Analysis

August 25, 2025

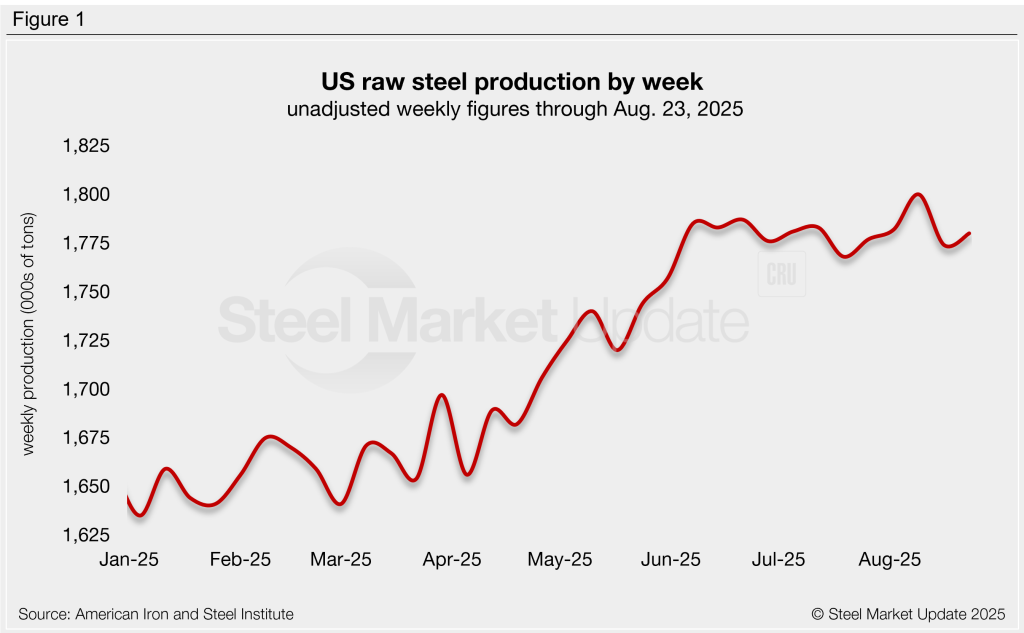

AISI: Raw steel mill production ticks up

Written by Brett Linton

Domestic mill output increased last week, according to the latest data released by the American Iron and Steel Institute (AISI). Production remains historically strong, holding near multi-year highs since June.

Raw steel production was estimated at 1,780,000 short tons (st) for the week ending Aug. 23 (Figure 1). Output increased 6,000 st, or 0.3%, from the previous week, just 20,000 st shy of the three-and-a-half-year high seen two weeks ago.

Last week’s production was 3.7% above the year-to-date (YTD) weekly average of 1,717,000 st and 3.1% higher than the same week a year earlier. YTD output now stands at 57,700,000 st, up 1.3% from the same period of 2024. Recall that in the first half of 2025, production had been trailing 2024 levels. June was the turning point, with annualized output climbing above 2024’s pace.

The mill capability utilization rate was 78.6% last week, higher than both the previous week (78.3%) and the same week last year (77.7%). Across the first eight months of 2025, capability utilization has averaged 76.6%.

Raw production increased week over week (w/w) in four of the five regions defined by AISI:

- Northeast – 125,000 st (up 7,000 st)

- Great Lakes – 535,000 st (down 19,000 st)

- Midwest – 241,000 st (up 4,000 st)

- South – 805,000 st (up 10,000 st)

- West – 74,000 st (up 4,000 st)

Editor’s note: The raw steel production tonnage provided in this report is estimated and should be used primarily to assess production trends. The graphic included in this report shows unadjusted weekly data. The monthly AISI “AIS 7” report is available by subscription and provides a more detailed summary of domestic steel production.