Prices

February 23, 2017

Hot Rolled Futures: Buckle Your Chinstrap

Written by David Feldstein

The following article on the hot rolled coil (HRC) futures markets was written by David Feldstein. As the Flack Global Metals director of risk management, Dave is an active participant in the hot rolled coil (HRC) futures market and we believe he will provide insightful commentary and trading ideas to our readers. Besides writing Futures articles for Steel Market Update, Dave produces articles that our readers may find interesting under the heading “The Feldstein” on the Flack Global Markets website www.FlackGlobalMetals.com.

While there is always a lot of noise to be deciphered in the steel market, it is clear that the primary catalyst behind Nucor’s flat rolled price increase this week was the futures article written in last Thursday’s Steel Market Update and this month’s Week-Over-Week reports published at www.flackglobalmetals.com.

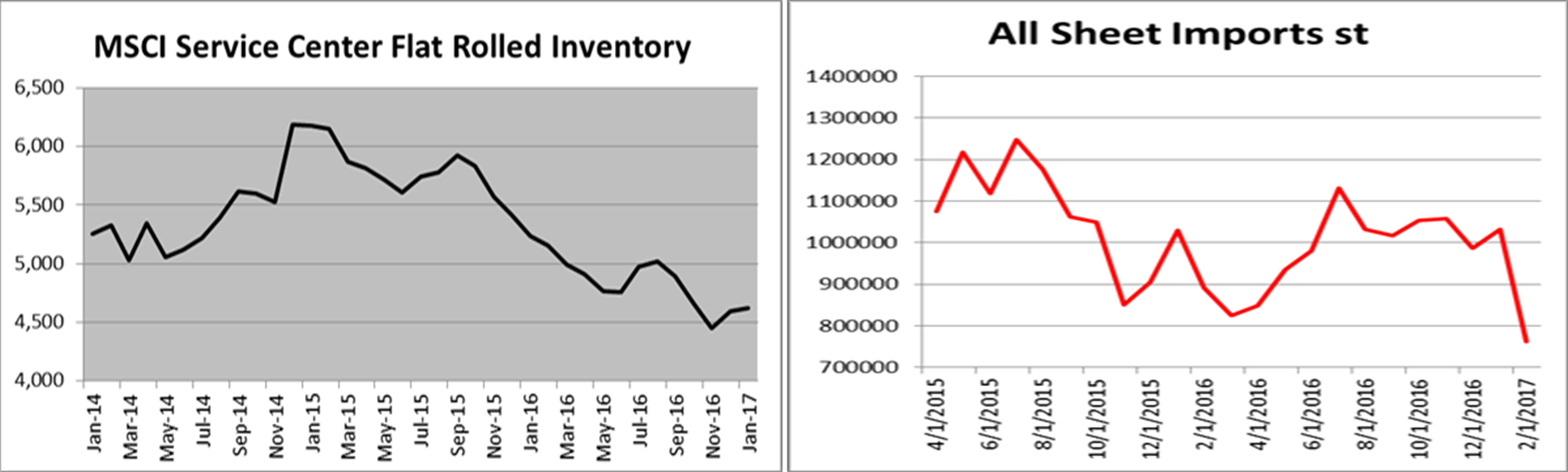

All kidding aside, it is very difficult to create a bearish story considering current steel market fundamentals. While these issues are discussed at length in the week-over-week report on FGM’s website, I’ll summarize it with a strengthening ISM PMI (expect next Wednesday’s to crush expectations), strong jobs and auto sales, improving construction spending, a resurgence in energy, building inflationary pressures, crashing imports, improving global fundamentals…hold on I gotta take a breath…strong raw material prices, China pumping up its old economy and low, low inventory across the manufacturing industry.

BUY THE DIPS!!

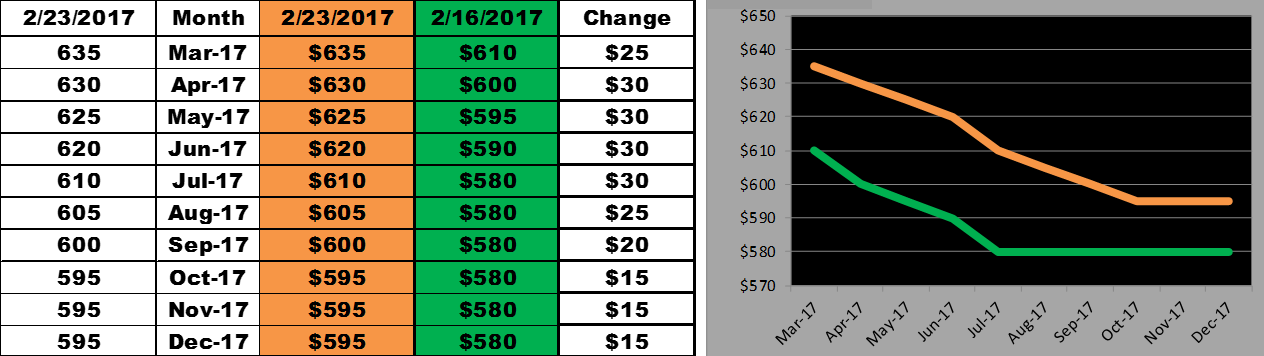

CME Midwest HRC futures rallied this week with Q2 trading up to $625/st today. The 2017 curve has shifted much higher in the past week. Today’s curve was estimated from prices provided this afternoon by Crunchrisk.

CME Midwest HRC Futures

The scrap rebound has not only held but is reaching new highs. March domestic scrap settlements are still two weeks away, but expect news and rumors about scrap negotiations to lead flat rolled prices. I have heard some calls that busheling could be up as much as $80 this month. Regardless, March LME Turkish scrap futures closed at $297/mt and Busheling settled last night at $320/lt. Will there be another price increase after March scrap settles?

March LME Turkish Scrap & March CME Midwest Busheling Futures

Prices in scrap futures over the past thirty days have been nothing short of amazing, especially when Chicagoans are walking around in t-shirts in February. If it seems like the old rules aren’t working, recognize something else could be happening! Don’t be the frog in the pot.

The nonstop march higher in iron ore futures took a breather this week. Prices remain near multi-year highs, while the curve is still steeply backwardated. March SGX iron ore futures settled at $86/t.

March SGX Iron Ore Futures and SGX Iron Ore Curve

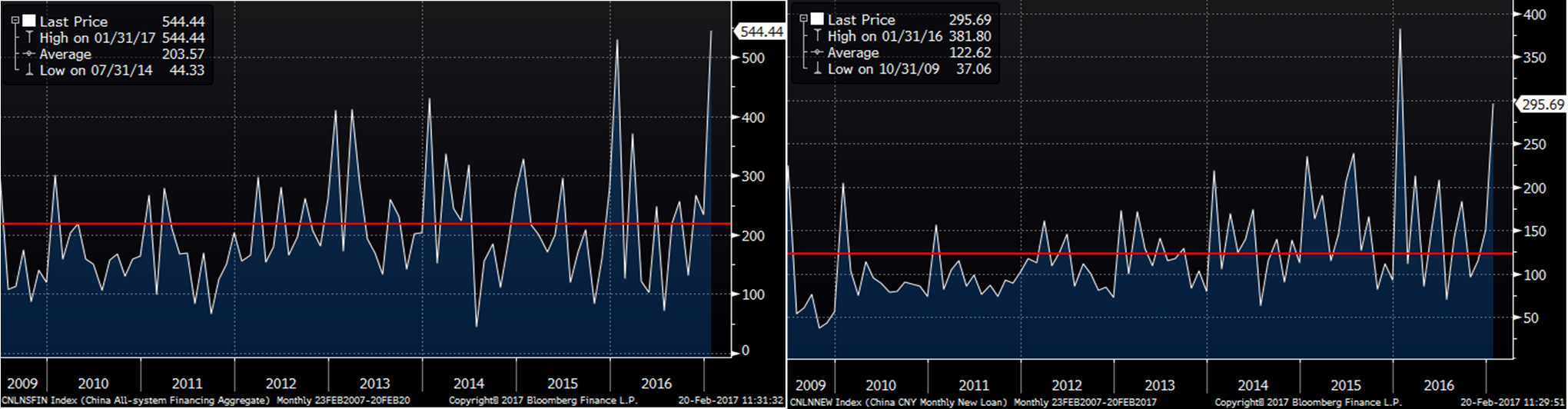

China aggregate financing tracks the outstanding amount of credit extended to businesses and consumers. January data showed an explosion to $544 billion of aggregate financing and almost $300 billion of new loans. If you are having a hard time understanding the iron ore price/rally or Chinese steel prices, this is the first place to look for answers.

January China Aggregate Financing and New Monthly Loans (USD)

The chart below shows the spike in Chinese aggregate financing in January, 2016 (green) sparking a strong run up in iron ore prices (red). US Midwest HRC prices (white) had a delayed rally that eventually sent prices up 50%, from $400/st to $600/st, in six weeks.

2016 Chinese Aggregate Financing, Chinese Iron Ore and TSI Midwest HRC

History may be repeating itself. Even higher Chinese aggregate financing in 2017 and a spike in iron or prices have already occurred. How will these developments affect the US flat rolled market in 2017 considering domestic fundamentals are much stronger. Oh, and there are these two charts.