Prices

April 3, 2014

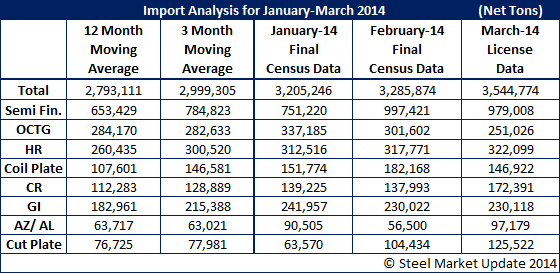

February Final Imports Highest since 2007

Written by Brett Linton

The US Department of Commerce released Final Census numbers for the month of February 2014. The 3,285,874 net tons was the highest level for imports since July 2007 when they were 3,288,054 NT.

In the table below we have provided updated twelve month and three month moving averages through the month of February. The March data continues to be a projection based on license data collected through the 1st of April. As you can see by the data shown we had a large jump in semi-finished steels (most of which are slabs) and most of the other products. February “other metallic” (most of which is Galvalume) were down but it looks like February will be sandwiched between two months over 90,000 tons each.

Below is an interactive graphic on flat rolled imports, showing data for both total imports and select products. You will see just white space unless you view the article once you are logged into our website. If you need assistance please contact our office and we will work with you with your passwords or on how to navigate the website. You can reach us at: info@SteelMarketUpdate.com or by phone: 800-432-3475.

{amchart id=”105″ Steel Imports- All Products, Final Data by Month}