Government/Policy

August 16, 2018

CRU: Tariffs Not Conducive to GDP Growth

Written by Sandy Williams

The U.S. trade situation is causing some consternation, according to analysts at CRU. During a webinar on Tuesday, which was made available to SMU member companies, analysts discussed the trade measures that have been instituted by the Trump administration and the potential impact on the U.S. and global economies.

Steel and aluminum tariffs were imposed under Section 232 on the grounds of national security and as a result steel prices have climbed sharply along with profits at domestic steel producers. The administration expects tariffs to improve U.S. steel capacity utilization rates and spur expansion as competition from steel imports declines.

Although there have been some furnace restarts and expansions for sheet and long products that were supported by Section 232 tariffs, said CRU Analyst Estelle Tran, market conditions supported those intentions before the tariffs. Capacity utilization increased in the first quarter supported by seasonal restocking and manufacturing demand. So far, capacity utilization has not reached 80 percent, according to AISI, though CRU expects utilization rates to reach the 80 percent target this year, at least temporarily.

The recent doubling of duties on Turkey will make Turkish steel uncompetitive in the U.S., prompting cancellation of orders due to arrive later this year.

Section 301 tariffs on China have escalated with the administration placing 25 percent tariffs on goods worth $34 billion, $16 billion and possibly 25 percent tariffs on an additional $200 billion. Although most of the trade war with China is focused less on metals and more on autos and soybeans, Tran said it shows the ”administration is willing to accept hits to downstream manufacturers in its broader trade negotiations.”

Additional pressure is added to the market by the ongoing negotiations of NAFTA and a Section 232 proposal that would place tariffs on imports of autos and auto parts.

CRU economist Lisa Morrison said the trade issues are likely to impact gross domestic product. GDP is derived from personal consumption, government spending, private fixed investment, export of goods and net export of services minus the value of imports. The U.S. currently imports about 50 percent more than it exports.

The cost of the tariff is borne by the importer, said Morrison. “If you raise the cost of imports, what you essentially do is reduce the overall value of your gross domestic product, your national wealth, in the near term until there is time for the physical flows to adjust.”

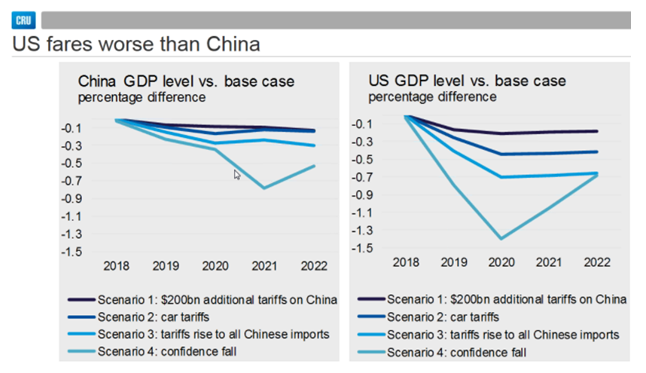

CRU analyzed four scenarios to determine the cumulative effects of tariffs on GDP for both China and the U.S. The scenarios include the 10 and 25 percent tariffs on aluminum and steel and the first two Section 301 measures against China. The analysis was completed before the tariffs were increased from 10 percent to 25 percent for the $200 billion measure and does not include the effect of retaliatory tariffs.

- Scenario 1: Additional 10 percent tariffs on $200 billion in Chinese goods

- Scenario 2: Scenario 1 plus 25 percent tariffs on autos and auto parts

- Scenario 3: Scenario 2 plus tariffs of 10 percent on all Chinese imports

- Scenario 4: Scenario 3 plus falling global business and investor confidence

In all cases, GDP is lower with the U.S. suffering more than China due to the exclusion of retaliation in the scenarios. Confidence shock occurs, but the U.S. recovers more quickly (2022) than China due to its cutting out the U.S. market and hurting Chinese economic growth potential. Overall, global GDP declines, but recovery from the confidence shock from trade actions takes until 2024. The overall global economy will see much lower growth due to the initiation of U.S. trade actions. If retaliation is accounted for, it will make growth levels decline even further.

In the chart below, CRU looks at the various trade conflicts and risks to growth.

In no case does any country gain from the scenarios, said Morrison. If dissolution of NAFTA would occur, for example, Canada and Mexico will suffer lower growth, but so will the United States. The U.S. vehicle tariffs would be extremely dangerous because of the integrated nature of the sector.

“Trade exists in order to allow an economy to grow outside of its borders,” said Morrison. “If you raise a tariff, you are really raising costs for your own domestic market, and if you are a country that retaliates to a tariff, you’ve gone ahead and done the same thing.”

“From an economic standpoint, it is not particularly constructive in terms of GDP growth,” added Morrison.

How will the trade battles turn out? Morrison believes that NAFTA will be renegotiated if the parties can reach agreement on a longer sunset provision.

The trade battle with China will escalate with further retaliations. China’s tariffs may become higher than U.S. tariffs—not a like-for-like situation, said Morrison. The U.S. could lower some of the tariffs if China is willing to make progress on non-tariff barriers that will give Trump a win.

Morrison believes there will be tariffs on autos and auto parts after seeing the willingness of the administration to impose the steel and aluminum tariffs.

“I honestly was incredibly shocked that there were tariffs put on steel and aluminum,” said Morrison. “I couldn’t quite believe that we would sacrifice the health of downstream industries for that of upstream industries where we don’t necessarily have such a large competitive edge.”

Transplanted production may still be able to bring in parts from offshore to be assembled in the U.S., but the extra cost due to tariffs will squeeze margins. Morrison expects tariffs to hit SUVs and light trucks the most, but a sliding scale may be possible for smaller cars.

Trump’s proposition of total free trade with no tariffs is a “lovely thought,” but will not be happening in Trump’s term, said Morrison.

CRU Principal Analyst Josh Spoores spoke about the impact of Section 232 on the sheet markets in the United States and provided a price forecast for benchmark hot rolled coil and plate steels. Spoores will be one of the speakers in Atlanta at the 8th SMU Steel Summit Conference. Those who missed his comments during this week’s webinar can hear him speak on Wednesday afternoon at SMU’s conference.