Analysis

April 14, 2026

SMU Price Ranges: Availability trumps price as spot market squeeze tightens

Written by Brett Linton & Michael Cowden

Sheet and plate prices increased yet again this week on an increasingly tight spot market. It’s gotten so tight that some market participants say they’re becoming more concerned about availability than about price.

Case in point: Some industry sources said they’ve been told by domestic mills they won’t be able to get spot tons until at least July.

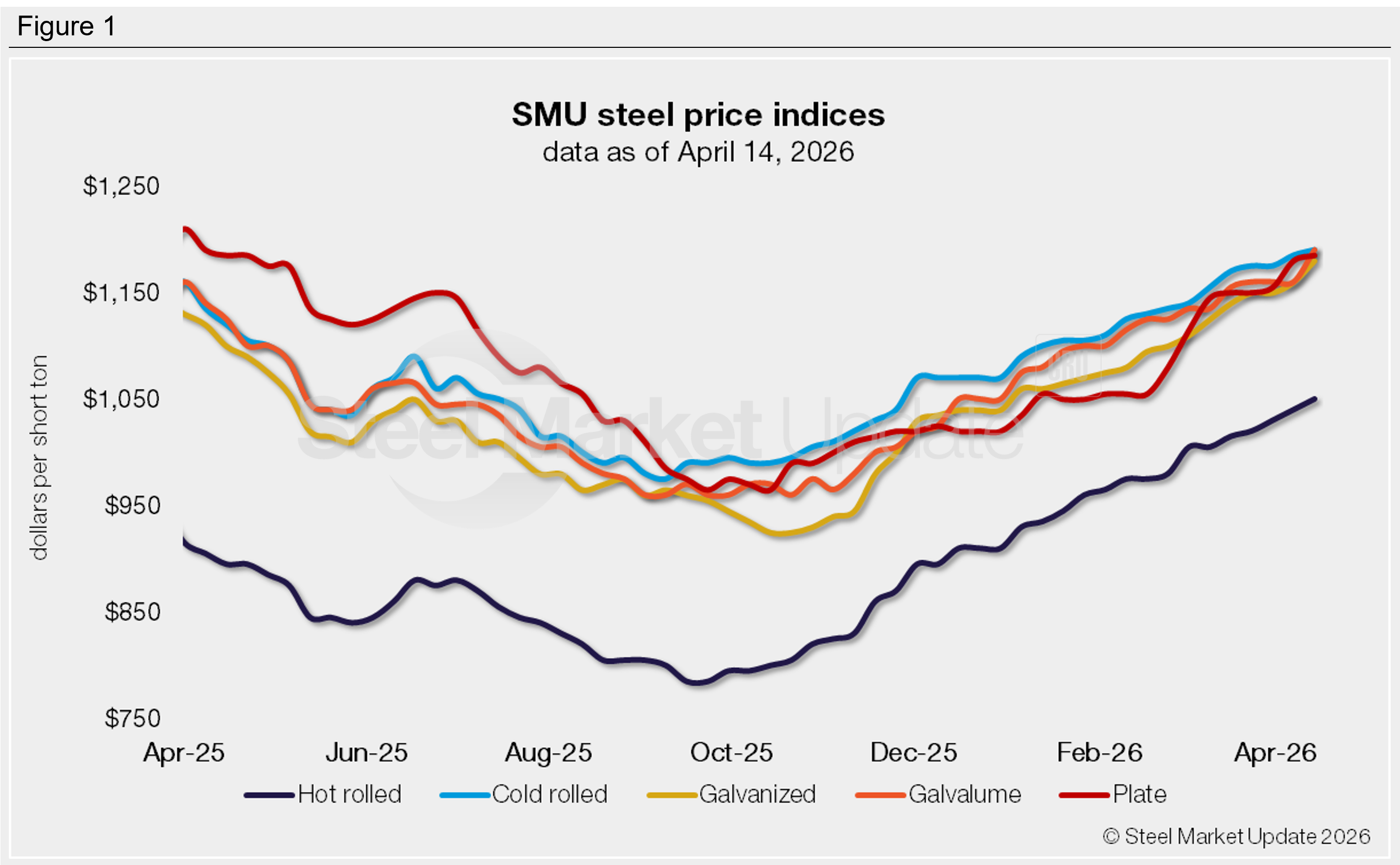

SMU’s spot price assessment for hot-rolled coil now stands at $1,050 per short ton, up $10/st from last week. Gains for coated products were more pronounced. Galvanized jumped $20/st w/w to $1,180/st on average. Galvalume rose $30/st to $1190/st on average.

What they’re saying

The spot tightness that has characterized the HR market appears to be spreading to cold-rolled and coated products as well, some market participants said.

The causes of the spot squeeze are not new. Imports, while up modestly, remain historically low. And it’s not clear whether they can come back in a big way, given higher tariff walls as well as rising freight and insurance costs (and uncertainty) stemming from the Iran War. Domestic mills, meanwhile, continue to grapple with unplanned outages happening against a backdrop of planned ones. And demand has proven more durable than some expected.

What is new – or at least exacerbated – is the lack of spot supplies. Some market participants tell us that they’re unable to get enough steel to serve all their customers. The issue appears to be most pronounced among companies that typically buy largely on a spot basis – and especially if they sell to their customers on a contractual basis.

And in the current environment, large buyers aren’t getting the volume discounts they’ve enjoyed in the past. “If someone sent in a quote for 50 truckloads, we could only do five loads,” one distributor source said of the hot-rolled market. “People are scrambling. And it’s going to get a lot worse before it gets better.”

It’s tight on the coated side as well, another industry source said. “The more desperate calls we’re getting now are on coated. It’s service centers, studders, even some of the automotive guys.”

In short, mills remain in the driver’s seat. “Some of the tubers and service centers have taken advantage of the mills in the past, and now the mills are getting theirs,” a third industry source said.

SMU data

SMU will release service center inventory data to our premium subscribers on Wednesday. And we’ll update lead time figures on Thursday. The supply situation could become critical if inventories continue to decline, lead times remain extended, and demand holds up.

Momentum

Broadly speaking, flat-rolled prices have been grinding higher since early Q4 of last year. We don’t see that trend changing soon. And so SMU’s price momentum indicators remain at higher for both sheet and plate products, signaling we expect prices to increase further in the short term.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil: $1,035–1,065/st, averaging $1,050/st

The lower end of our range is up $15/st w/w, while the top end is up $5/st. Our overall average is up $10/st w/w.

Hot-rolled lead times range from 4–9 weeks, averaging 6.5 weeks as of our April 2 market survey. We will publish updated lead times on Thursday.

Cold-rolled coil: $1,160–1,220/st, averaging $1,190/st

The lower end of our range is up $10/st w/w, while the top end is unchanged. Our overall average is up $5/st w/w.

Cold-rolled lead times range from 6–11 weeks, averaging 8.2 weeks through our latest survey.

Galvanized coil: $1,140–1,220/st, averaging $1,180/st

Our entire range is up $20/st w/w.

Galvanized .060×48” G90 benchmark: SMU price range is $1,230–1,310/st, averaging $1,270/st FOB mill, east of the Rockies.

Galvanized lead times range from 6–10 weeks, averaging 7.9 weeks through our latest survey.

Galvalume coil: $1,160–1,220/st, averaging $1,190/st

The lower end of our range is up $40/st w/w, while the top end is up $20/st. Our overall average is up $30/st w/w.

Galvalume .0142×42” AZ50, grade 80 benchmark: SMU price range is $1,589–1,649/st, averaging $1,619/st FOB mill, east of the Rockies.

Galvalume lead times range from 6–10 weeks, averaging 8.4 weeks through our latest survey.

Plate: $1,160–1,210/st, averaging $1,185/st

The lower end of our range is up $30/st w/w, while the top end is down $20/st. Our overall average is up $5/st w/w.

Plate lead times range from 6–8 weeks, averaging 7.1 weeks through our latest survey.

Brett Linton

Read more from Brett Linton