Analysis

May 19, 2026

SMU Price Ranges: Few signs of a peak with demand strong and spot tons scarce

Written by Brett Linton & Michael Cowden

Sheet prices continue to rise in a market that remains characterized by extremely limited spot availability, solid demand, long lead times, and the lowest sheet inventories since May 2021.

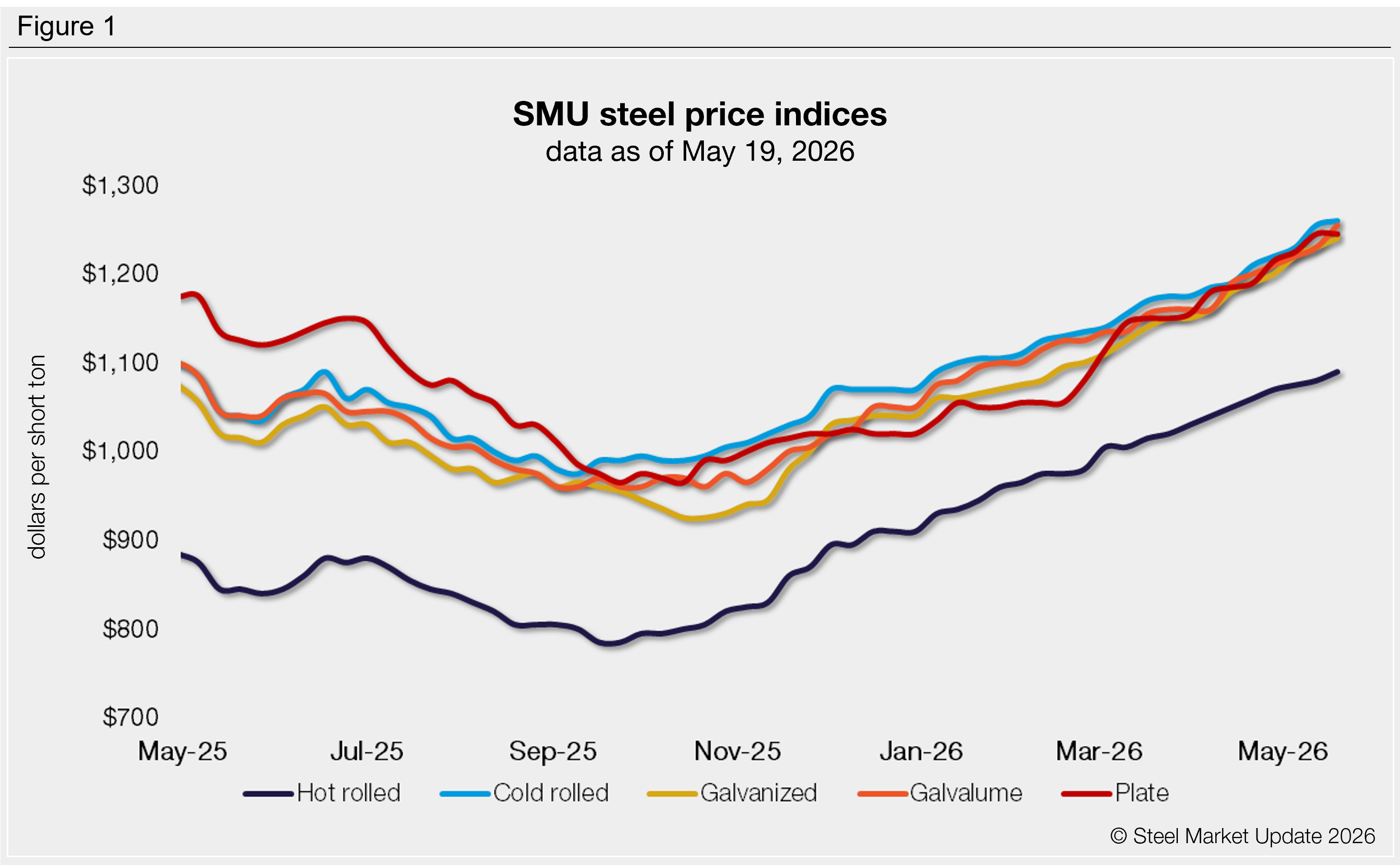

HR on a roll

SMU’s price for hot-rolled (HR) coil now stands at $1,090 per short ton (st) on average, up $10/st week over week (w/w).

HR prices are also at their highest point since early May 2023, more than three years ago.

Some market participants now take $1,100/st HR as a given and think it’s only a matter of time before HR hits $1,200/st. Others said imports could become a much bigger factor in the should US prices go above $1,200 – although a few said foreign tons might be necessary to meet current demand and refill depleted inventories, especially with domestic mills continuing to run late.

CR and coated up too

Cold-rolled and coated prices also increased. CR stands at $1,260/st on average (up $5 w/w). Galv base is at $1,240/st on average (up $10/st w/w). And Galvalume notched the biggest gains at $1,255/st on average (up $25/st w/w).

Plate prices were largely unchanged as the market digests the latest round of price hikes. While some plate mills have announced price hikes, others have kept plate prices unchanged.

What they’re saying

Forty-four percent of respondents to SMU’s last survey reported increasing demand, the highest such reading since June 2021, which was one of the strongest steel markets on record.

But while the current market is hot, some sources noted that demand is not strong across all sectors as it was in 2021 – even if specific sectors, like anything related to data centers and the border wall, are on fire. Some also noted the market is not officially on allocation, as it was for much of 2021. But it can feel that way with buyers often unable to find spot tons (and certainly not in large volumes) and unable to buy to their contract maximums.

While some market participants expressed concerns about buying at or near the peak of the market, others said such caution would only serve to extend the current upcycle.

Momentum

SMU’s price momentum indicator remains at higher for both sheet and plate products, signaling we expect prices to increase further in the short term.

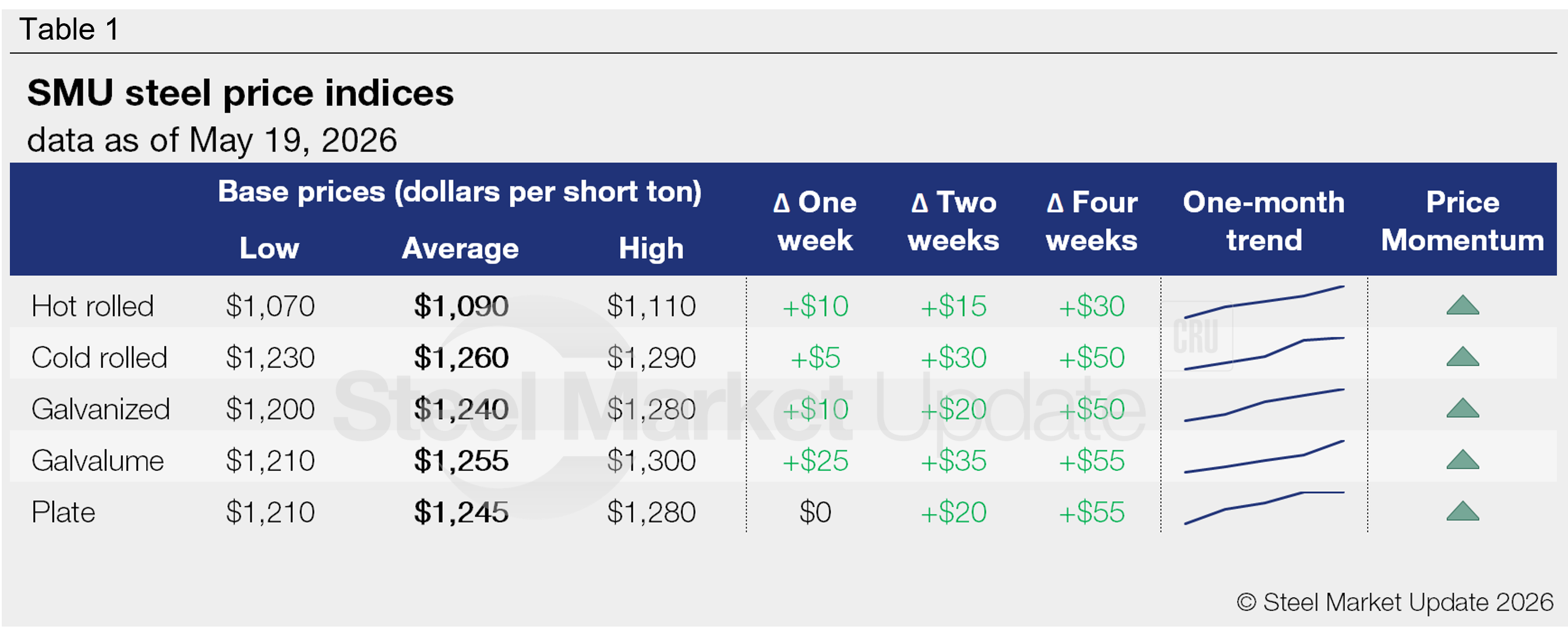

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil: $1,070–1,110/st, averaging $1,090/st

Our entire range is up $10/st w/w.

Hot-rolled lead times range from 5–11 weeks, averaging 7.0 weeks as of our May 14 market survey.

Cold-rolled coil: $1,230–1,290/st, averaging $1,260/st

The lower end of our range is unchanged w/w, while the top end is up $10/st. Our overall average is up $5/st w/w.

Cold-rolled lead times range from 6–11 weeks, averaging 8.4 weeks through our latest survey.

Galvanized coil: $1,200–1,280/st, averaging $1,240/st

The lower end of our range is unchanged w/w, while the top end is up $20/st. Our overall average is up $10/st w/w.

Galvanized .060×48” G90 benchmark: SMU price range is $1,290–1,370/st, averaging $1,330/st FOB mill, east of the Rockies.

Galvanized lead times range from 6–11 weeks, averaging 8.1 weeks through our latest survey.

Galvalume coil: $1,210–1,300/st, averaging $1,255/st

The lower end of our range is up $10/st w/w, while the top end is up $40/st. Our overall average is up $25/st w/w.

Galvalume .0142×42” AZ50, grade 80 benchmark: SMU price range is $1,639–1,729/st, averaging $1,684/st FOB mill, east of the Rockies.

Galvalume lead times range from 6–12 weeks, averaging 8.2 weeks through our latest survey.

Plate: $1,210–1,280/st, averaging $1,245/st

Our entire range is unchanged w/w.

Plate lead times range from 5–8 weeks, averaging 7.1 weeks through our latest survey.

Brett Linton

Read more from Brett Linton