Prices

September 23, 2018

Where’s the Beef, Part Two, Unintended Consequences

Written by John Packard

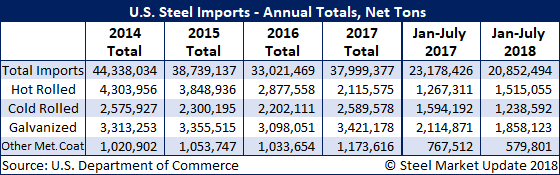

When looking at the last four years of import data, as well as the first seven months of data available from the U.S. Department of Commerce, we are seeing a reduction in most flat rolled products.

Of the past four years, 2014 was by far the biggest year for foreign steel imports into the United States. The U.S. received 44,338,034 net tons that year. The following year, the domestic steel mills went on the war path filing antidumping and countervailing duty suits against all of the products referenced in the table below. Imports that year fell to 38,739,137 net tons. In 2016, when the AD/CVD suits were finalized, imports dropped to their lowest level of the time period under consideration, just topping 33 million net tons.

In 2017, President Trump announced the Section 232 investigation, and domestic buyers once again went back to their foreign suppliers for more steel. During calendar year 2017, foreign steel imports totaled 38 million net tons, an increase of 5 million tons compared to the previous year.

SMU spent some time taking a look at the imports of hot rolled, cold rolled, galvanized and other metallic (the vast majority of which is Galvalume) to see what trends we could find in the numbers.

Hot rolled imports peaked in 2014 at 4.3 million net tons for the year. Since then, HRC imports declined each year over the following three years. In 2017, total HRC imports bottomed at 2.1 million net tons.

During the first seven months of 2017, HRC imports totaled 1,267,311 net tons. In contrast, during the first seven months 2018, HRC imports rallied and are about 300,000 net tons above 2017 levels. HRC imports, if they continue at the pace reported during the first seven months of the year, are on pace to reach 2.5 million net tons during 2018. This is still well below the levels reported in 2014, 2015 and 2016.

Cold rolled has been more resilient than hot rolled. Cold rolled imports peaked during 2017 at just shy of 2.6 million net tons, almost the same as the 2.575 million tons reported during 2014. The lowest year for CRC imports was the all-important AD/CVD decision year of 2016 when CRC imports dropped to 2.2 million net tons.

So far this year, cold rolled imports are trending lower than the peak of 2017. For the first seven months, CRC imports were 250,000 net tons below 2017 levels. If CRC imports continue at the pace of the first seven months, we can expect 2.1 million net tons of CRC to come into the country during 2018.

Galvanized is another resilient product having exceeded 3 million net tons of imports each of the past four years. Last year was the biggest year for GI, reaching 3.4 million net tons. However, the 2017 total was not that far away from the 3.3 million net tons recorded in both 2014 and 2015.

For the first seven months of 2018, we are seeing a drop in GI import levels. Imports are down 256,000 net tons and, if the year continues at its current pace, it’s looking like another 3-million-plus ton year for galvanized (3.1 million net tons).

Galvalume (other metallic) is another resilient product exceeding 1 million net tons in each of the four years. The biggest year for imports of AZ was 2017. When looking at the first seven months of 2018 compared to the same period in 2017, AZ imports are much lower. The import numbers suggest we will see 2018 finish just below 1 million net tons.

As was mentioned in the article above, U.S. buyers of steel continue to favor their suppliers of choice. This includes continuing to buy foreign steel. With the domestic mills raising prices well beyond the foreign plus 25 percent threshold, domestic buyers are incentivized to continue to buy foreign steel.

At our 2018 SMU Steel Summit Conference, we asked those in attendance to comment about their buying habits, and if they intended to continue to place foreign steel tonnage or would they be moving those tons to domestic sources. We shared the results with Nucor CEO John Ferriola during our one-on-one interview with him on stage. He was surprised, as were many in the audience, that only 4 percent of the respondents were moving foreign orders to domestic suppliers.