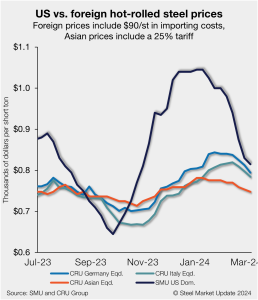

CRU: Low demand continues to weigh on global sheet prices

A weak start for sheet demand this year has continued to weigh on global prices. European demand outside of the renewable energy sector was weak enough that market participants said mills are likely to cut output further after several furnace restarts earlier in the year. In China, demand has also failed to pick up after recent holidays, and even government announcements of more stimulus measures during the country’s “Two Sessions” meetings failed to boost market confidence.