Prices

December 21, 2023

HRC futures: 2023 was wild, what comes next?

Written by Daniel Doderer

We started 2023 with HRC spot pricing around $700 per ton and the third-month future (March ‘23) trading at $800/ton. That same future eventually settled at $1,059/ton – a $259/ton swing.

Today, spot pricing is just shy of $1,100/ton for HRC, and the third-month future (March ‘24) settled at $1,091/ton. The clear takeaway: a lot can change over three months. And while future contracts are a valuable tool for hedging, they are a terrible predictor of price.

Turning our focus to today’s curve, the chart below shows Thursday’s settlements of the CME Hot-Rolled Coil futures curve in solid blue, with the darker blue shaded region representing the last month’s trading range and the lighter shaded region representing the month prior. Clearly, the holiday’s started early for the curve, with the sharp rally in November losing steam since Thanksgiving.

CME hot-rolled coil $/ton futures curve (Dec.23-Dec.24)

Looking more closely at the data, a notable shift is the recent sharpening of backwardation. This is shown by near-term futures trading at the higher end of their recent range, while longer-term futures are trading at the bottom.

The market signal is that material today is at a premium compared to expectations for the future. There are a few reasons the market is pricing in backwardation. First, mills are currently operating with incredible profitability. Going forward, expectations are for that stretched level to mean-revert.

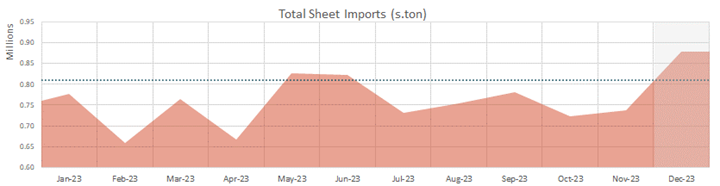

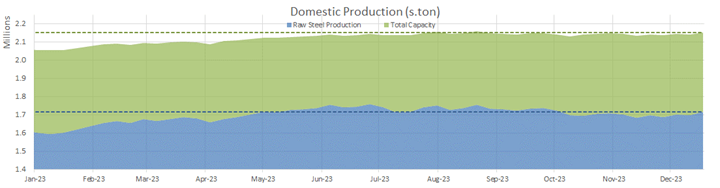

The second driving factor is the expectation for the clear trend of increased supply to be even more pronounced going into next year. In the middle of November, domestic production bottomed out, as did imports in October. Now both have started to push higher. The two charts below show total sheet imports and AISI raw steel production.

Notes on imports: Our preliminary forecast for December’s imports (shaded) shows that arrivals are clearly on the rise, just shy of 900,000 tons. For context, this would (1) be the highest level of arrivals for the year and (2) be the first time we meaningfully pushed above the dotted line (which our analysis suggests is the neutral level).

Notes on domestic production: While current levels of raw steel production are not at their highest level of the year, this week could be a turning point. AISI’s capacity utilization was up 0.8% to 74.6%, its highest level since the first week of October – finally representative of what we are seeing in related data (i.e., softening but elevated lead times, pockets of availability, and incredibly attractive margins).

So, we know that supply will be increasing going into the first quarter of next year. But what about demand? 2023 will be viewed as mixed with clear bright spots and other disappointments from steel consuming sectors. However, it has also clearly been much better than expected.

The chart above is the Bloomberg “Economic Surprise Index,” which shows how economic data is coming in versus consensus expectations and which provides a clear signal on demand. Through our analysis we’ve found a strong leading relationship between steel prices and these economic surprises.

Since peaking in late September, the index lost steam and was sitting right around “neutral” up until December. This upward momentum culminated in this week’s housing and sentiment data solidly beating expectations. Also, the final 3Q23 GDP figures show the strongest growth since 4Q21.

As is always the case, economic data is inherently lagged and can change on a dime. But through our analysis, changes in demand explain 66% of steel price movements, while changes in supply only explain 9% of price movements. Additional data will be necessary before anyone is convinced that the prior trend lower is reversing. But this is an encouraging preliminary signal.

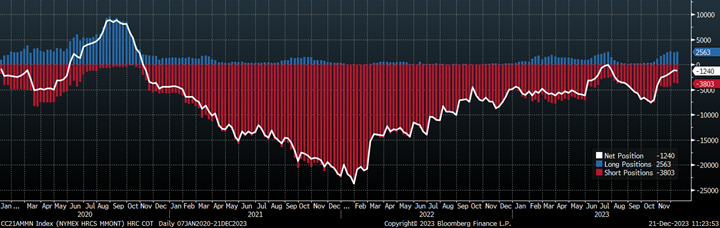

Moving over to the plumbing, the net speculative position for money managers is below.

The net speculative position is represented in white. It is the offset of money managers who are long (blue) and short (red). Long positions have been on the rise since the end of October and are still holding above the levels seen in July. Short positions continue to make up most of the market.

The takeaway from this recent development is that speculation on whether the HRC price will continue to rally or will begin to fall is essentially split. In the end, as is always the case, steel pricing in the first quarter will be dictated by whether demand continues to outperform expectations in the face of the meaningful increase in upcoming supply.

About Flack Global Metals

In 2010, Flack Global Metals (FGM) was founded with the mission to reinvent how metal is bought and sold. Over 13 years later, the company has evolved into a hybrid organization combining an innovative domestic flat-rolled metals distributor and supply chain manager, a hedging and risk management group supported by the most sophisticated ferrous trading desk in the industry known as Flack Metal Bank (FMB), and an investment platform focused on steel-consuming OEMs called Flack Manufacturing Investments (FMI). Together, these entities deliver certainty and provide optionality to control commodity price risk in the volatile steel industry.

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Flack Global Metals or Flack Metal Bank should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.