Analysis

April 15, 2026

HRC vs. busheling spread continues to widen in April

Written by Ethan Bernard & Stephen Miller

The spread between domestic hot-rolled coil and prime scrap prices widened again in April, a trend that started back in September.

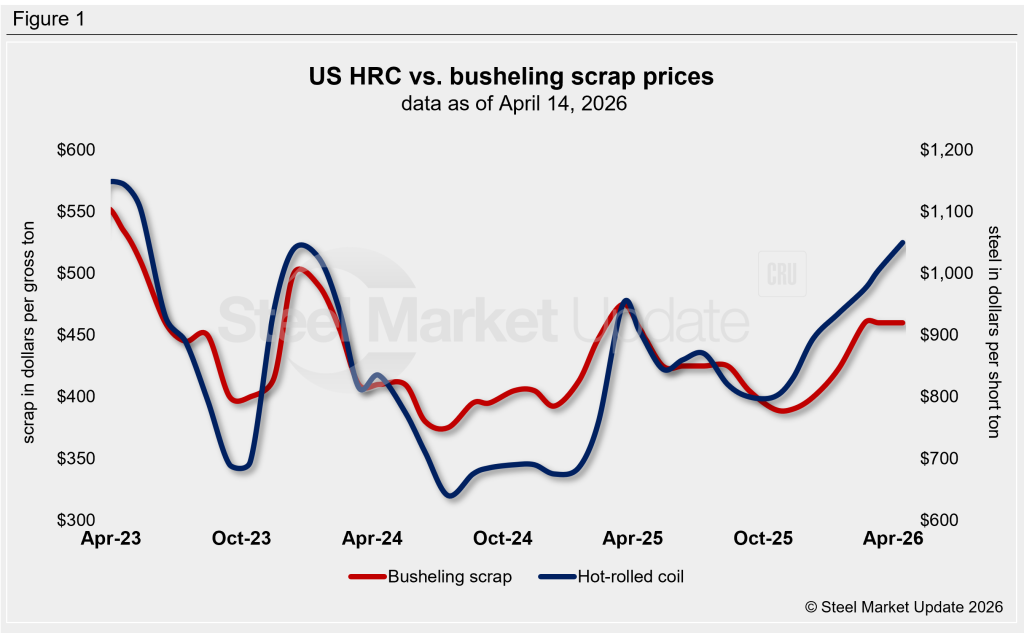

SMU’s average HRC price was $1,050 per short ton, FOB mill, east of the Rockies, as of Tuesday, April 14. That’s up $10/st from the previous week and $35/st from a month earlier.

Meanwhile, busheling tags were flat again in April, averaging $460 per gross ton (gt).

Figure 1 shows price histories for each product.

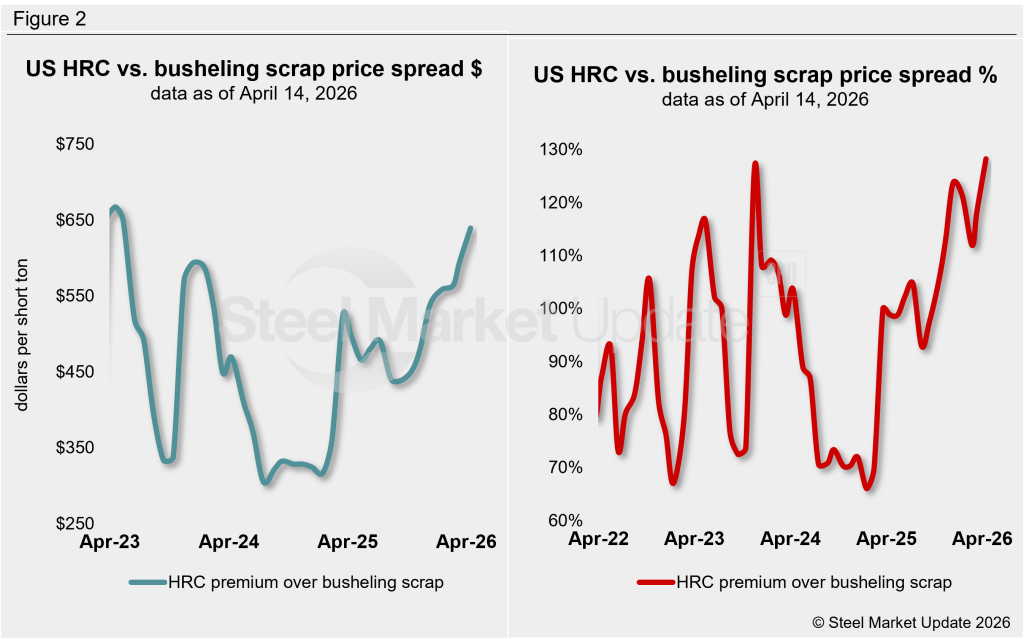

After converting scrap prices to dollars per short ton for an equal comparison, the differential between HRC and busheling scrap prices was $639/st as of Tuesday, April 14. That’s up $45/st from a month earlier. We have to go back to May 2023 to find a mark above this when it stood at $650/st (Figure 2).

What’s going on?

As HRC prices rise, the price of #1 busheling is struggling to keep up. The US scrap market in April was seasonally adjusting downward. But due to several factors, busheling maintained its March price level. This still was not enough to keep the HRC-busheling spread from widening.

One reason busheling traded sideways was that pig iron prices increased and were subject to a $45-50 per metric ton tariff. So, depending on the location of the HRC mill, the cost of using pig iron is well over $120/gt over busheling on a delivered basis.

HRC premium as a percentage

The graph on the right-hand side of Figure 2 shows the spread relationship differently: We have graphed HRC’s premium over busheling scrap as a percentage. HRC prices now hold a 128% premium over prime scrap vs. 118% the previous month.

Ethan Bernard

Read more from Ethan Bernard