SMU price ranges: Sheet prices rebound, plate flat

Sheet prices reversed course and moved higher this week, while plate priced remained flat, according to our latest canvas of the market.

Sheet prices reversed course and moved higher this week, while plate priced remained flat, according to our latest canvas of the market.

Prices for pig iron in Brazil have increased despite efforts by US-based buyers to lower them.

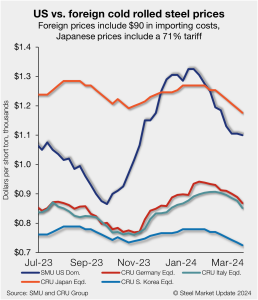

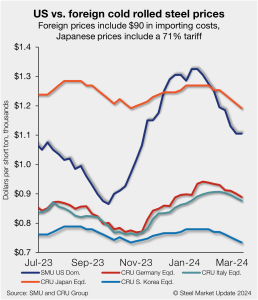

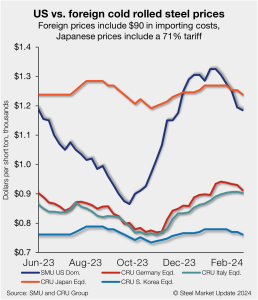

Foreign cold-rolled (CR) coil remains notably less expensive than domestic product even with repeated tag declines across all regions, according to SMU’s latest check of the market.

As the month of March goes into the second half, the scrap community is trying to cope with the large drop in ferrous scrap earlier this month.

2024 started with a $200 per short ton (st), one-week demon drop in the CME Midwest hot-rolled (HR) coil futures. Then, HR futures consolidated in the low $800s/st with the April future trading to as low as $770/st as the curve shifted into contango or upward sloping. A big move was expected, and a big […]

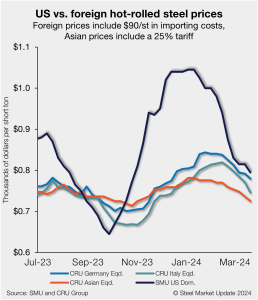

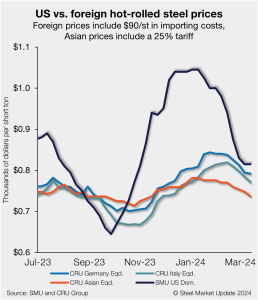

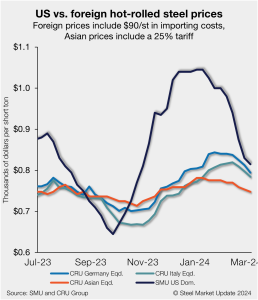

US hot-rolled coil (HRC) remains more expensive than offshore hot band but continues to move closer to parity as prices decline further. The premium domestic product had over imports for roughly five months now remains near parity as tags abroad and stateside inch down.

Sheet and plate prices mostly moved lower this week after little change was noted the week prior. Despite edging down, sentiment is mixed, and many suggest a bottom may be near.

Foreign cold-rolled coil (CR) remains significantly less expensive than domestic product even as US tags continue to decline in a hurry, according to SMU’s latest check of the market.

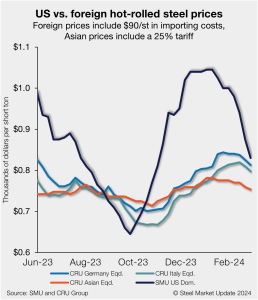

US hot-rolled coil (HRC) remains more expensive than offshore hot band, even as domestic prices remain under pressure. The premium domestic product had over imports for roughly five months now remains near parity as tags abroad and stateside inch down.

The spread between hot-rolled coil (HRC) and prime scrap prices has narrowed for the third consecutive month in March, according to SMU’s most recent pricing data.

The ferrous scrap market experienced a sharp decline for March shipments. Prime scrap fell $60-70 per gross ton (gt) while shredded and other obsolete grades declined $40-50/gt. It seems these prices were accepted in the trade by dealers across the continent.

Sheet and plate prices were mostly flat this week – largely in response to the mill price blitz from last week – pausing the downtrend they’d been on for the better part of 2024.

US ferrous scrap prices fell steeply in March for HMS, shredded, and prime scrap, sources told SMU.

As I see it, the market looked to be a perfect storm for consumers this month while two large steel mills tried to put a floor on hot-rolled coil (HRC). One source speculated that “flat rolled mills coordinated their downtime and will take out 250,000 tons of capacity in April,” which made them attempt to put a bottom on flat-rolled product.

A weak start for sheet demand this year has continued to weigh on global prices. European demand outside of the renewable energy sector was weak enough that market participants said mills are likely to cut output further after several furnace restarts earlier in the year. In China, demand has also failed to pick up after recent holidays, and even government announcements of more stimulus measures during the country’s “Two Sessions” meetings failed to boost market confidence.

ArcelorMittal is targeting a minimum base price for hot-rolled (HR) coil of $825 per ton. The Luxembourg-based steelmaker said the new floor price was effective immediately in a letter to its commercial team dated Friday, March 8.

Hot rolled (HR) futures have been on a bit of a hot streak recently, while busheling futures have been more in the “not” category.

Nucor and Cleveland-Cliffs on Thursday announced target minimum base prices for hot-rolled (HR) coil. Both said the moves were effective immediately.

US hot-rolled coil (HRC) is now just about 5% more expensive than offshore hot band. The premium domestic product had over imports for roughly five months is all but gone, and nearing parity.

A Detroit area steelmaker this morning announced its offers for scrap for March scrap shipments. The drop in its offer prices were larger than most industry observes forecasted, especially for shredded scrap. Many in the scrap community had predicted that prime scrap would drop $40-50 per gross ton (gt) with shredded only down $30-40/gt. But other market participants were skeptical about these predictions given bearishness in ferrous markets, both domestically and abroad.

Sheet and plate prices this week continued the downward trend they’ve been on for most of 2024. Some market sources predicted that a wave of spring maintenance outages would help to stabilize lead times and prices in the weeks ahead – especially should service center inventories, high at the beginning of the year, come down meaningfully.

The strong resilience of iron ore prices has come to an end with the weak steel performance worldwide and significantly improved iron ore availability in China.

The news in the West was that a mill in the Rocky Mountain region made a significant reduction in their usual purchase program, while still another small mill in the region also apparently reduced their buying program for February.

The March scrap trade is set to pick up steam next week.

The premium US hot-rolled coil (HRC) held over offshore product for roughly five months has nearly vanished. Domestic hot band prices continue to run downhill at a high rate, erasing a $300/st gap they had over imported HRC just two months ago.

The March outlook for most ferrous products is trending down faster than most participants thought as recently as a week ago.

US hot-rolled (HR) coil prices have fallen further this week, working their way to $800 per short ton (st) on average – a mark not seen since late October.

Foreign cold-rolled coil (CR) remains much less expensive than domestic product even as prices in the US have declined at a rapid pace over the past month, according to SMU’s latest check of the market.

Falling US sheet prices have reduced the attractiveness of hot-rolled (HR) coil imports as domestic mills price competitively to secure limited business. However, tightness in the CR coil market has extended delivery to June or July in some cases, and buyers may consider to import given competitive prices and arrival times.

In the period between mid-February and mid-March, CRU forecasts global demand for steelmaking raw materials to change little from the previous month,but buying activity will improve towards the end of next month