Product

January 9, 2020

Hot Rolled Futures: The Bull is Back!

Written by David Feldstein

The following article discussing the global ferrous derivatives markets was written by David Feldstein. As an independent steel market analyst, advisor and trader, we believe he provides insightful commentary and trading ideas to our readers. Note that Steel Market Update does not take any positions on HRC or scrap trading, and any recommendations or comments made by David Feldstein are his opinions and not those of SMU or the CRU Group. We recommend that anyone interested in trading steel futures enlist the help of a licensed broker or bank.

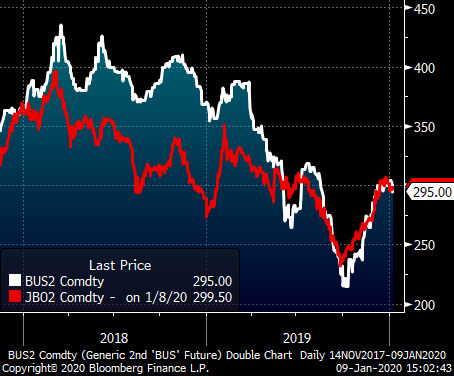

January CME busheling looks to settle tomorrow up $30 at $296. CME busheling and Turkish scrap remain in lock step with one another and have been in a tight range between $290 and $310/t.

Rolling 2nd Month CME Busheling Future (white) & LME Turkish Scrap Future

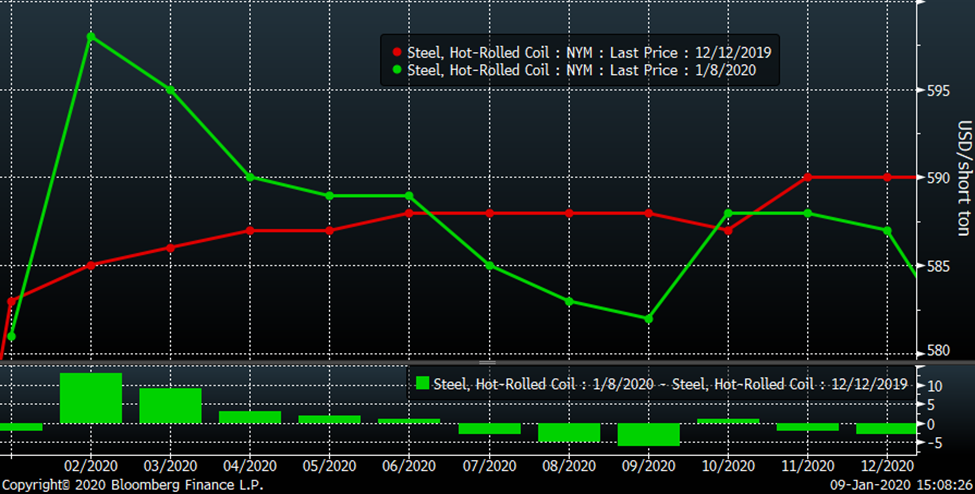

The CME Midwest HRC futures market was very quiet and rangebound throughout December. This week, the February and March futures have been moving higher with February trading as high as $605 on the screen today. Also today, a block trade of 6k tons per month for February, March and April (18k total) traded at an average price of $594. The muted reaction to U.S. Steel’s unplanned outage at Gary Works, announced closure of its Great Lakes mill and ArcelorMittal’s accident at its Indiana Harbor #4 BOF has been surprising. The curve remains essentially flat.

CME Midwest HRC Futures Curve

2019 was a tough year for the steel and manufacturing industry. It was tough for the mills, OEMs, service centers and scrappers. Last year’s price action was unrelenting leaving many in the industry flat out depressed. Service centers did their best to collectively destock and are now holding the lowest level of flat rolled inventory since 2010. The good news is 2019 is over. It’s 2020 and not only is the bear market over, but I see a scenario for a big rally in the coming months.

Rolling 2nd Month CME Midwest HRC Future

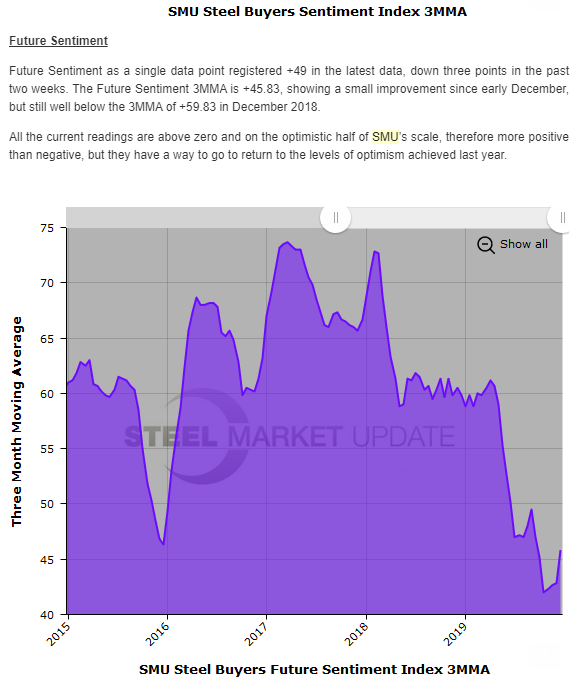

The regional Fed purchasing managers indexes, the ISM Manufacturing Index and the SMU Steel Buyers Sentiment Index are all in the gutter, more or less. These are sentiment indexes. They are a gauge of attitudes, opinions, expectations, etc., and all are indicating buyers are still in the fog of 2019. They are in risk off mode.

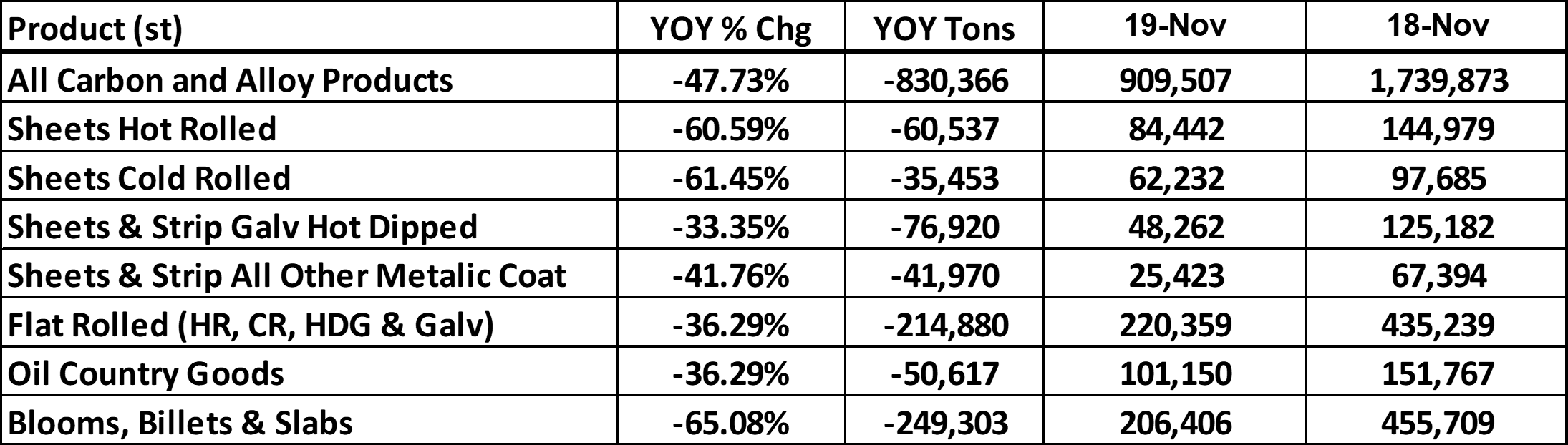

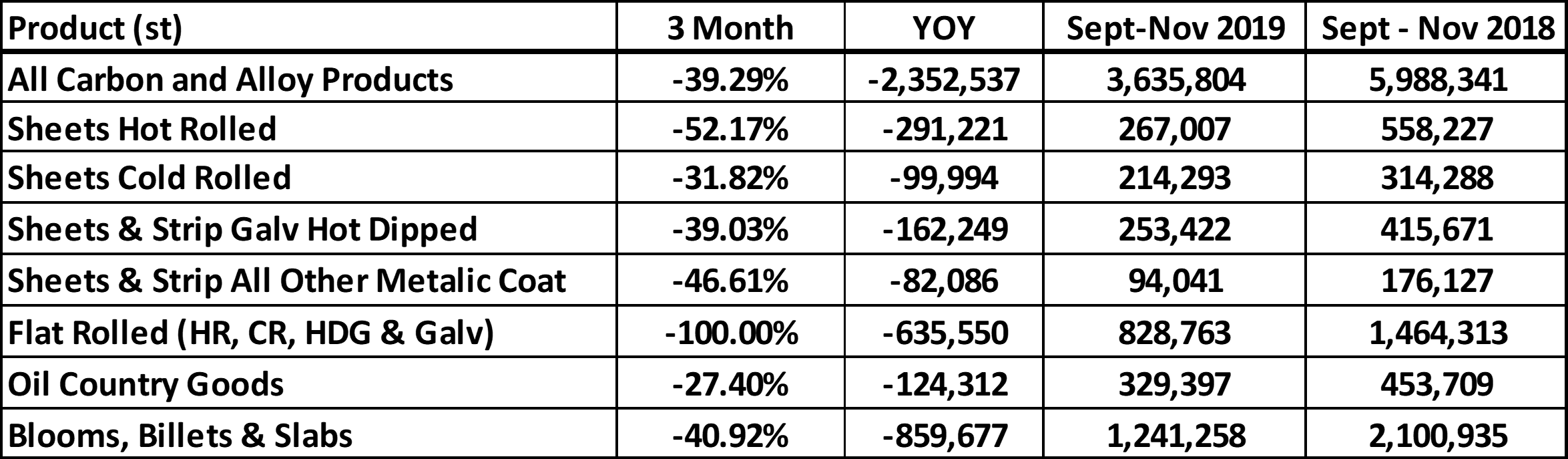

A rationalization of steel inventory has taken place in 2019. As stated above, service centers are holding dramatically lower inventory. These two tables look at net imports—imports minus exports. November data shows a significant drop in tons on a YoY basis in all categories. Taking just the four largest flat rolled categories, 215k less tons were imported in November 2019 vs. November 2018.

This next table is like the one above, the difference being it compares the total net imports over the three-month periods from September through November 2019 and 2018. The YoY decrease in the four flat rolled categories sums to 636k tons over the three-month period, which equates to an annualized decrease of 2.54m flat rolled tons. That is approximately the annualized capacity of Nucor Berkeley, Nucor Decatur and Nucor Crawfordsville (individually). SDI Butler’s annual capacity is 3m and SDI Columbus is 3.4m. The cut in imported flat rolled equates to one of these EAFs going down for a year. That’s a lot of tons!

Sentiment is in the dumps. The industry is shuffling their feet into 2020 still in the fog of 2019. I say pick your heads up and start dialing because the cavalry is coming, they’re wearing a hard had and riding a bull!

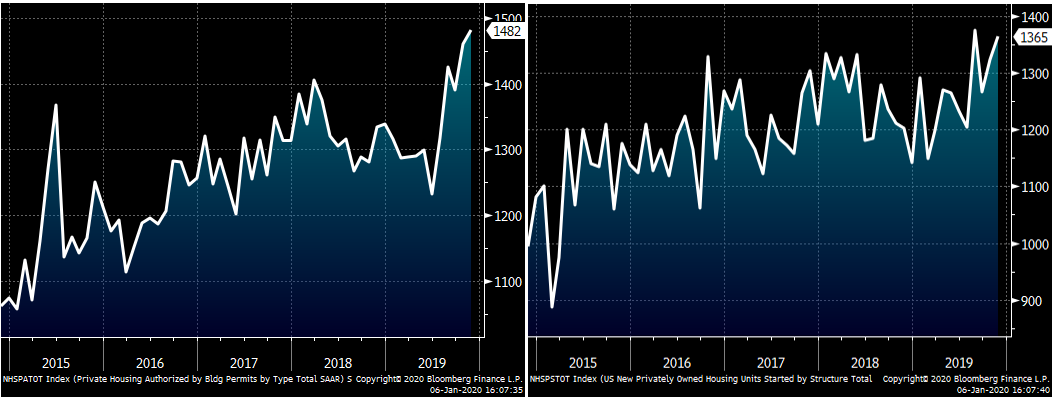

These next few charts are very exciting indicating a boom in housing in 2020. Building permits exploded higher in November, perhaps a sign of what’s to come, and housing starts have followed suit reaching their second highest SAAR since 2007.

U.S. Building Permits (left) & Housing Starts (right) SAAR

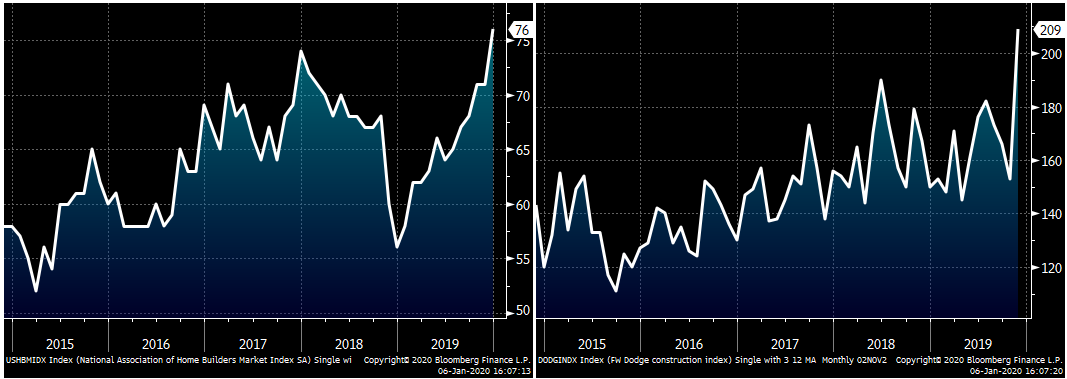

While sentiment in the steel industry and the ISM are in the tank, sentiment in the construction industry has exploded near record highs. The National Association of Home Builders Housing Market Index ripped higher to 76 in December, the highest level since 1999. The Dodge Construction Index jumped a whopping 56 points to 209 in November, its highest level ever.

The fact that these dramatic jumps are lining up across these data points increases the reliability that demand in construction will significantly exceed expectations.

NAHB Market Index (left) & Dodge Construction Indexnhsp (right)

The setup is bullish. The steel industry is relatively low on inventory, low on attitude and high on complacency. An upside surprise from construction, which accounts for 40 percent of demand, will catch the steel industry off guard. Longer lead times and bottlenecks in supply could result in restocking at OEMs and service centers, driving prices higher.