Prices

December 14, 2023

HRC Futures: The role a hedge plays

Written by Logan Davis

Last week in Chicago, we hosted several metals companies for our bi-annual Metals Price Management Seminar (“MPMS”). During the class, we heard feedback we believe is important to address here, as our readers continue to install and implement their respective hedge programs.

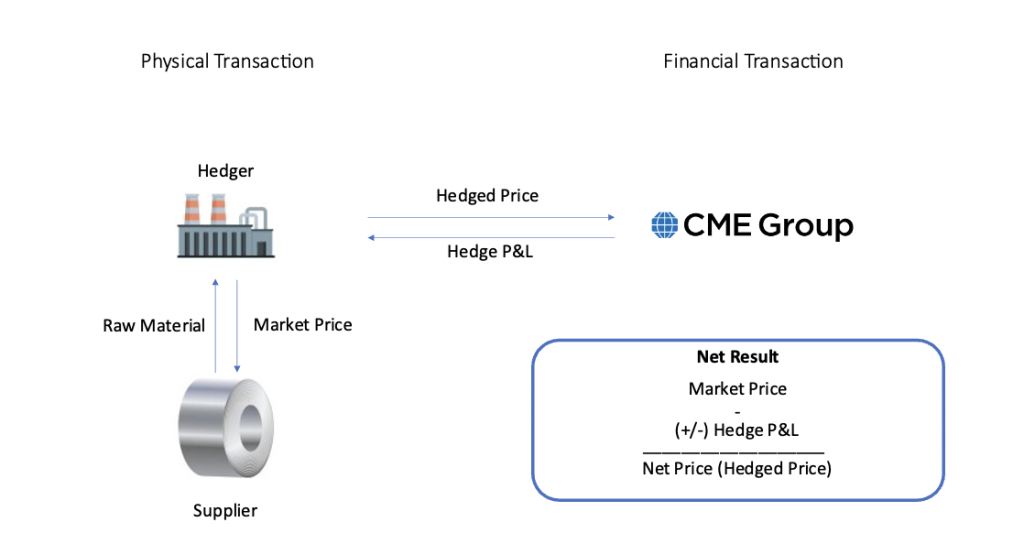

During our two-day education session, there was some discussion around the role a hedge plays in the related physical transaction. It’s important to remember that a hedge is a separate, but related, financial transaction. This transaction represents an expected physical transaction that will occur at some future date. An important note: a company’s hedge position does NOT have to alter the regular operations between its suppliers or its customers.

As an example, see the diagram below:

This physical + hedge structure can be extrapolated out in time for all committed future transactions. As an example, let’s say we are a hedger that has committed to buying 500 tons/mo. for 2024, all to be priced using CRU Index Week 1 monthly prices (Market Price).

Based on these terms, we know we will have material that we need to purchase in each month throughout 2024. Knowing our future raw material quantity, we can have confidence in the quantity of the finished product we’ll be able to sell. However, we don’t have enough information to have confidence in a sales price for those finished goods.

By using the HRC futures price in each corresponding month, our company should have confidence to make sales at the right price. Once a sale has been made, prudent risk management would have us place a hedge to protect against a rise in the raw material from now until the time the supplier will issue the invoice for that respective month.

Alternatively, our company could buy futures to take advantage of lower prices before the supplier is ready to set the price. As a result, the company would have an average inventory cost for each time period, that they could then use in their sales process.

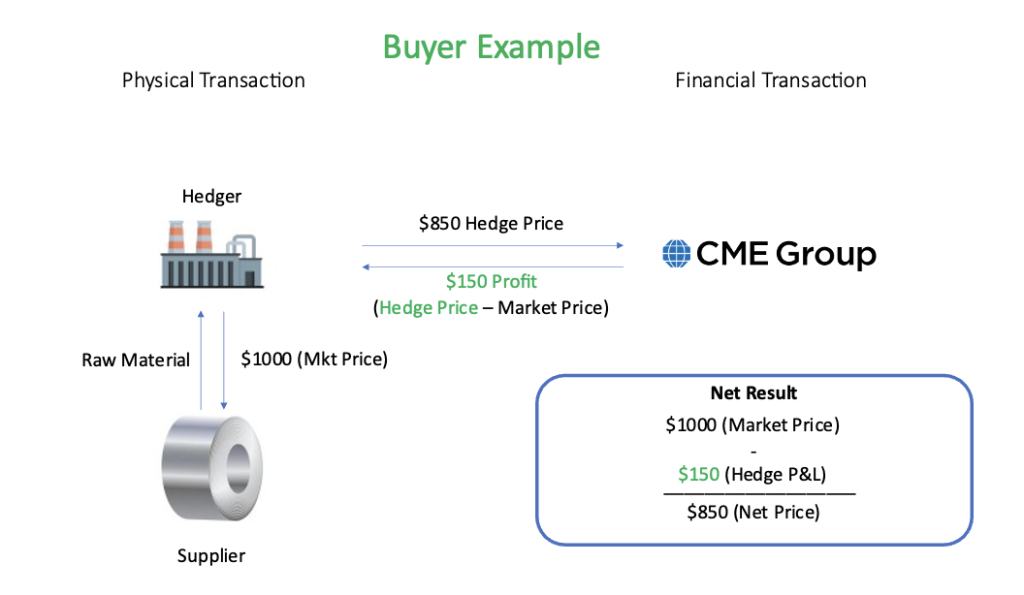

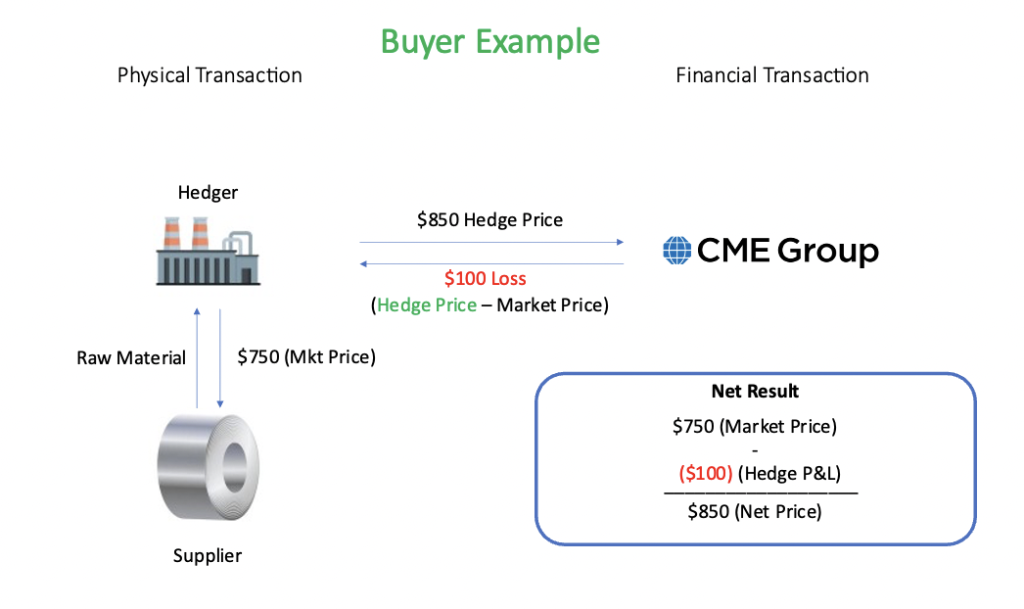

We will use the diagram from above to illustrate how a futures gain and a futures loss is ultimately the same thing.

The above illustration shows the entry point of the hedge, and its ending point. In reality, the hedge’s price and value will fluctuate throughout time, from entry to end.

Once a hedge is established, astute hedgers will re-evaluate and manage the hedge position as the market and the hedge value fluctuates. While there are many things to contemplate with futures and options, one of the advantages is their flexibility. Unlike an agreement on physical delivery with a supplier or customer, futures and options can be entered and exited at any time before expiration.

By utilizing the full suite of risk management tools available to you, hedgers can capitalize on market volatility through adjusting their hedge positions as the market rises and falls. When making these decisions, it’s important to consider the trade-offs between strategies, and how your risk management goals are being addressed.

If you’d like to learn more about things to consider when using these tools, please visit the following link, CPE Accredited Metals Hedging Class.

There is a risk of loss in futures trading. Past performance is not indicative of future results. © 2023 Commodity & Ingredient Hedging, LLC. All rights reserved.