Prices

April 20, 2017

Futures Up, Don't Fight the Fed

Written by David Feldstein

The following article on the hot rolled coil (HRC) futures markets was written by David Feldstein. As the Flack Global Metals director of risk management, Dave is an active participant in the hot rolled coil (HRC) futures market and we believe he will provide insightful commentary and trading ideas to our readers. Besides writing futures articles for Steel Market Update, Dave produces articles that our readers may find interesting under the heading “The Feldstein” on the Flack Global Metals website www.FlackGlobalMetals.com.

Buy the dips……

That’s been the theme of this article for 2017. The fundamentals remain stellar.

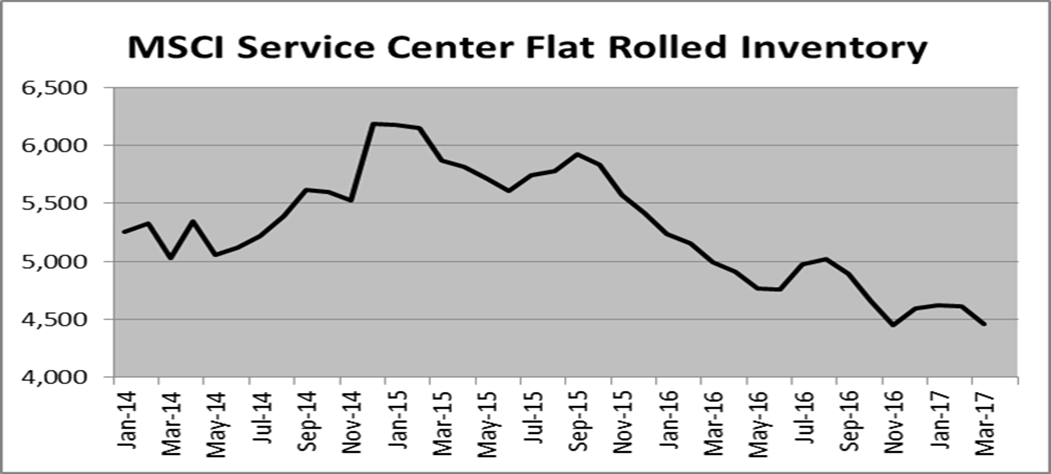

This week, the MSCI released March service center data showing an increase in flat rolled shipments and a decrease in inventory. Very bullish.

There has been some confusion/controversy about the reliability of the MSCI data after they were rumored to lose some service center data providers. If you look at the chart above, you would expect to have seen a sharp one time drop when the providers pulled out rather than a slow downtrend if that was the case. I would assume the MSCI somehow normalizes the data, but this is mere speculation on my part.

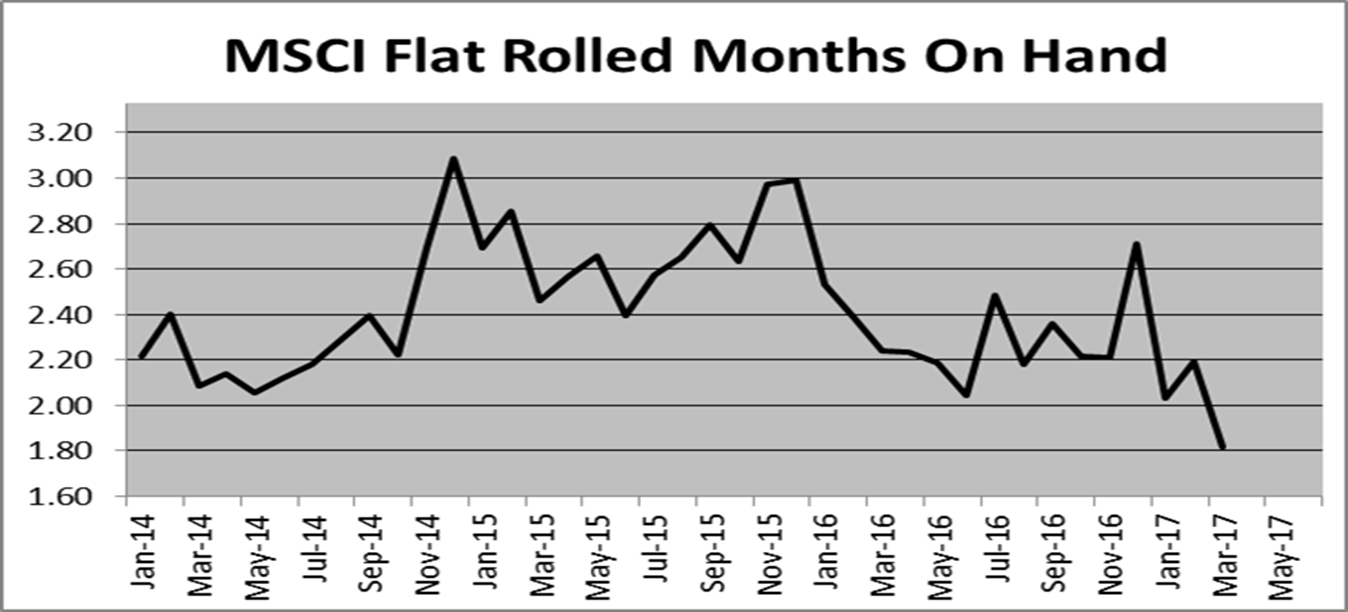

Consider the MSCI data provides a cross section of the aggregate service center data and we assume this data is representative of all service centers. So, regardless of whether the data covers 40, 60 or 80 percent of service centers, looking at the months-on-hand (M.O.H.) data will give us a standardized number through time that is unrelated to the changes in the number of service center contributors. March M.O.H. is at 1.82, the lowest level since August, 2009!!!

As has been discussed for months in this article and on www.FlackGlobalMetals.com in the Week Over Week report, data showing low inventory levels has not only been provided by the MSCI report, but also in the ISM Manufacturing PMI and the Durable Goods Report. Domestic steel mills know service center inventory levels are low too.

In fact, earlier today during Steel Dynamic’s earnings conference call, CEO Mark Millet said, “1.8 months-on-hand is unheard of…I would imagine if service centers are going to support OEM customers when demand continues to grow, they will need to restock and this will fuel additional demand.” It’s kind of hard to bluff when the other side knows you have a weak hand.

So this is the crux of the “buy the dips” theme based on the assumption that the buyers will be quick to scoop up tons if discounted below current prices.

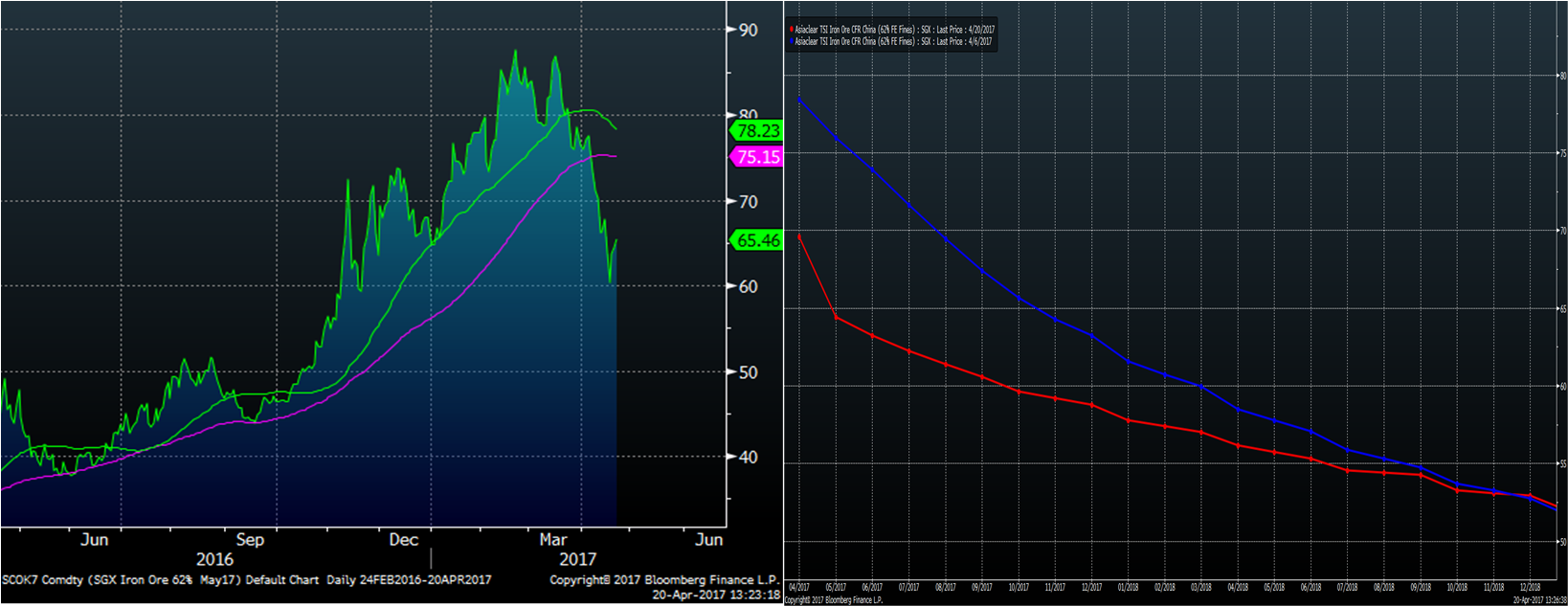

Meanwhile in Asia, holy iron ore Batman! Iron ore prices have fallen 20% since the last time I wrote a SMU article two weeks ago! Prices have fallen along with prices for finished steel products and this is a real cause for concern if the Chinese steel export monster is waking back up.

May SGX Iron Ore Futures & Curve

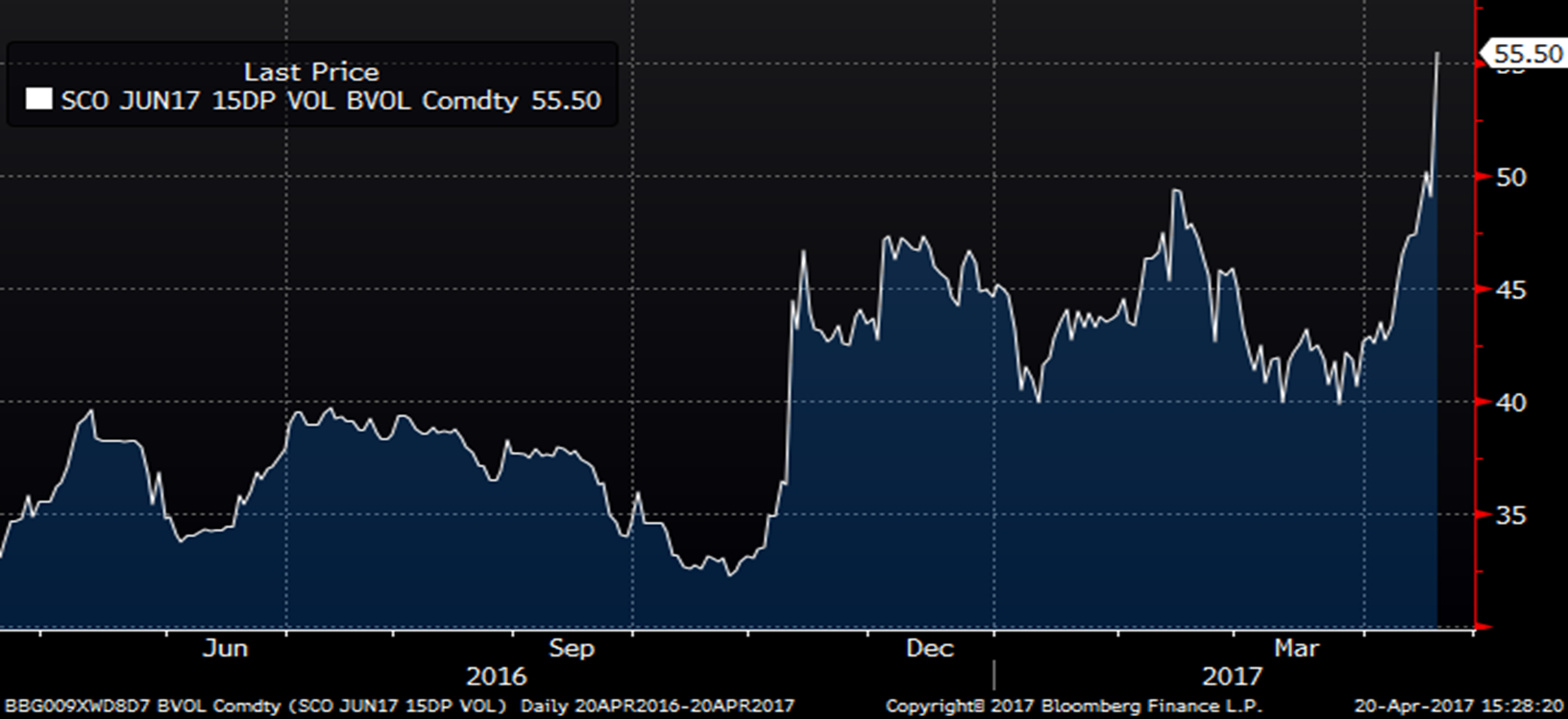

The price of insuring downside risk in iron or spiked as prices have plummeted. Expect this increased volatility to whip day-to-day ore prices around sharply. Don’t be surprised if prices fall to $50 or rally back to $80 by the end of the month.

June and July Iron Ore Volatility

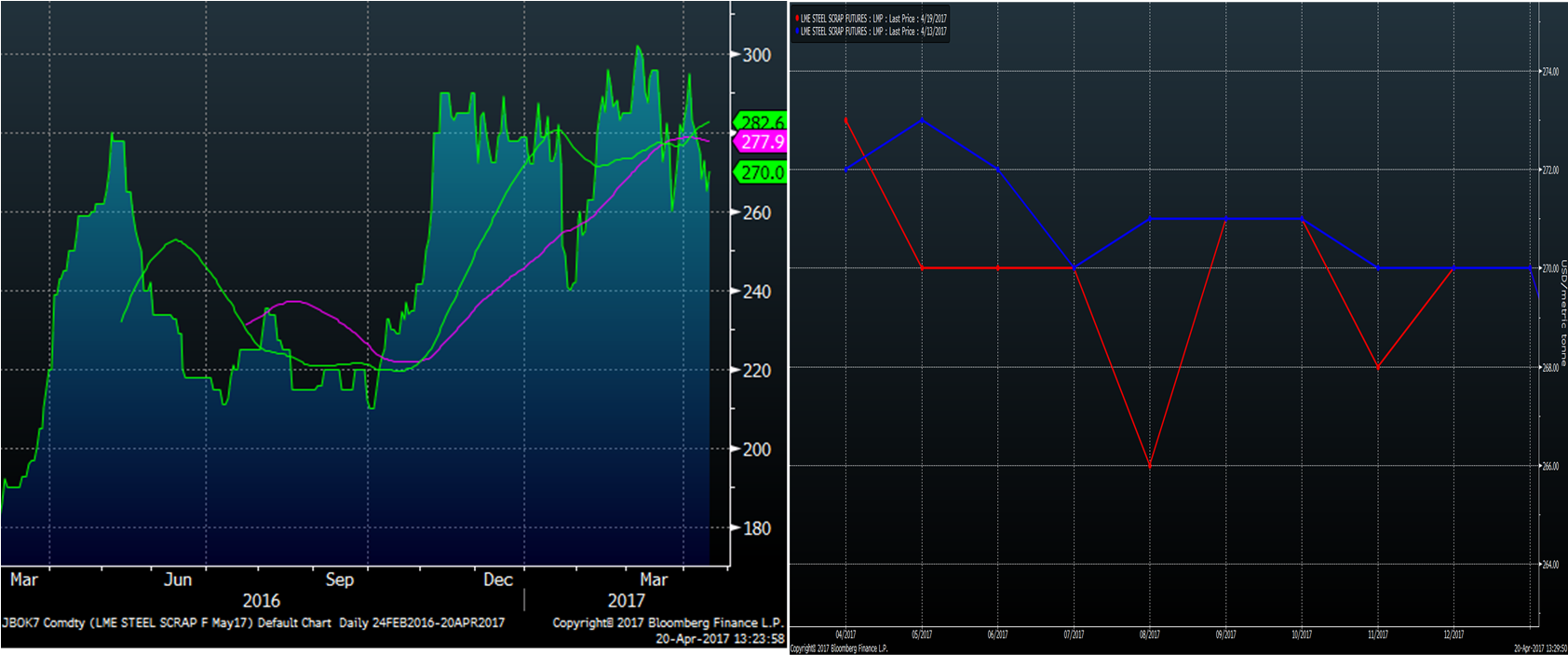

LME scrap has hung in there relatively well considering the sharp move lower in ore. Meanwhile, scrap fell 20% at the end of January and then rebounded 25% by mid-February so go figure.

May LME Turkish Scrap & Curve

Back to the SDI earnings call, Mark Millet said he believes the steel industry “is not in a raw material driven environment, but rather a supply-side driven environment.” If this assumption is correct, buying the dips on raw material volatility may prove to be a solid strategy.

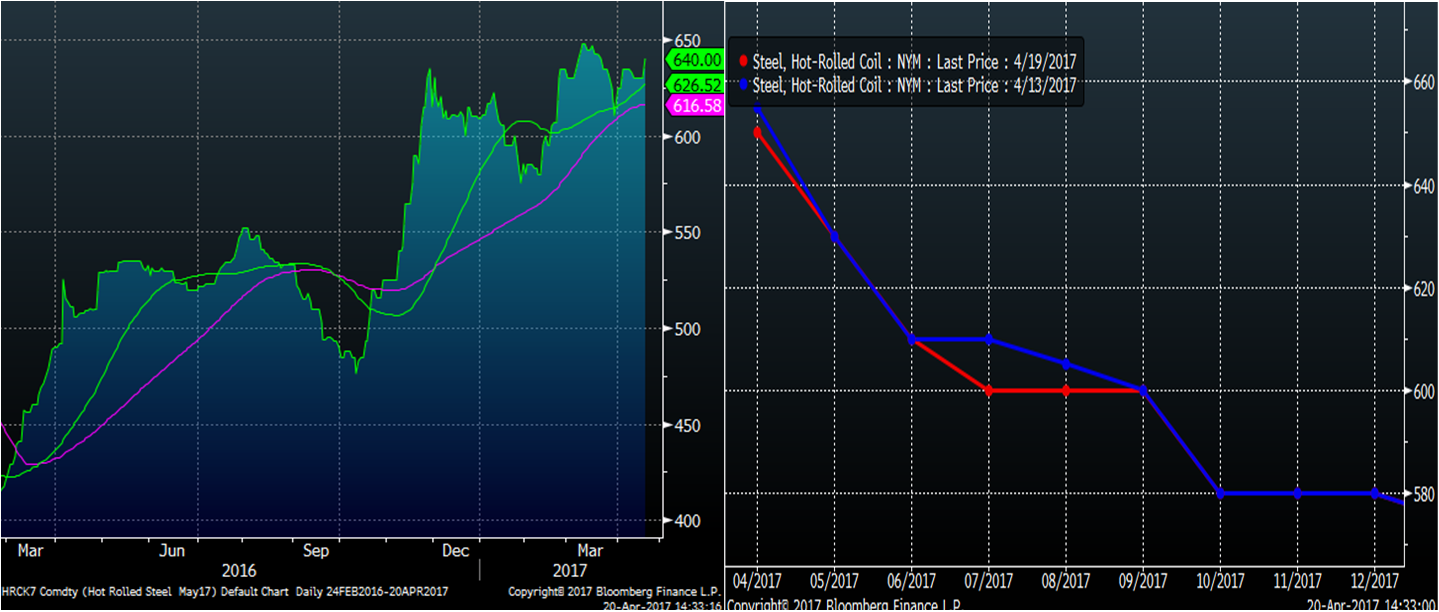

US Midwest HRC indexes remain in the $640 – $650 level. Today, CME Midwest HRC futures traded $640 for 500 May and 500 June short tons, most likely in reaction to President Trump’s signing of an executive order to launch an investigation into imported steel under Section 232 of The Trade Expansion Act of 1962.

May CME Midwest HRC Futures & Curve

The HRC curve remains steeply backwardated, but has started to move up with Q3 now at $600 and Q4 at $585/st. It will be interesting to see the effect this executive order and other government policy developments have on the futures market and the shape of the curve.