Prices

May 4, 2017

HRC Forward Curve Flattens - Relfation Trade Backing Up

Written by David Feldstein

The following article on the hot rolled coil (HRC) futures markets was written by David Feldstein. As the Flack Global Metals director of risk management, Dave is an active participant in the hot rolled coil (HRC) futures market and we believe he will provide insightful commentary and trading ideas to our readers. Besides writing futures articles for Steel Market Update, Dave produces articles that our readers may find interesting under the heading “The Feldstein” on the Flack Global Metals website www.FlackGlobalMetals.com.

Buy the dips……

That’s been the theme of this article for 2017. The fundamentals are a little less stellar this week, but still pretty good. Since our last visit, the most interesting development has been the launching of the Section 232 Investigation by the Trump Administration. The industry looks to be wrapping its head around what it means, but there is definitely a lot of chatter and noise about it.

“Don’t worry, this is my guy. He is an unbelievable guy. The best guy. He is gonna take care of you”

This week’s Week-Over-Week report discusses the issue at length, but the basic idea is that the power held by the Administration to block imports for a certain period seems absolute. An influx of import orders detrimental to domestic steel prices will be met with swift message sending aggression from these guys. Will the threat and uncertainty be enough to hold up Midwest HRC prices and the global differentials at abnormal levels? It happened for almost all of 2014. Don’t fight the fed.

The crux of the “buy the dips” theme has been based on the assumption that the buyers will be quick to scoop up tons if discounted because inventory levels are at historically low levels.

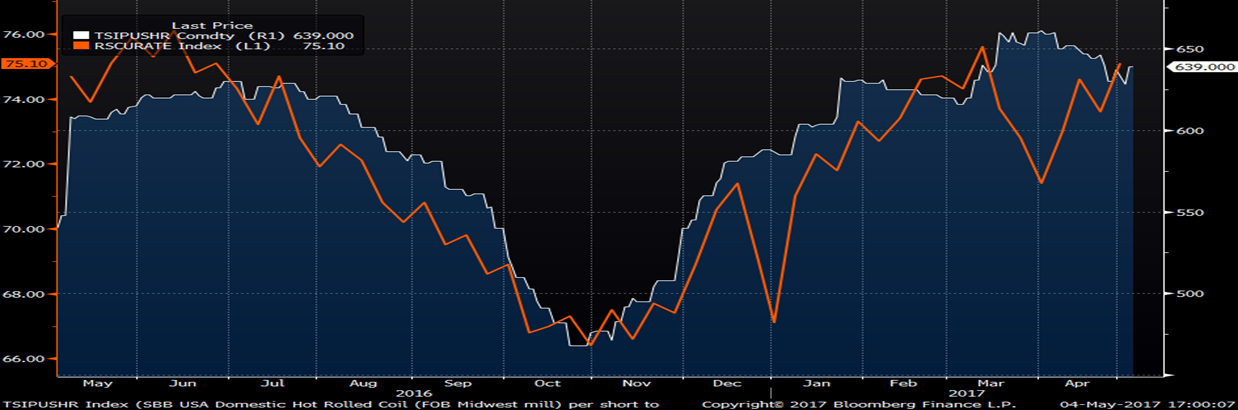

TSI Midwest HRC Index and AISI Capacity Utilization Rate

The AISI capacity utilization rate popped to 75.1, the highest level since March 13th and the TSI Midwest index price increased to $639/st yesterday and held tonight. Does this mean that the shallow dip in prices in past week resulted in increased orders for the mills?

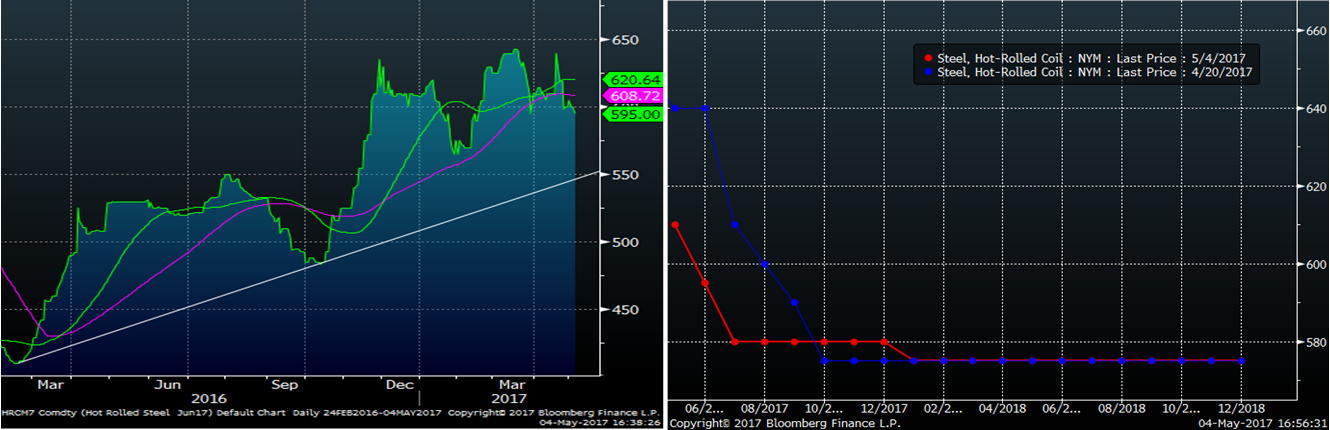

The futures curve has flattened in the $575 – $600 area with the front end falling dramatically.

June CME Midwest HRC Futures & Curve

So is it time to buy the dips?

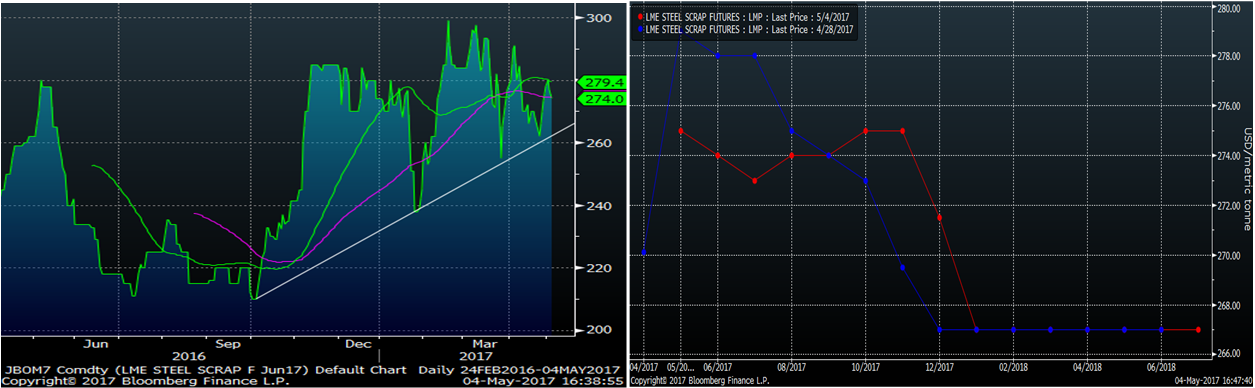

June LME Turkish Scrap & Curve

Another feather in the bull cap has been the resilience in the scrap market. June LME Turkish scrap has held it uptrend closing today at $274/t. Domestic scrap is expected to be flat or up slightly in May.

Then there is iron ore. Iron ore looked to have bottomed, but then tripped all over itself after last week’s Singapore Iron Ore Week conference and is approaching the low of $59.31/t set on April 18th.

June SGX Iron Ore Futures & Curve

Below is the price of buying a put option (in volatility) on June SGX iron ore futures. As you can see, it has spiked and is holding near the highs. What you can expect from this is iron ore futures are going to continue to whip around making big moves in both directions.

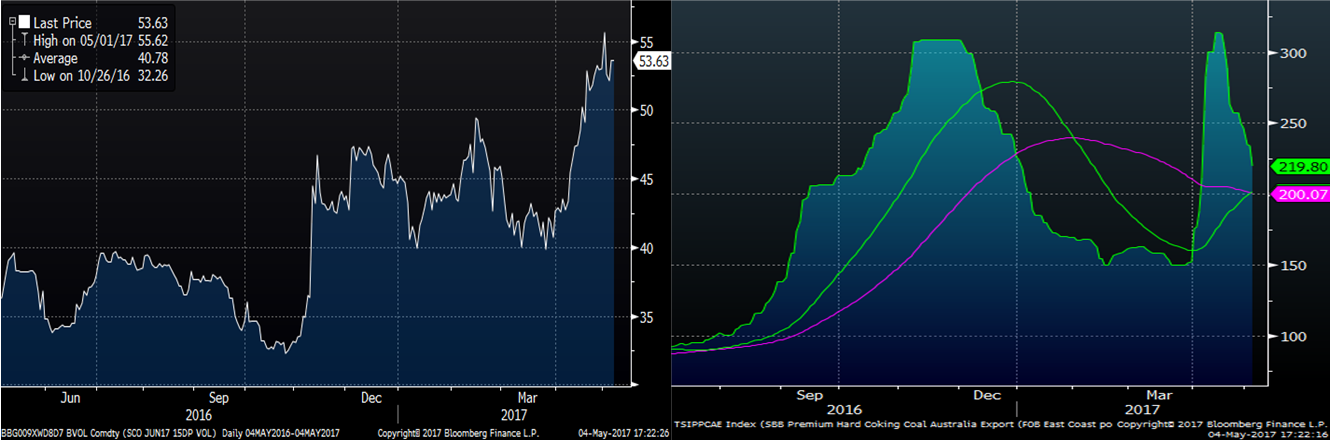

Meanwhile, Australian Coking Coal has plummeted from its $314/t high as expected now that logistical infrastructure in Queensland is back up and running. While the price is coming down fast, it is still $70/t higher than before the cyclone hit and the run up will drive costs higher in coming months for those with coking coal contracts tied to previous pricing of the Aussie coking coal index.

June SGX Iron Ore Futures Volatility and Australian Coking Coal

The most important thing to remember about China is that the 19th National Congress of the Communist Party of China will be held in November. If you understand anything about China’s planned economy, it’s that they will do everything in their power to hold up the economy until this meeting takes place.

The resurgence in the domestic energy industry has been a big part of keeping domestic demand and prices up. So today’s sharp drop in WTI Crude Oil futures is an unnerving development.

June WTI Crude Oil Futures

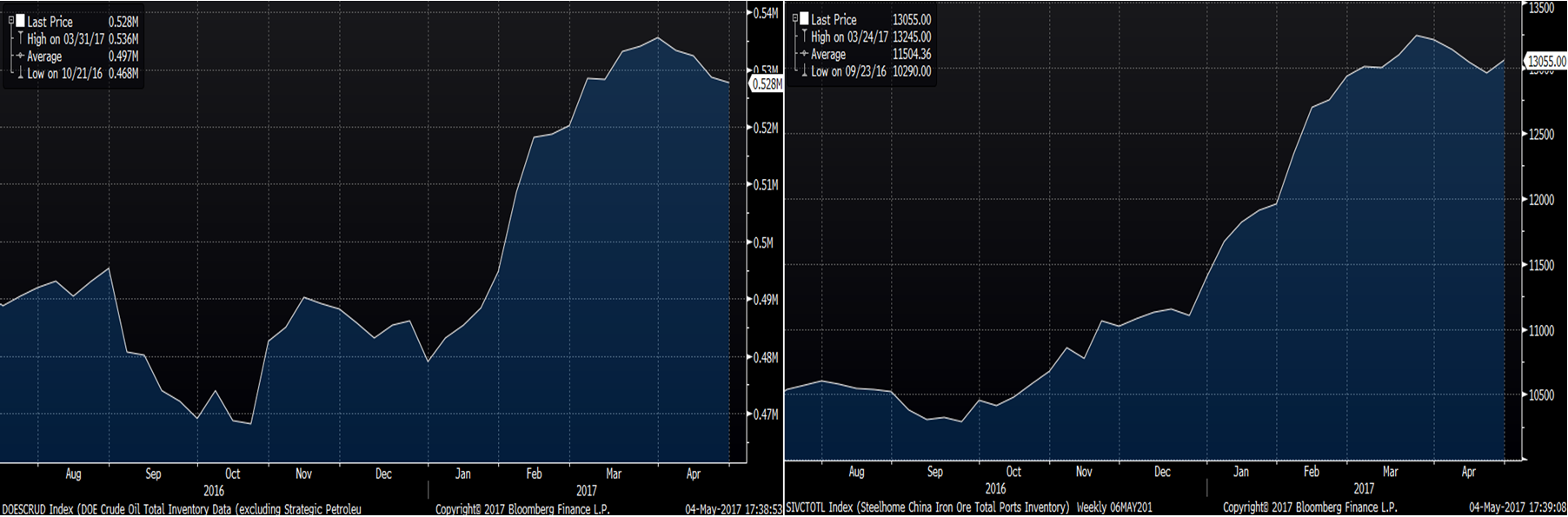

Crude oil and iron ore inventory levels have been building to new highs for months. However, prices stayed strong in both until mid-March. Oil prices rebounded from $47 to $54 while iron ore has failed to rally.

US Crude Oil Inventory and Chinese Iron Ore Inventory

Looking at the charts, if June SGX ore can hold the $58-60 level and crude can hold the $45 level in the short-term, then that will be a great development with a nice double bottom in ore.

June SGX Iron Ore Futures and June WTI Crude Oil Futures

So is it time to buy the dip? HRC hasn’t fallen enough yet to warrant the risk while there is so much sudden pressure on oil and iron ore looks to have head-faked on its recent bottom. If you feel a little queasy though, that’s normal. It is tough sticking your nose out there, but when things look their worst and prices get bizarre that is when you’ll know the reward suits the risk. Just remember there is a lot of support underneath from a stronger economy, low flat rolled inventory levels and a favorable political climate in both the US and China.

The opportunity might present itself in HRC futures in the coming days or weeks, so pay close attention. Keep your local broker on speed dial and remember…

“Life moves pretty fast. If you don’t stop and take a look around once in a while, you could miss it.”