Product

September 3, 2020

Hot Rolled Futures "Go Vertical"

Written by David Feldstein

Editor’s note: SMU Contributor David Feldstein is president of Rock Trading Advisors. David has over 20 years of financial market trading experience and has been active in the ferrous futures space for eight years. David earned an MBA from the University of Chicago Booth School of Business with concentrations in economics, statistics and analytical finance.

“This is crazy!!!” No, my friend, this is hot rolled.

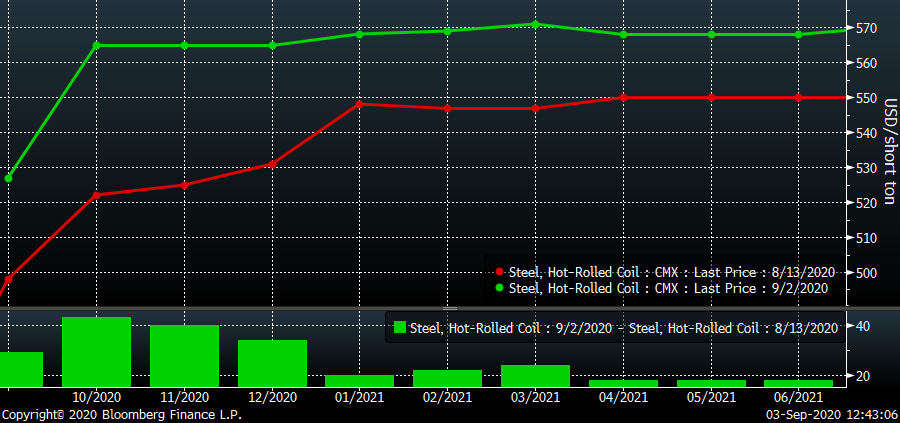

Midwest hot rolled futures have gone vertical over the past six trading sessions and have broken above the down trendline with authority. This chart shows the rolling 2nd month CME Midwest HRC future. What “rolling 2nd month” means is it captures only the trading of the 2nd month future while it is the 2nd month future. On 8/25, the August HRC future expired resulting in the September future shifting from the 2nd month to the front month and the October future now becoming the rolling 2nd month future. The jump from $505 to $526 on 8/26 was due to the “roll” (see inset lower LH corner). The first $21 of the vertical move was due to the October future that had been trading roughly $20/t above September becoming the 2nd month future.

The move from $526 to trading as high as $575 is due to a confluence of events including a strike at NLMK PA, disruptions at Big River Steel, strong August order intake pushing out mill lead times, upcoming planned mill maintenance outages and, most importantly, new actions by President Trump cutting Brazil’s Q4 slab quota by 290k tons. Rumors circulated in steel after the administration slapped 10 percent tariffs on Canadian aluminum imports. Friday’s cut to Brazil’s quota has acted as a major catalyst behind the gains in steel by imposing a government policy risk premium into the cost of flat rolled as we barrel toward the election.

Rolling 2nd Month CME Midwest HRC Futures $/st

Below is the HRC futures curve. In case you were wondering, it is called the “roll” because over time, the future rolls down (from right to left) the upward sloping (contango) futures curve toward spot. Since my last article on Aug. 13, October and November futures have rallied over $40/st. The curve has almost lost its contango and is close to being flat. If the front months continue to rally, the curve could shift into backwardation (downward sloping). One could interpret this to mean that the market isn’t willing to pay much more than $575 in future months. With a glut of supply still offline and Big River bringing up their new mill in November, one can make a strong case for why the current rally could be short-lived. With steel demand badly wounded by the pandemic, pay close attention to buyers’ willingness to pay spot prices above $540. Or will these higher asking prices result in weak order entry in the coming weeks deteriorating lead times? Regardless, the industry is in contract season, so both buyers and sellers have their mutual incentives to drive the spot price in the direction that favors them most.

Rolling 2nd Month CME Midwest HRC Futures Curve $/st

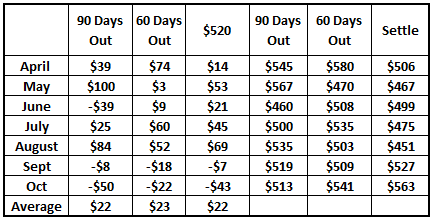

Hedging downside price risk in CME HR futures has been a winning strategy during the pandemic. In my last article, I showed that regardless of implementing a strategy of selling at $520, 90 days or 60 days prior to settlement, it would have rewarded the seller with an average of $40/st per month. September and October are both within the 90-day window, so I’ve added them to the table. Based on last night’s settlements, the current positions are showing an unrealized loss bringing down the average to April to $22/st per month if prices settled here.

For service centers that implement hedging into their overall business strategy, the hedging gains/cashflow have been of significant value. While it is frustrating to see some of those gains reversed, most companies only hedge a percentage of their inventory. This rally is a welcome development for all of those in the service center industry, a sector that has endured two long years of falling flat rolled prices only to be compounded by decreased volumes since April. For those out there who believe hedging is “just gambling,” I hope this information helps dispel that as it is the complete opposite of gambling. Hedging diminishes price risk exposure. Considering the historically intense volatility in the Midwest hot rolled price, it has not been surprising to see growth in the number of new participants in the CME HRC futures market.

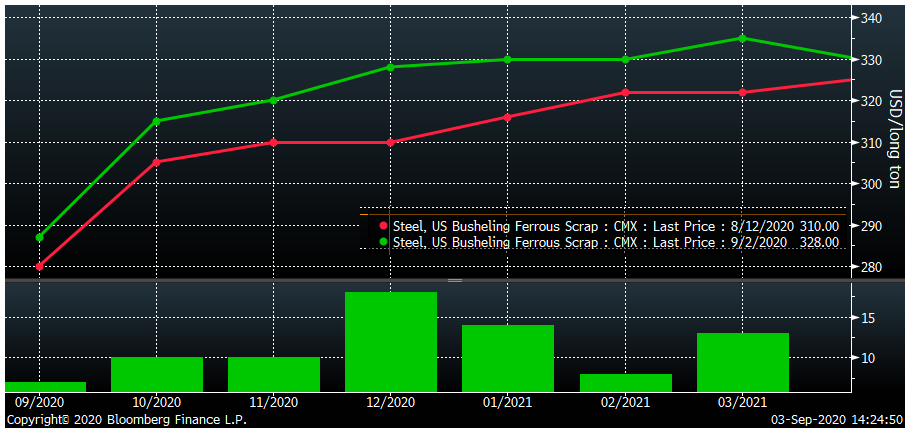

Below are CME busheling and LME Turkish scrap futures. The sharp move higher in the green circle was the “roll” that took place on Aug. 11 (when the August future settled). Busheling has only gained $10 in October and November despite hot rolled rallying $40+ in those same periods. Turkish scrap continues to bounce between $280 and $287.

Rolling 2nd Month CME Busheling Future (white) & LME Turkish Scrap Future (red)

The CME busheling futures curve remains upward sloping with the most obvious driver of higher future scrap prices being Big River’s new EAF coming online in November needing to build up its scrap inventory ahead of its start.

CME Busheling Futures Curve $/lt

Subtracting the CME busheling future’s settlement from the CME HRC future’s settlement gives a rough way to evaluate EAF profitability. Profitability plummeted during the pandemic, but has moved back above its historic floor. The green line and red dots show the future implied levels of the spread moving higher to $240-$250/t through year end.

CME Midwest HRC – CME Busheling Futures

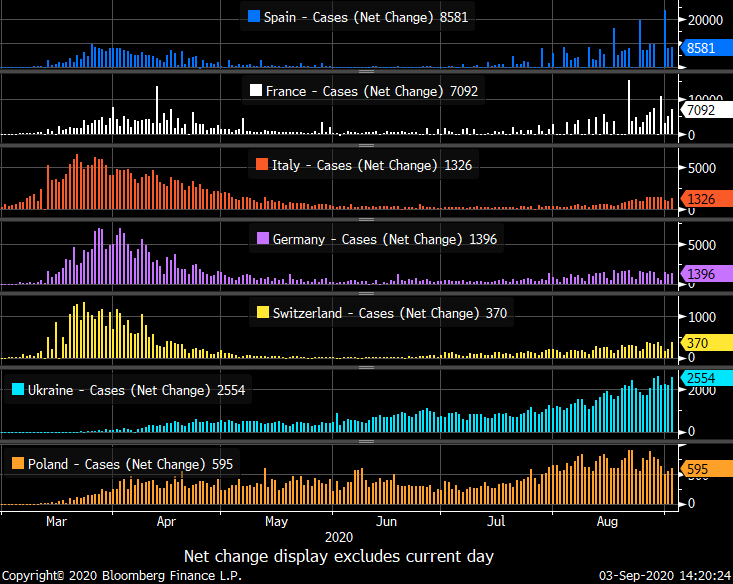

While Midwest HR has rallied sharply and that rally is being driven mostly by steel industry specific forces, there are concerning developments in global financial markets I am watching closely. Europe is struggling with a second wave of COVID infections as shown in the chart of new daily cases below.

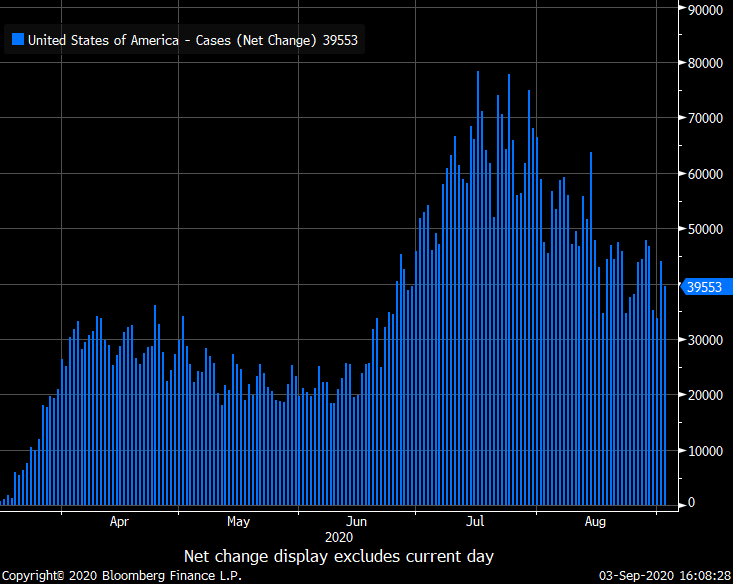

While new cases in the United States have been trending down since peaking in July.

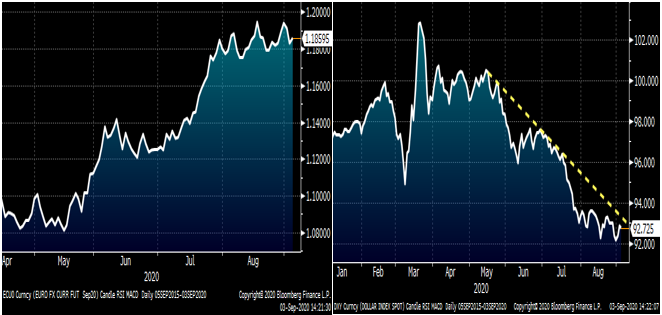

The euro rallied sharply vs. the U.S. dollar in July. The dollar weakness helped boost rallies in commodities such as oil, iron ore, zinc, aluminum, copper, etc. The rally in the euro occurred as the U.S. suffered through the spike in COVID cases. Now that new COVID cases are falling in the U.S. and rising in Europe, will the dollar rally? Another factor favoring the U.S. dollar is that export driven European countries, especially Germany, want the euro to lower and will likely support it.

Euro/U.S. Dollar Spot (left) & U.S. Dollar Index (right)

While the dollar has shown signs of reversing its downtrend, there has been a move lower in crude oil. Wednesday’s sell-off got real when it was announced that the DOE U.S. Crude Oil Inventories fell by almost 10 million barrels, almost five times expectations, leading to a sharp short rally that quickly failed as shown in the yellow oval in the inset in the chart below.

Rolling Front Month WTI Crude Oil Future $/bbl

The selling continued in oil today bleeding into the commodity complex with iron ore and Chinese steel prices falling.

Rolling 2nd Month SGX Iron Ore Future $/mt

Also, the Nasdaq fell almost 5 percent while the S&P 500 fell 3.3 percent today. Is this the beginning of a risk-off profit taking after gluttonous rallies in risk assets? If it is, would a rallying dollar and falling commodity complex snuff out the nascent rally in hot rolled? Tune in next time.

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Mr. Feldstein should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.