Analysis

April 21, 2026

Foreign steel interest rises as buyers confront tight market, higher substrate costs

Written by Laura Miller

North American steel buyers are signaling stronger interest in foreign material amid a tight market and rising global substrate costs, which are complicating purchasing decisions.

A West Coast-based trader with whom SMU spoke described a volatile but active import market. He said Korean mills have suspended some offers due to the Iran crisis and rising domestic demand. Additionally, he reported limited competitive supply of bare galvanized from Korea, Vietnam, Indonesia, and Thailand due to vessel shortages and market disruptions.

Despite the uncertainty, the trader said import interest remains solid: “There’s definitely interest… There’s still a lot of pent-up supply requirements because of delays and production domestically.” He added, “I think this thing has legs.”

A Gulf Coast-based trader wasn’t quite as optimistic. He told SMU the import market is “extremely slow,” and he has started doing more business domestically, both in the US and Mexico. Because, according to him, “imports don’t stand a chance” in this environment.

Let’s take a look at what our latest survey reveals about the current steel trade.

Competitive pricing depends on product and buyer type

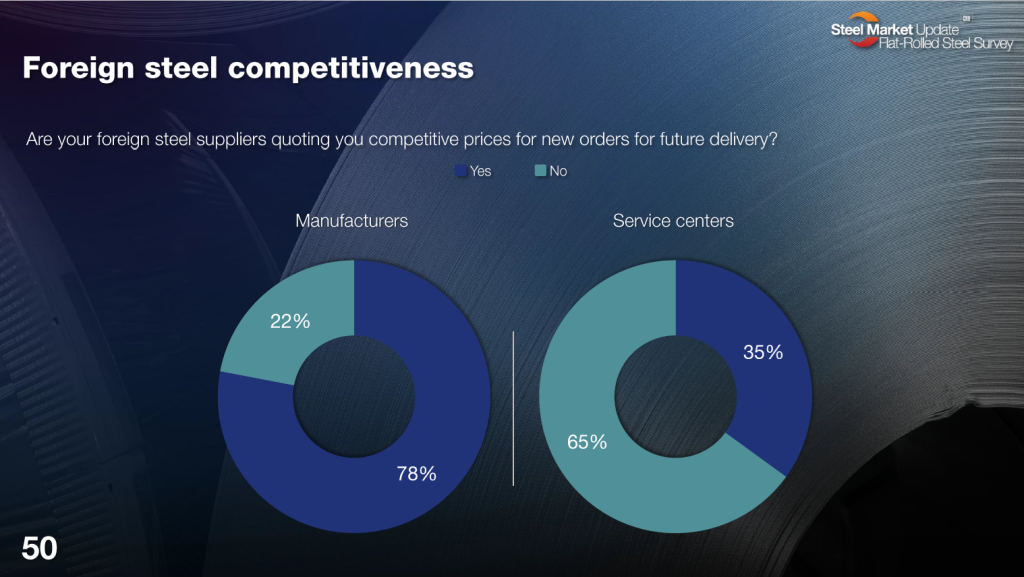

In SMU’s April 17 flat-rolled steel buyers’ survey results, manufacturers reported more favorable foreign pricing than service centers: 78% of manufacturers said foreign suppliers are quoting competitive prices, while 65% of service centers said the opposite, that prices are not competitive (slide 50, below).

Tariffs remain a sticking point for some buyers. One manufacturer in the South said, “Tariffs have prevented cost-effective alternatives.” A national service center source noted that, although offers exist, “those prices are rising also.” Another service center in the Midwest mentioned they are “entertaining offers from several suppliers for August delivery.”

Foreign buying interest growing as domestic prices rise

One service center buyer said they are increasingly considering global options, calling the current moment an “inflection point.”

Domestic steel prices continue to rise, with SMU’s hot-rolled coil price increasing by another $10 this week to an average of $1,060 per short ton (st). Broadly speaking, flat-rolled steel prices have been grinding higher since early Q4 of last year.

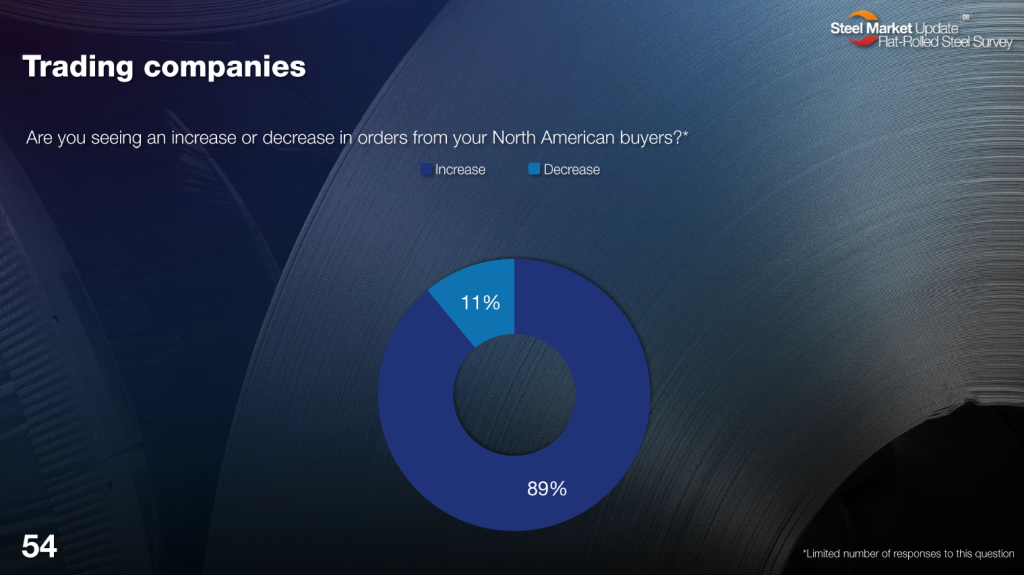

Traders also reported stronger demand from North American buyers, with 89% of those surveyed reporting increased orders (slide 54, below), up from 57% the previous week. One trader mentioned there is “more interest in all products now, including imports.”

Most buyers not placing new foreign orders

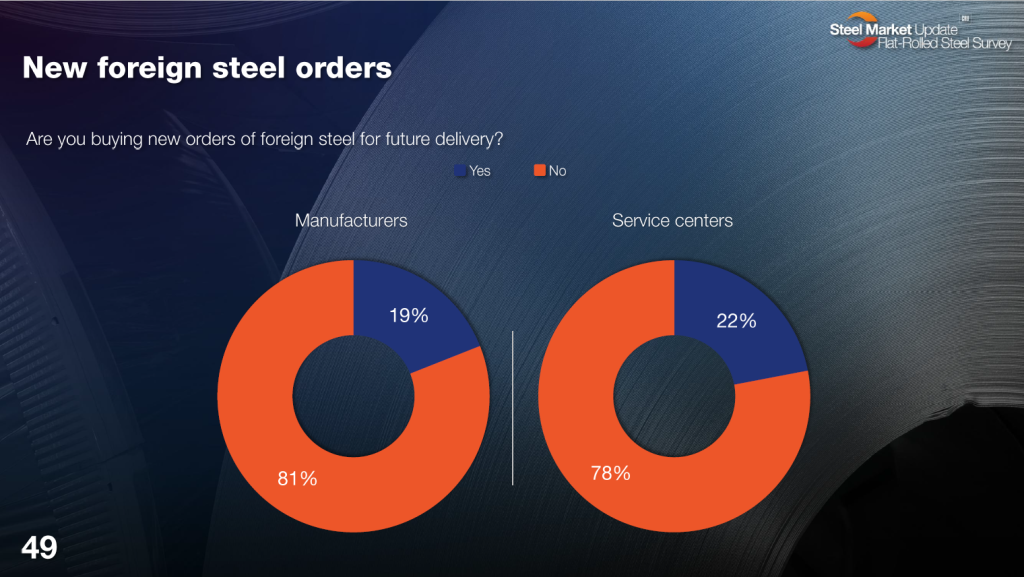

However, a majority of manufacturers (81%) and service centers (78%) surveyed said they are not placing new foreign steel orders for future delivery (slide 49, below). Long lead times and tariffs remain deterrents. Of note, the number of service centers reporting making new foreign steel orders increased by five percentage points from the previous week to 22%.

One Canadian manufacturer pointed to tariff-rate quota (TRQ) constraints in his country, saying, “TRQ fills up before the actual quarter is open… There appear to be loopholes that were not clear to everyone prior to TRQs being established.”

Import offers are attractive

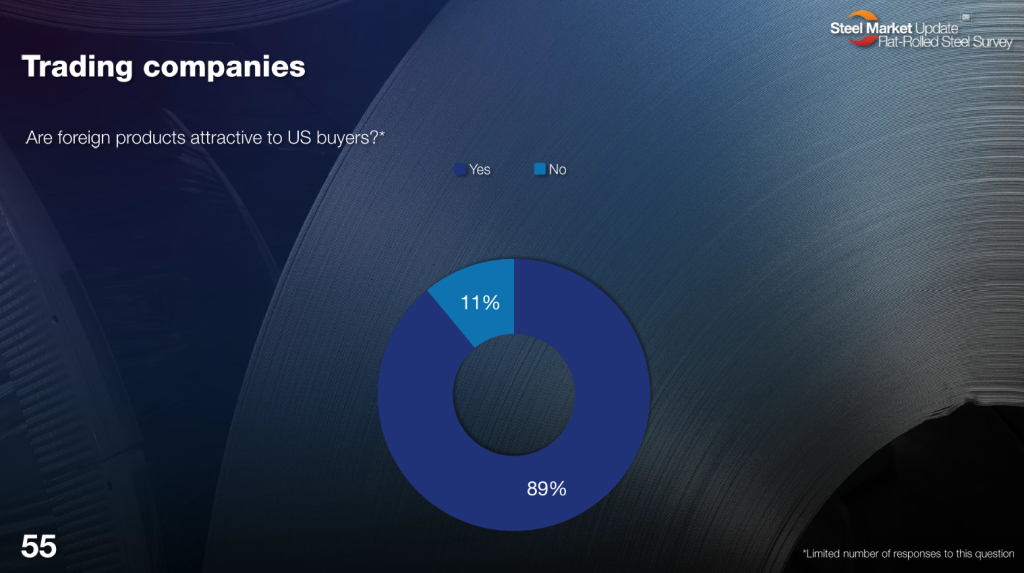

Still, foreign products remain broadly attractive to US buyers – 89% of traders said yes, their offers are attractive. But product differentiation matters. As one trader put it: “Bare galvanized is not. Pre-painted and hot rolled, yes.”

A trader based in the Midwest reported painted Galvalume offers from Korea at $2,200 per metric ton ($1,995/st) DDP US port. SMU’s April 21 price assessment pegged bare Galvalume products at an average of $1,200/st ($ /mt) FOB domestic mill, up $10/st from the week before and $40/st from two weeks earlier.

One buyer at a Midwest service center said more imports are needed to bring domestic pricing down from its current rally. “I believe foreign will need to start arriving before mills move off their pricing,” they commented. Flat-rolled steel imports in February hit their lowest measure in SMU’s seven-year data history, falling 41% below their 2025 monthly average.

Mixed competitiveness across product categories

Survey responses show uneven competitiveness across sheet and plate.

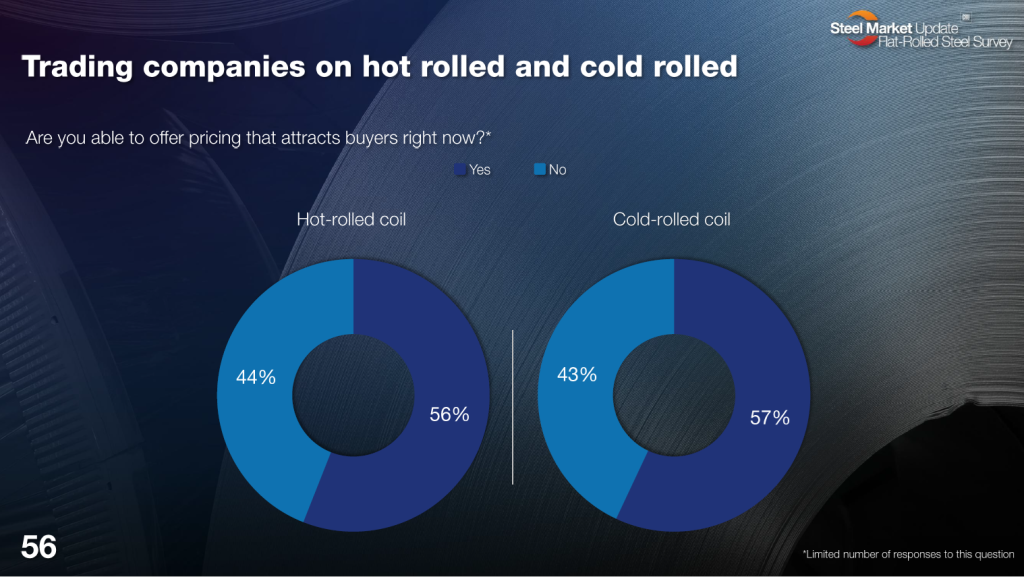

On hot rolled, 56% of traders said they can offer attractive pricing, with one trader reiterating, “Demand for hot rolled is strong.” For cold rolled, 57% of traders surveyed said their prices are competitive, though one trader noted Korean mills remain the most attractive. (Slide 54, below.)

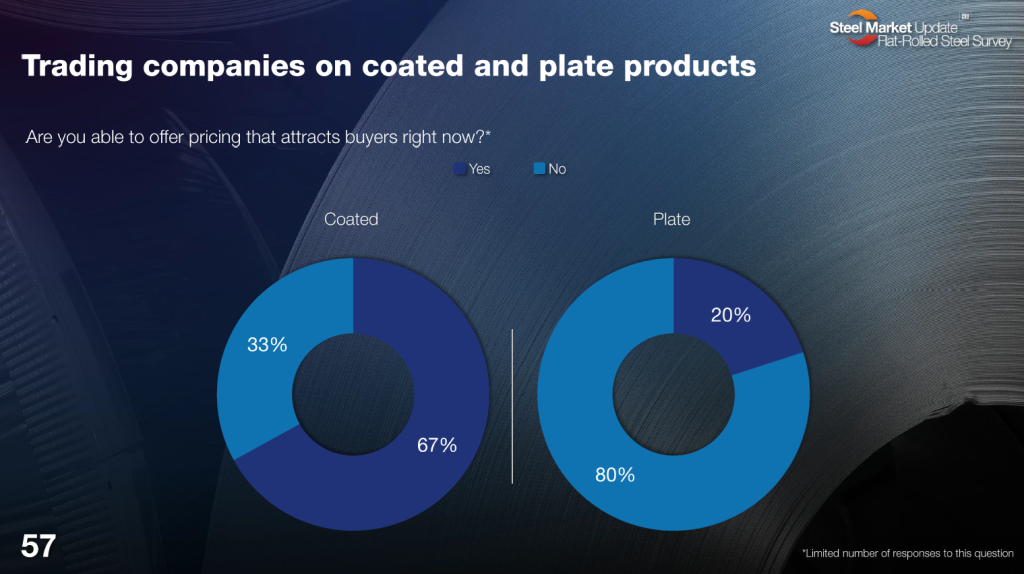

Two-thirds (67%) of traders said coated products are competitive (Slide 57, below). But “not on bare galvanized,” according to one buyer. A trade case last year resulted in hefty fines on corrosion-resistant (CORE) steel imports from ten countries, including Canada and Mexico. That, combined with higher tariffs, caused galvanized imports to reach their lowest level in 15 years in February, according to SMU’s latest import analysis.

On plate, most traders (80%) report current offers are not competitive (Slide 57, below). One buyer warned that landed costs will continue to rise due to logistics constraints, citing driver shortages and elevated freight costs driven by geopolitical uncertainty.

Editor’s note: The full results of the latest SMU Flat-Rolled Steel Survey are available to premium subscribers on the SMU website.