HRC vs. busheling spread narrows in January

The spread between hot-rolled coil (HRC) and prime scrap prices narrowed slightly this month, according to SMU’s most recent pricing data.

The spread between hot-rolled coil (HRC) and prime scrap prices narrowed slightly this month, according to SMU’s most recent pricing data.

US hot-rolled (HR) coil prices fell noticeably this week for the first time since late September. SMU’s hot-rolled coil price now stands at $1,025 per ton on average, down $25 per ton from last week. Cold-rolled (CR) coil was unchanged at $1,325 per ton.

Domestic scrap prices ended up down slightly after a roller coaster of trading in January, scrap sources told SMU.

Turkish scrap import prices increased last week with CRU’s assessment for HMS1/2 80:20 at $423 per metric ton (t) CFR, up by $7/t week over week (w/w) but down $2/t month over month (m/m). This was driven by a pickup in buying activity.

For two consecutive months, the initial scrap prices didn’t attract the amount of scrap that mills needed. A Detroit area mill came in at $460 per gross ton (gt) for busheling, which was down $50 from last month and down $20 on shredded and plate and structurals (P&S). But I guess they did not know at the time another mill in the district bought scrap sideways. Needless to say, that order filled right away. SMU could not find any supplier who sold at down $50.

The spread between cold-rolled coil (CRC) and hot-rolled coil (HRC) prices jumped during the week of Jan. 8 as cold rolled tags continued to rise while hot rolled tags held steady.

After a holiday period that saw HR futures volumes somewhat muted in December, the first week of January brought with it increased interest reflected in higher volumes.

US scrap prices for January remained unsettled as of early Thursday afternoon, according to market sources.

Pig iron prices rose month over month (MoM) in all major regions aside from Europe on improved buying. Demand in the US remains robust while market participants report that availability of Brazilian material increased after tightening a month prior. Meanwhile, Ukrainian export capacity increased due to greater access to temporary sea corridors.

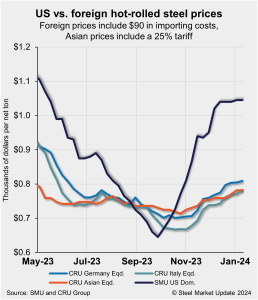

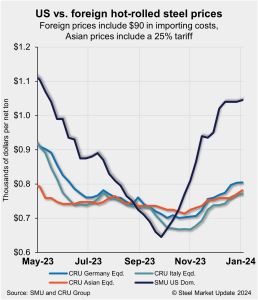

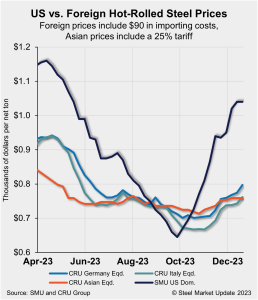

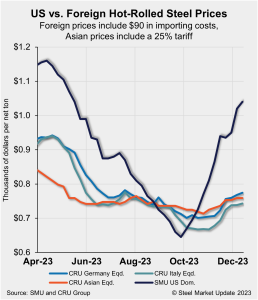

US hot-rolled coil (HRC) prices were unchanged this week but remain significantly more expensive than offshore product. While imported hot band tags increased vs. last week, gains were marginal, keeping domestic HRC substantially more expensive than imports. All told, US HRC prices are 24.3% more expensive than imports, a premium that is down only slightly […]

Hot-rolled (HR) coil prices remain in the holding pattern they've been in since mid-December, according to SMU pricing archives.

A Detroit-area mill entered the scrap market on Friday afternoon with the following offers: The Chicago area followed suit: Mills in the Great Lakes region sensed there was ample supply of most grades. Also, they all bought heavily last month and so had sufficient inventories to make this move, market participants said. Still, the move surprised […]

After a brief decline in the price of scrap for the Turkish market, which peaked in December at approximately $424 per metric ton (mt) for HMS 80/20, the market has bottomed at $405/mt on cargoes from Europe.

Trading slowed across the Midwest hot-rolled coil (HRC) futures curve in the final weeks of 2023, with prices drifting mostly sideways through the month of December.

Radius Recycling reported a net loss in its fiscal first quarter of 2024 on tighter supply flows for recycled metals and lower average selling prices for the company’s products.

US hot-rolled coil (HRC) prices moved up again this week and remain significantly more expensive than offshore product.

Cleveland-Cliffs is now targeting base prices of $1,150 per ton for hot-rolled coil (HRC), according to a press release on Wednesday morning, Jan. 3.

Sheet prices were mixed in SMU’s first assessment of the market in the New Year.

Nucor Corp. announced in a letter to customers on Friday, Dec. 29, that its plate mill group would hold prices unchanged for as-rolled discrete plate, normalized, and quenched-and-tempered plate with the opening of its plate mill order book for February.

We started 2023 with HRC spot pricing around $700 per ton and the third-month future (March ‘23) trading at $800/ton. That same future eventually settled at $1,059/ton - a $259/ton swing. Today, spot pricing is just shy of $1,100/ton for HRC, and the third-month future (March ‘24) settled at $1,091/ton. The clear takeaway: a lot can change over three months. And while future contracts are a valuable tool for hedging, they are a terrible predictor of price.

US hot-rolled coil (HRC) prices might have plateaued. But while prices for offshore product have increased in some regions, imports remain significantly cheaper that domestic material. All told, US prices are roughly 26% more expensive than imports, a premium that is down only slightly from last week.

As we look back at the scrap market for 2023, it basically followed its normal seasonal pattern. Most of the disruptive geopolitical events that riled ferrous raw materials occurred in 2022. So, with those things out of the way—or settling down at least for now—2023 resumed its normal pattern.

US hot-rolled coil (HRC) prices were unchanged week over week (WoW) following a string of mostly upward moves dating back to late September.

Pig iron prices rose month over month (MoM) for all major regions, driven by rising scrap prices.

Over the last two decades, the role of the scrap broker has been diminished in favor of steel mills purchasing their scrap requirements directly from scrap dealers.

US hot-rolled coil (HRC) prices continued their upward movement this week, distinctly outpacing increases for offshore product once again. Domestic tags are now 27% more expensive than imports - the widest pricing gap in nearly two years.

Last week in Chicago, we hosted several metals companies for our bi-annual Metals Price Management Seminar (“MPMS”).

The spread between hot-rolled coil (HRC) and prime scrap prices widened slightly this month, according to SMU’s most recent pricing data.

Sheet prices increased again this week on the heels of higher costs for scrap, pig iron, and iron ore.

US scrap prices shot up in December and are expected to continue their rise in January, market sources told SMU.