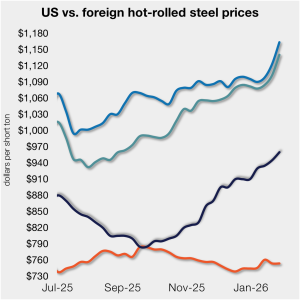

Spread between US HR and imports widens marginally

The price gap between US hot-rolled coil and landed offshore product inched higher, even as prices stateside and abroad mostly moved in tandem vs. last week.

The price gap between US hot-rolled coil and landed offshore product inched higher, even as prices stateside and abroad mostly moved in tandem vs. last week.

SMU polled steel buyers on an array of topics earlier this week, ranging from market prices and demand, to inventories, imports, and evolving market events.

What do SMU's latest survey results show about the current market take on tariffs and where HRC prices are going?

Sheet prices mostly continued their uneven but steady march higher this week, according to SMU’s latest check of the market.

Raw steel output from US mills climbed last week to the highest rate seen in over four months, according to the latest American Iron and Steel Institute (AISI) figures

The latest tally of operational oil and gas rigs increased this week in both the US and Canada, according to the latest figures published by Baker Hughes.

SMU columnist Daniel Doderer looks out over the economy as it regards the steel industry.

SMU’s Steel Buyers’ Sentiment Indices both increased this week to multi-month highs

The total amount of raw steel produced around the world slipped 0.4% from November to an estimated 139.6 million metric tons (mt) in December, according worldsteel data.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

Architecture firms across the US continued to face weak business conditions through the end of 2025, as economic conditions added to the uncertainty, said AIA.

Steel mill lead times held steady on most products this week following the surge seen in early January, according to responses from SMU’s latest market survey

Just over a third of the steel buyers who responded to our market survey this week reported that domestic mills are willing to talk price to secure new spot orders.

The volume of raw steel produced by US mills grew last week, holding on to the gains seen the prior week, according to the latest figures released by the American Iron and Steel Institute (AISI).

SMU’s sheet price indices climbed to new multi-month highs this week, while plate prices marginally declined.

US service centers’ flat-rolled steel supply recovered in December, after trending lower from September to November.

Economic activity across the US increased at a light-to-modest pace, according to the US Federal Reserve’s (The Fed) latest Beige Book report.

The amount of finished steel that entered the US market contracted from September to October, driven primarily by slowing domestic mill shipments, according to SMU’s analysis of Department of Commerce and American Iron and Steel Institute (AISI) data

The number of oil and gas rigs operating in the US fell this week, while Canadian activity recovered further, according to the latest data released from Baker Hughes.

SMU's steel market chatter this week.

The opening weeks of 2026 are revealing a subtle but important change in the HRC futures market, as tightening physical conditions begin to exert greater influence over pricing dynamics.

The volume of steel shipped outside of the country increased 11% from September to October 2025 to a seven-month high of 662,000 short tons (st), according to recently released data from the US Department of Commerce.

Participants in the domestic steel plate market said they are maintaining strong order books, experiencing longer lead times, and finding mills are less open to negotiating prices.

The majority of SMU’s sheet and plate price indices rose this week, with multiple products climbing to new multi-month highs

According to recently released final US Commerce Department data, US steel imports rebounded 11% month on month (m/m) in October 2025 after falling to a multi-year low one month earlier. The latest license figures suggest imports eased back by 3% in November and by another 2% in December, with trade again nearing historical lows.

US mills have begun ramping up output after the end-of-year holiday slowdown, according to the latest data from the American Iron and Steel Institute (AISI).

SMU’s January ferrous scrap market survey results are now available on our website to all premium members.

Shipments of heating and cooling equipment fell for the sixth straight month in November, reaching the lowest rate seen since October 2016, according to the latest data released by the Air-Conditioning, Heating, and Refrigeration Institute (AHRI).

The Current SMU Steel Buyers’ Sentiment Index has rebounded from our previous market check in December. However, Future Buyers’ Sentiment has edged down, according to our latest survey data.

The number of oil and gas rigs operating in the US fell this week, while Canadian activity surged, according to the latest data released from Baker Hughes.