Market Data

June 17, 2018

As We Prepare for the Next SMU Steel Survey

Written by John Packard

Twice each month, Steel Market Update conducts a review of the flat rolled and plate steel industries. We do this through a web-based questionnaire, which is sent to approximately 640 individuals associated with either the flat rolled or plate steel industries. The individuals invited are from manufacturing, steel distribution, steel mills, trading companies and toll processors.

Our last analysis was conducted during the first week of June (4-6) and was published to our Premium level members on Friday, June 8. Our Premium level members have access to a PowerPoint presentation we put together for each and every survey we conduct.

The early June questionnaire saw 46 percent of the respondents as being service centers/wholesalers, 38 percent manufacturing companies, 8 percent trading companies, 5 percent toll processors and 3 percent steel mills. We intentionally weigh the invitations heavily toward the manufacturing and distribution portions of the industry since they represent the steel buyers in North America.

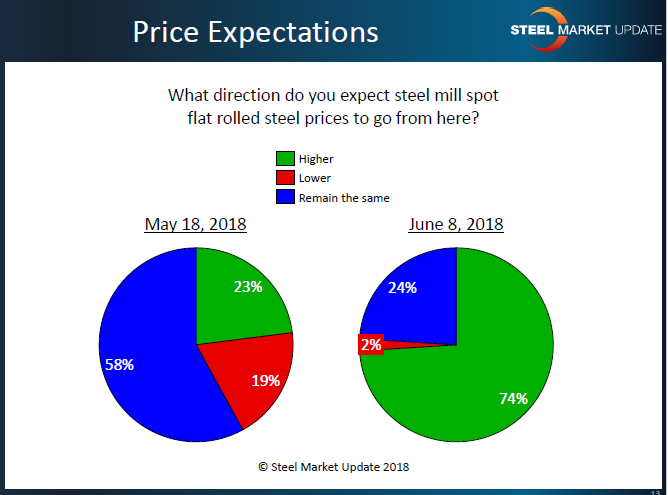

From survey to survey, we can spot radical changes in trends. Here’s a good example. Over the past couple of surveys, we asked all of the respondents to share their opinions as to the direction spot mill flat rolled prices were likely to go from here (the first week of June). As you can see by the graphic below, in the middle of May, 58 percent believed prices would remain the same, 23 percent thought they would go higher and 19 percent believed spot prices would actually move lower.

Move ahead by a couple of weeks and the opinions have shifted as 74 percent believe prices would move higher, 24 percent thought prices would remain the same and only 2 percent (two) were convinced prices would move lower. What changed during that two-week period? The U.S. government announced that Canada, Mexico and the European Union were no longer excluded from the Section 232 steel tariffs.

Several respondents left comments regarding the question of pricing’s direction:

• “It’s all dependent on the current Section 232 and if countries are exempted, and if applied for product exemptions are accepted or rejected.”

• “The stage has been set again for the mills to try to push a price increase. Whether or not it will stick will depend on the strength of demand. Even more of a concern will be just how tight this market will get and how available steel will be.”

• “Higher for a few weeks more, but expect pricing to decline rapidly towards the end of the third quarter.”

• “Probably will go higher, but ultimately will be controlled by foreign prices, which are currently more than 25 percent below domestic prices.”

• “Based on the 232’s shutting out Canada, the mills will seize the opportunity to take us all for a Toronto sleigh ride.”

• “Slightly higher, but I think the big push will be for the steel producers to try to lock today’s high prices and market confusion into their 2019 contract negotiations.”

• “Uncertainty will keep prices high.”

Prices Are Affected by Supply – Will There be a Shortage Later This Year?

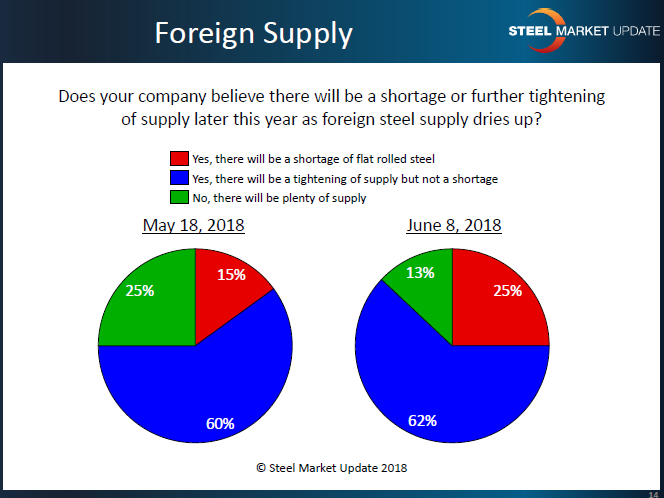

Despite the changing opinions regarding the direction of pricing, our respondents have remained consistent regarding their belief there will be a “tightening” of supply later this year. We saw growth in the opinions of our respondents from mid-May to early June that there would be a shortage of steel. At the same time, the percentage of respondents who believe there will be plenty of supply shrunk to 13 percent.

Respondents left behind some thoughts on this question, as well:

• “If the foreign supply dries up, the domestic mills won’t be able to produce enough steel to supply demand. Tight supply/long lead times/no other options puts the domestic mills in the driver’s seat and prices sky high.”

• “Ramping up domestic capacity will take 2-3 quarters. It would have been faster if the situation on trade disputes was clear. During those 2-3 quarters, there will be a shortage. If the trade disputes are settled favorably, new efficient capacity will be added domestically.”

• “It’s product dependent. Pipe and tube might be short, as well as some flat rolled products like Galvalume, but others might be okay.”

• “I don’t understand why foreign steel supply would dry up. Domestic is running in lockstep with the tariff increases and FOB world market pricing is not. Steel will always be available at a price.”