Prices

May 24, 2018

May Steel Imports Trending Toward 2.5 Million Ton Month

Written by John Packard

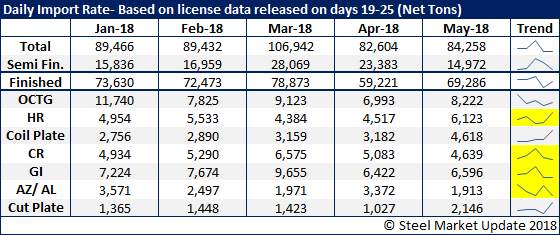

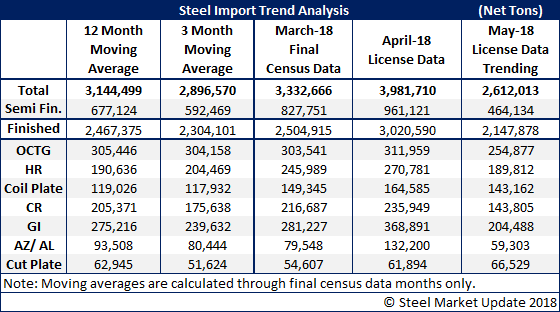

Based on the latest license data from the U.S. Department of Commerce reported earlier this week, we are expecting the trend for May steel imports to total 2.5 million to 2.6 million net tons. We continue to see strength in plate imports, in both coil and sheet. Finished imports are trending toward 2.1 million net tons, which if correct would be approximately 900,000 net tons lower than what was received during the month of April.

OCTG (oil country tubular goods), hot rolled, cold rolled, galvanized and Galvalume are all trending lower than what we saw in April.

Below is a table we use along with a graphic depicting how imports have been trending during the first 19-25 days of a month. What is shown is the daily import license rate, and the May rate is compared against that of April, March, February and January 2018. We are seeing a rising trend in hot rolled, coiled plate and cut plate. All of the other flat rolled items (shaded yellow items) are trending lower.