Prices

March 3, 2020

CRU: Global Growth Lowered Due to Covid-19

Written by Jumana Saleheen

By CRU Chief Economist Jumana Saleheen, from CRU’s Steel Sheet Products Market Outlook

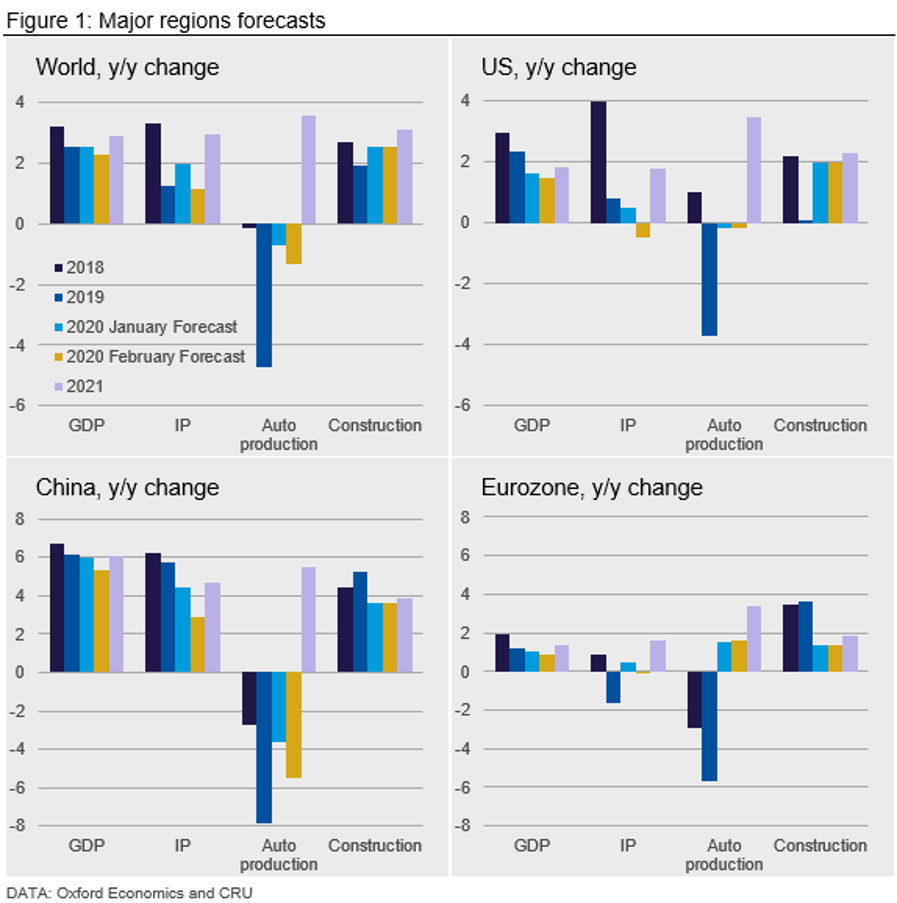

Two pieces of news have led us to lower our global forecasts for 2020. First, disruptions caused by the Covid-19 epidemic are expected to lead to a sharp downturn in near-term global growth, followed by a sharp recovery later in the year. Second, weaker than expected industrial production data suggests that the global slowdown which started last year will continue into 2020. At the time of this writing, fears of a global pandemic have increased. Such a scenario would lead to further lowering of our forecasts.

Two Pieces of Bad News: Covid-19 and Weak World IP

The Covid-19 epidemic has dominated headlines since mid-January. The human and social cost has been heavy, disrupting the normal patterns of life primarily in China, but more recently in some areas outside China as well. The outbreaks in Italy, Iran and South Korea have ignited fears of a global pandemic, leading major equity indices to fall by around 10 percent.

Even under the optimistic scenario of successful virus control, global growth forecasts now need to be lowered. CRU has reduced the 2020 GDP growth forecasts: for China by 0.4 percentage points (pp) to 5.3 percent; and for world GDP growth by 0.2pp to 2.3 percent. The last time world growth was this low was during (but not at the trough of) the Global Financial Crisis. Full IP data for all countries for 2019Q4 is still not available. However, data released this month suggests that IP is likely to continue to weaken in 2020. World IP growth was cyclically strong in 2018 at 3.1 percent. We had not expected that high rate to continue, but we had expected 2019 to mark the cyclical trough, followed by a mild recovery in 2020 to 2 percent. Recent weaker IP data and the impact of Covid-19 mean that world IP growth is now forecast to slow to 1.3 percent in 2019 and then to 1.2 percent in 2020; a recovery to 3.1 percent in world IP is expected in 2021.

At the time of this writing, the risks of a global pandemic are rising; should those risks materialize it would lead to further lowering of our forecasts.

Short-term Damage to Growth is Greatest in China

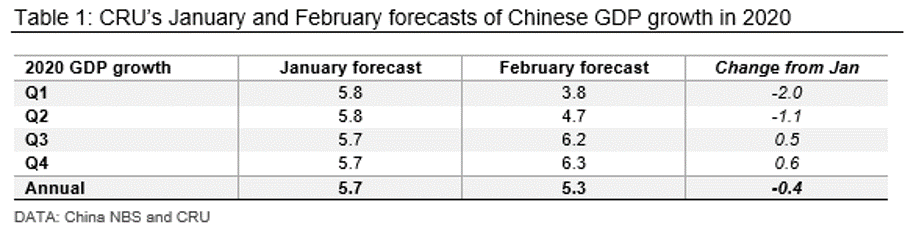

Covid-19 will cause most damage to economic activity in China. The lockdown of the industrial province of Hubei and constraints on the movement of people throughout China have already reduced consumption and disrupted supply chains. We have revised our 2020 GDP forecast from 5.7 percent down to 5.3 percent. Our base case forecast, built on our analysis and information from CRU’s China offices, is that the impact will be short-lived and will result in a sharp recovery in the third quarter. The table below compares our quarterly forecasts made in January and February; we have reduced our forecasts for Q1 and Q2 but increased those for Q3 and Q4. This month we have also cut our forecast of Chinese auto production in 2020 from -3.5 percent to -5.5 percent. More details are given in the China section of this report.

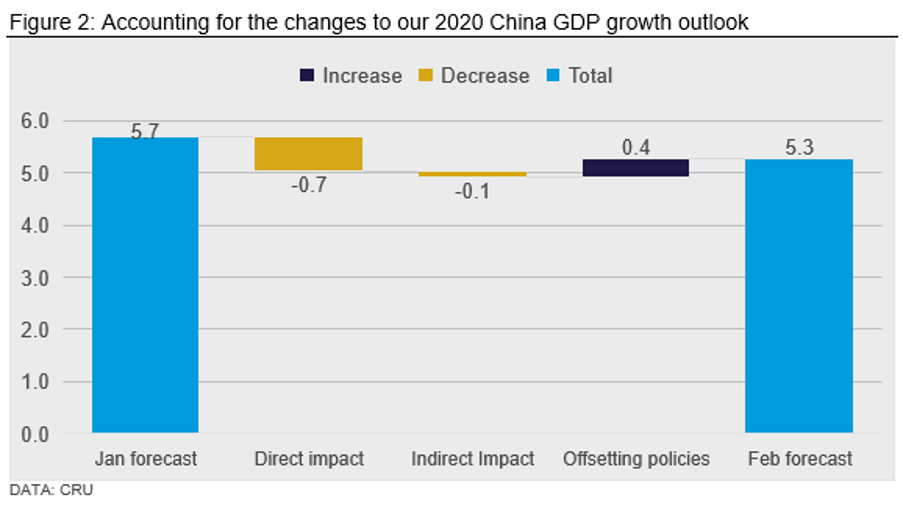

Modeling the Impact of Covid-19 on the Chinese Economy

We expect the Covid-19 epidemic to affect the Chinese economy in three ways: directly, indirectly and through the impact of changes to policy. The estimated size of each is illustrated below.

The direct economic impact will include a large cut in consumption, especially in the entertainment, transportation, tourism & hotel and retail sectors. There will be fewer opportunities to spend, because of the constraints on the movement of people and weaker consumer confidence. Investment will also be lower, because of reduced cash-flows in private businesses, caused by lower demand and supply chain disruptions. The direct impact is expected to lower annual GDP growth in 2020 by ~0.7 percentage points.

Increased uncertainty also weighs on GDP through indirect channels, as households and businesses pause before spending. This impact is expected to be small, at this stage.

In response to the downturn, we expect additional fiscal and monetary easing to be announced in H1, which will boost the economy by 0.4 percentage points from Q2 onwards. However, the stimulus is likely to disappoint the market. We expect the People’s Bank of China to lower the main policy rate by 30 bps in 2020, and introduce a fiscal stimulus worth another RMB 200bn, through government spending and tax cuts. We expect the additional fiscal stimulus to be financed through a special bond issue of RMB 50bn and a larger quota for local government special bonds, which we now expect to be RMB 3.1trn, or RMB150bn more than previously thought.

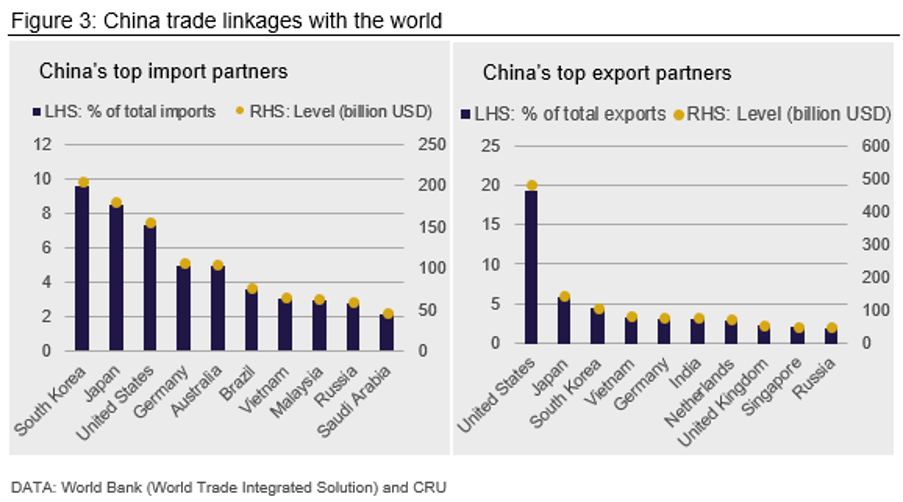

When China Sneezes the Rest of the World Catches a Cold

As noted in previous analysis, disruptions in China will affect the global economy through trade, financial and uncertainty linkages. The trade effect has two dimensions: a demand effect, through China’s imports, and a supply effect, through China’s exports. The charts below illustrate China’s top import and export partners and identify the economies that will be directly affected by the disruptions in China.

The charts above are useful, but they give only a partial picture of the potential impact of Covid-19 on China’s trading partners. The full picture will emerge when we can assess (a) the importance of trade with China relative to other economies (b) the type of goods traded, which may be final consumer goods, such as toys or clothing, or intermediate products such as components that are embedded in final goods, and (c) the ease with which trade with China can be replaced, either domestically or through trade with other countries. China is at the center of global value chains and the East Asian regional production networks. Indeed, according to World Bank Trade Statistics, 66 percent of Chinese exports in 2018 consisted of intermediate and capital goods, up from 48 percent 15 years ago.

Asian economies will suffer most because of their proximity and economic ties to China.

China imports raw materials from the ASEAN region, and parts and components from advanced neighboring economies such as Japan and Korea, to produce final goods for the rest of the world. The intra-Asian trade relationships are complex and often involve several stages of re-imports and re-exports. China has moved up the production value chain, and now supplies many critical high-tech components to advanced economies. The closures at Hyundai Motor in South Korea and Nissan in Japan, and disruptions to Samsung’s factories in Vietnam and to companies such as Apple, Adidas and Mastercard, are examples of the spreading effect of the coronavirus. Furthermore, China is the largest source of foreign tourists to most countries in the region. Travel restrictions will certainly hurt Asian economies severely, especially Thailand, Cambodia and the Philippines, where the contributions of tourism to GDP are more than 20 percent.

Eurozone Likely to be the Second Most Heavily Impacted Region

The Eurozone is an open economy, dependent on manufacturing and trade. In 2018, Eurozone exports accounted for 28 percent of the region’s GDP. China and Asia are prominent destinations for Eurozone goods accounting for 8 percent and 24 percent, respectively, of the bloc’s total exports of goods. Slower growth in Asia will affect the economy of the Eurozone. We have therefore reduced our forecast of Eurozone GDP growth by 0.2 percentage points in 2020, largely because of Covid-19. However, we expect the impact to be short-lived, and to be followed by a recovery starting in Q2.

USA Should be Less Affected than Asia and Europe

The USA is a more closed economy, where exports account for only 13 percent of GDP. We expect the coronavirus outbreak to reduce U.S. GDP by 0.15 percentage points in 2020. Much of this fall should arise through the trade channel as a result of greatly reduced Chinese tourism in the USA. We also expect a lower volume of imported goods to result from supply chain disruptions in China.

Implications for Commodity Markets

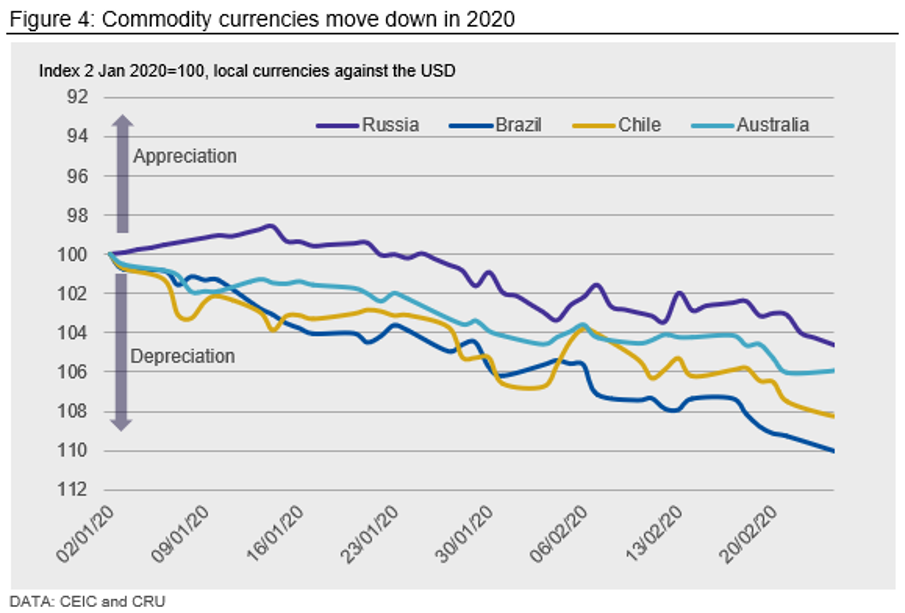

Changes to our global outlook will have important implications for commodity markets. Currencies of major commodity producers have fallen by 4-10 percent in 2020 against the U.S. dollar in response to lower Chinese demand for commodities. This includes lower demand for iron ore from Australia and Brazil, and a fall in demand for copper from Chile. Demand for freight that carries bulk commodities has also plummeted. For example, the Baltic Dry Index fell to 517 on Feb. 26, a level last seen in 2016.

China is the world’s second largest consumer of crude oil. Lower manufacturing activity and reduced consumption and travel in China have led to a significant drop in the demand for refined oil products and thus for crude oil imports, including oil imports from Russia. The consensus from the main oil agencies is that annual demand will fall to less than 1Mbbl/d, similar to demand in 2019 (0.8Mbb/d). OPEC+ will meet in early March. We expect the organization to cut production further in order to support the oil price.

Moving Targets

Covid-19 is a moving target. A few days ago, it felt as though the pace of the virus’ spread was slowing. But things have taken a turn for the worse, as virus cases outside China climb. The spread outside China indicates that economies in the rest of the world may weaken further in coming months, independently of their links to China. Fear is running high. Where things go next is unclear, but we do know that isolation has been effective in containing the virus. City lockdowns and school shutdowns will no longer be a scene only viewed from Wuhan.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com