Long Products

September 7, 2019

CRU: Pressure Continues to Mount for U.S. Long Product Prices

Written by Tim Triplett

By CRU North America Analyst Ryan McKinley

U.S. long product price declines were limited for most products in September after finding support from the scrap market, but downward pressure continues to mount. Even with scrap prices rising by $20 /l.ton in August, persistent price falls throughout the year have yet to spur buyers’ interest amid high inventory levels, especially for wire rod. As a result, mills have had to compete harder to secure the little demand that does exist in the market. The exception to relative price stability was for beams, with mills announcing price decreases of $3.00 /cwt in mid-August.

For wire rod, September’s decline is the seventh month in a row that prices have fallen and marks the month that prices reached parity with pre-Section 232 prices. This constant decline, however, has failed to generate any buying interest and mills continue to cut deals to keep cash flowing. The lack of buying interest has pushed low carbon wire rod prices under rebar prices, with the two inverting for the first time since March 2018.

With the seasonally strongest months now behind, market participants are growing increasingly bearish about the remainder of the year. This concern is limiting interest in imports, especially given the relatively small spread between import and domestic prices. Wire rod imports license data totaled 64,000t in August, according to U.S. Census Bureau data. This is a 15 percent decline in imports m/m and a 40 percent decrease y/y.

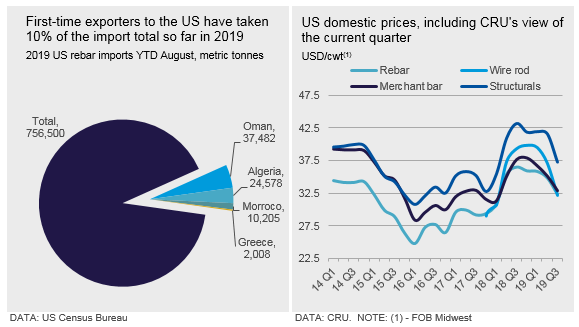

Rebar imports in August are on pace to be at their lowest level since December 2018. While the 40,800t total is a decline of 48 percent m/m and 69 percent y/y, Turkish exporters have become more competitive and have cargoes on the water heading to the U.S. Other, non-traditional, exporters like Oman have found openings as well in 2019, with first-time exporters to the U.S. capturing a tenth of total import volume so far (see chart). Market participants put import prices for rebar DDP Gulf Coast at $31.50 /cwt.

The decline in import volumes coupled with an uptick in scrap prices prevented further price declines for domestic rebar. Fabricators still report solid demand for the next 6-9 months, but it is unlikely that construction projects, which were delayed earlier in the year, will catch up after falling behind schedule. Mills are also positioning for seasonally weaker demand by destocking.

Outlook: Scrap Oversupply Adds to Pressure

Scrap prices are poised to drop by $20-40 /l.ton over the next 60-day time period with a glut of supply available to the market in September and scheduled mill outages in October. This, in addition to construction projects that are behind schedule and high inventory levels, will likely keep downward pressure on long product prices near term. Demand is typically weaker in November and December, which means the likelihood for any price increase for the remainder of 2019 is remote.