Prices

April 19, 2018

HRC Futures in Steep Backwardation as Upside Risks Mount

Written by David Feldstein

The following article on the hot rolled coil (HRC) futures market was written by David Feldstein. As the Flack Global Metals Director of Risk Management, Dave is an active participant in the hot rolled futures market, and we believe he provides insightful commentary and trading ideas to our readers. Besides writing futures articles for Steel Market Update, Dave produces articles that our readers may find interesting under the heading “The Feldstein” on the Flack Global Metals website, www.FlackGlobalMetals.com. Note that Steel Market Update does not take any positions on HRC or scrap trading, and any recommendations made by David Feldstein are his opinions and not those of SMU. We recommend that anyone interested in trading steel futures enlist the help of a licensed broker or bank.

The U.S. sanctions against Russian oligarch Oleg Deripaska has resulted in his company, Russian aluminum giant United Co. Rusal (Rusal) losing its ability to accept payment in dollars. The sanctions have essentially blocked Rusal, the world’s second largest aluminum producer, from the global financial system. This has immediately halted all deliveries and resulted in a major global aluminum supply shock. The reaction has been powerful with the three-month aluminum future gaining as much as 35 percent in less than two weeks. Not only does global aluminum supply lose Rusal’s production, but also the orders on Rusal’s books all go poof and those orders need to be placed elsewhere, exacerbating the short-term supply shock. Last week, Glencore announced force majeure on 50,000 tons of aluminum expected from Rusal. While this could lead to incremental steel demand to substitute for aluminum in short supply, there is something much larger afoot.

LME 3 Month Rolling Aluminum Future

This week, nickel prices started going vertical on growing fears a fresh round of sanctions against Russia in response to the latest chemical attack in Syria could affect nickel in the same way it has aluminum.

LME 3 Month Rolling Nickel Future

What if additional sanctions have the same effect on carbon products?

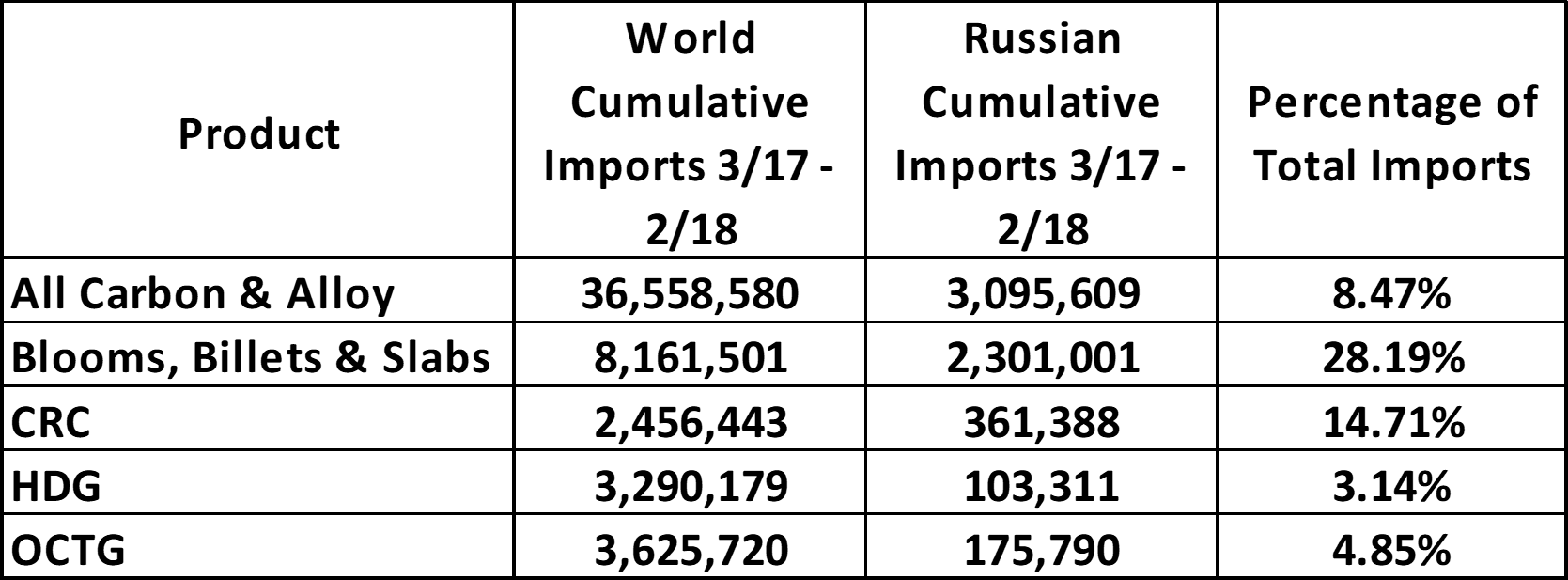

The table below shows the short tons imported in the most recent 12 months from March 2017 through February 2018 (Dept. of Commerce). About 28 percent of slabs imported into the U.S. were from Russia. During this period, Russia accounted for 8.5 percent of U.S. carbon imports and 15 percent of CRC imports. Keep in mind, this is just for the USA.

To give perspective on the size of this potential supply disruption, below is a list of domestic steel mills with annual flat rolled production close to Russia’s cumulative carbon imports.

Whether or not Russian steel imports are taken offline is uncertain, but it is clearly a major risk. That risk in and of itself should depress demand for Russian import. Would you want to take the risk of Russian import in this market?

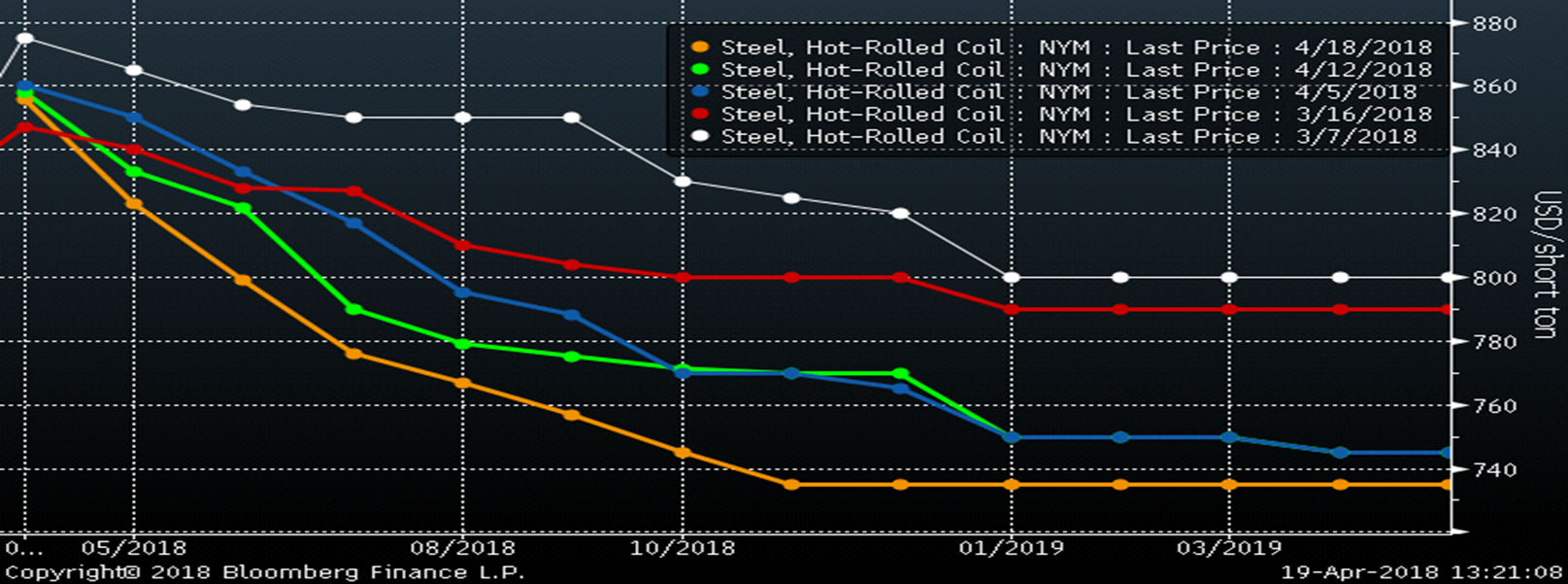

The Midwest HRC futures have been under pressure, now sitting at their lowest level since peaking on March 7. The market has yet to reflect this risk or a number of other very real upside risks still affecting the domestic flat rolled market. The market seems complacent that the recent influx of import orders will resolve the supply constraints of the 232 tariffs and quotas.

May is trading around $830, an almost $30 discount to this week’s index print. June traded as low as $800, while Q3 traded today at $775 and Q4 at $750.

This week, rumors surfaced that U.S. Steel Great Lakes Works was facing operational issues forcing the mill to go down for maintenance for three to four weeks. Then yesterday, ArcelorMittal sent out an internal memo raising prices for HRC back to $900/st from $850. Today’s Q3 and Q4 trades should move the settlements higher by $10 to $15.

There is a fallacy that a curve with massive backwardation (downward sloping) reliably predicts physical prices will fall by year end. The reality is these are the prices at which market participants have found equilibrium. What the curve is telling you is that you can lock up steel in Q3 at $775 and Q4 at $750. If that makes you a profit on a fixed commitment to your customer for those periods, then it’s a great way to lock up profit and mitigate the risk that prices stay elevated in the $800s or go higher.

CME Midwest HRC Future Curve

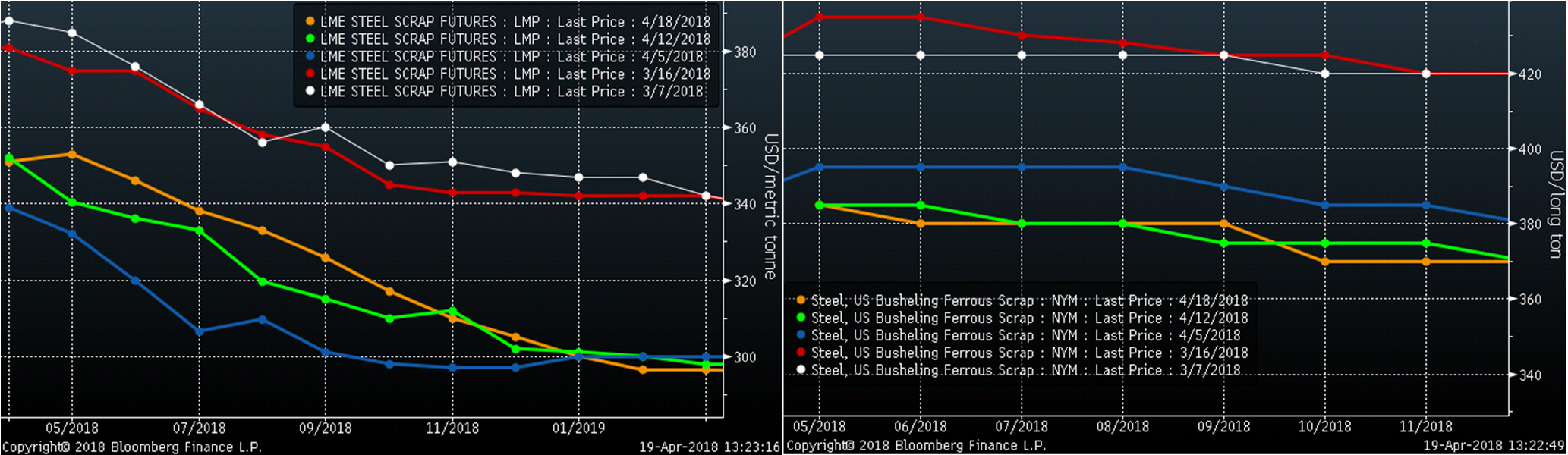

Turkish scrap futures have rebounded after hitting lows on April 5. The May LME Turkish scrap future settled at $348 today. The May busheling future continues to make new lows, settling last night at $380.

LME Turkish Scrap (left) & CME #1 Busheling (right) 2nd Month Rolling Future

The SGX 2nd month iron ore future has bounced nicely off its multi-year uptrend line (red dashed) as rebar and a number of global commodities (oil, copper, aluminum, nickel) have rallied sharply over the past few trading days.

SGX 2nd Month Iron Ore Future

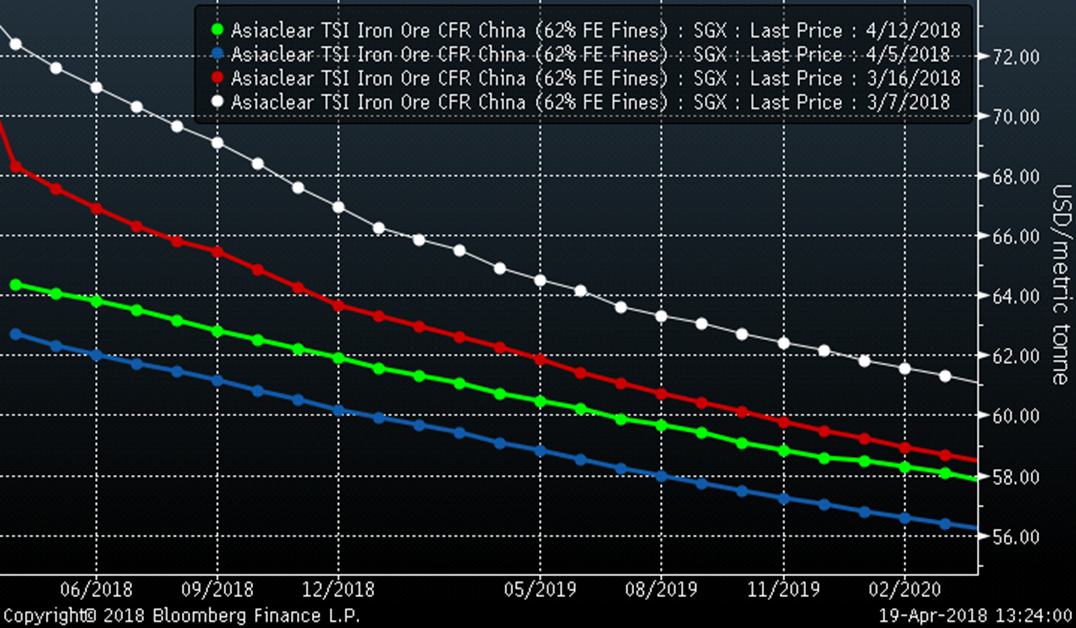

Iron ore prices are down since last month, but have been rebounding and currently look to be attempting to rally off recent lows.

SGX Iron Ore Future Curve

The stock market traded up to the down trendline yesterday and has thus far failed to break above it. Not a great sign for the market and if it goes back into sell off mode, watch the 2530 (red dashed line) level. If the S&P 500 closes below that level, the market is likely in for a serious correction.

S&P 500 June Future