced dead by many analysts and industry observers.

This year, we’re proud to have David Burritt at Summit and speaking very much on the record. It will no doubt be one of the highlights on the first day of Summit on Monday afternoon.

It’s a testament to his grit and determination – and that of everyone else at U.S. Steel and Nippon Steel – that the deal closed earlier this summer. And we’ve also learned that Nippon Steel plans to invest a transformational $11 billion into U.S. Steel.

Again, I would suggest you check out the magazine and read my interview with David. You can learn more about the deal from him, in his own words.

Of course, my colleague David Schollaert and I will start Monday off as we do most years – with live audience polls. I know many of you reading this will be among those attending. So, if you haven’t done it already, please download the SMU Steel Summit app. You’ll need it to participate in those polls.

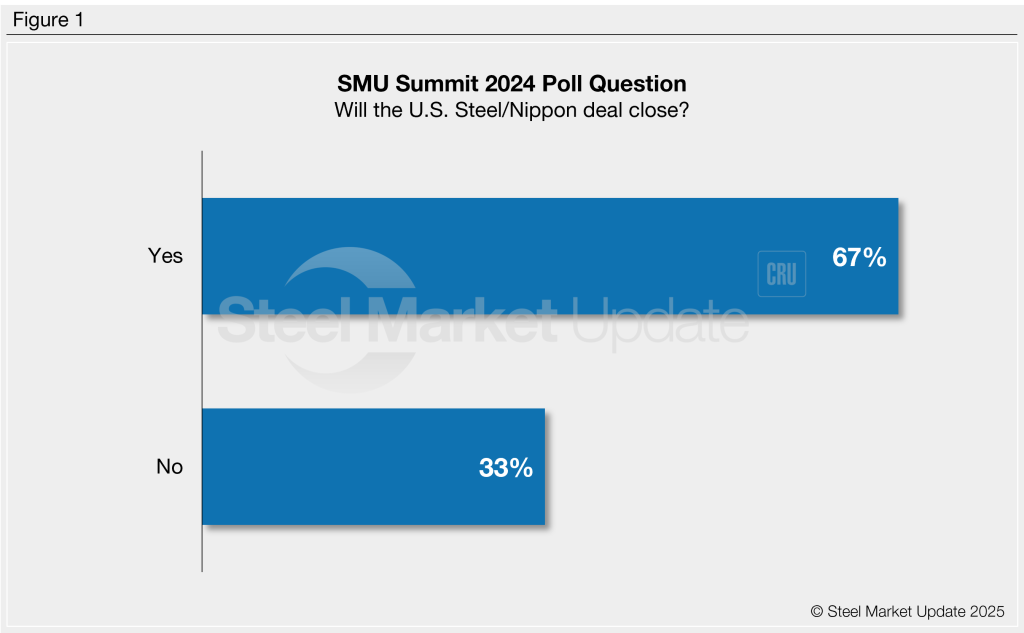

For what’s worth, the Summit crowd was really on the money in the polls last year. As you can see in the chart below, most predicted the Nippon-U.S. Steel deal would close at a time when that was not the consensus view. (Editor’s note: You can click on the images below to expand them.)

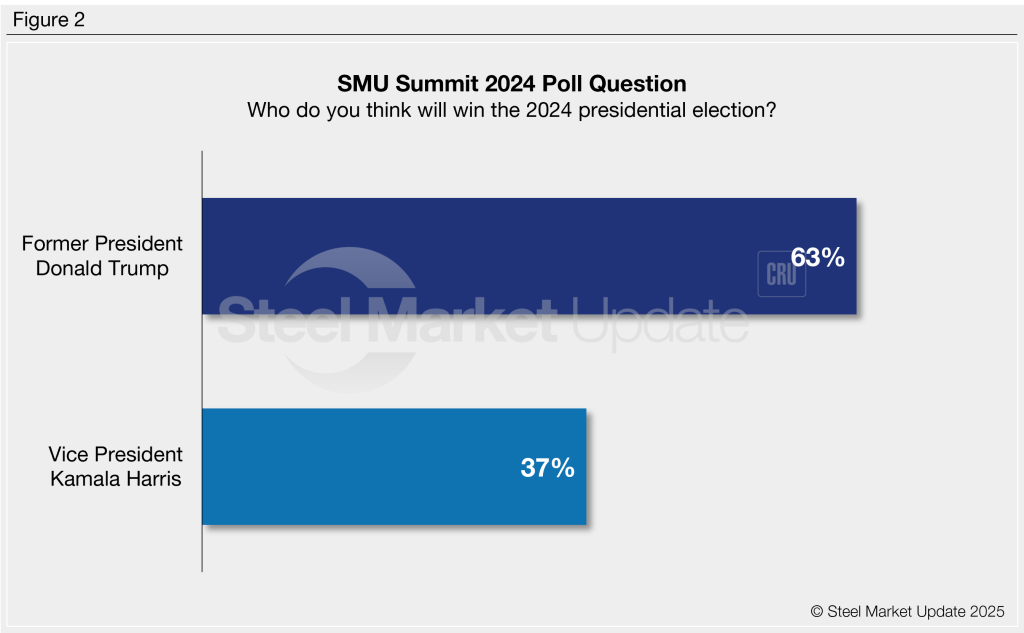

The Summit crowd was also right in predicting that Donald Trump would be the next president at a time when former Vice President Kamala Harris was ahead in the polls.

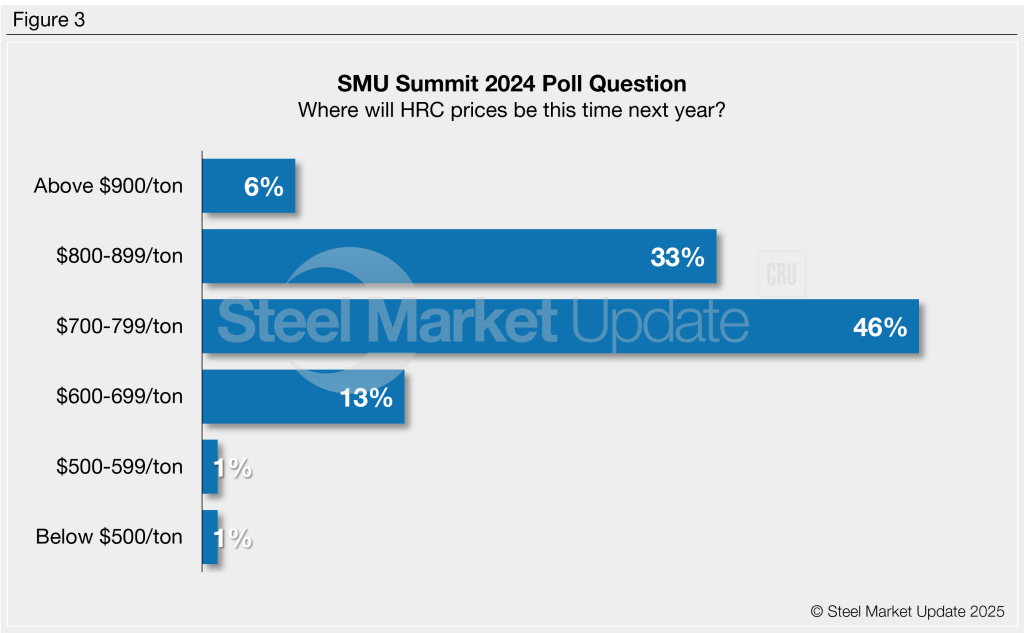

Heck, yinz were even right last year when it came to predicting where prices would be in August 2025, as you can see here.

Most people thought hot-rolled coil prices would be in the $800s per short (st). And, sure enough, that’s where we are now.

I mention that because we’ve been almost laughably bad with such predictions in the past, as I’ve noted in prior Final Thoughts.

In August 2020, for example, the pandemic year that sent Summit virtual, we thought the bad times – HR at around $400/st would never end. A year later, when talk was of HR hitting $2,000/st, we collectively thought the good times would never end – even though lead times were already slipping.

I’d like to say the Summit crowd has the proverbial crystal ball. But I think unexpected changes to Section 232 since Trump’s inauguration are a big part of the reason prices are where they are. And I don’t think any of us were predicting this time last year that S232 would be re-applied to everyone and then increased to 50%.

Why the space theme? To be honest, part of the reason we chose space as a theme for this year’s Summit was because I figured we’d be past politics by now. Trump would have implemented the tariffs he promised so often on the campaign trail. And we’d have moved on to other, bigger topics – like AI, the future of manufacturing, leadership, and the next big catalyst for demand.

But as we’ve seen, Trump’s tariff policies continue to evolve in unexpected ways. When it comes to steel news, late May and June were all about S232 on imported steel increasing to 50% – and speculation about how long they might stick. Much of our July coverage centered around whether the US might hit Brazilian pig iron with a 50% “reciprocal” tariff. And this month, we’ve seen S232 tariffs expanded to include hundreds range of downstream goods. I think some of our speakers will have a thing or two to say about the impacts of this latest tariff move.

We’ll, of course, anchor discussions in more earthly matters too – like how you’re seeing demand shape for the balance of this year and into 2026,

And you in the audience will shape the discussion too. Because we’ll be leaving plenty of time for Q&A. As in years past, you’ll submit questions in the Steel Summit app. You can also upvote the questions you’d most like to see answered.

So, again, download the app. With it, you’ll help us steer the steel rocket ship we’ll all be embarking on together on Monday. Get ready for blast off!

PS – If you still haven’t registered, just show up at the Georgia International Convention Center on Monday. Registration opens at 7:30 am, and we do take walk-ins.