Market Data

September 20, 2020

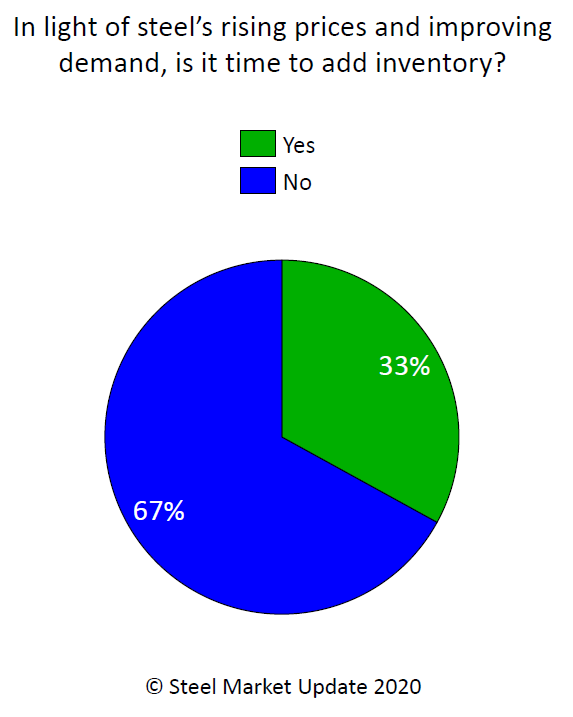

SMU Market Trends: Is It Time to Add Inventory? Buyers Disagree

Written by Tim Triplett

Service centers and and other buyers traditionally jump into the market to buy ahead of rising steel prices. Steel prices are clearly on the rise, but only about one-third (33 percent) of buyers responding to Steel Market Update’s questionnaire this week said they feel it’s time to add inventory.

Their comments reveal some disagreement about the staying power of the higher prices. Do they reflect improving demand or a temporary tightness of supply?

Here are some of their thoughts:

“Buy only what you need. Excess buying extends lead times and runs up prices.”

“There’s risk in getting caught with high-priced inventory when prices come down.”

“There’s too much uncertainty as to whether this bump in demand is only temporary.”

“We’re adding inventory, but only slightly, as fourth quarter tends to utilize less.”

“We’re buying, mainly because the supply is getting tight.”

“Not buying. If demand falters, we do not want excess inventory getting devalued month after month.”

“We are ordering sooner and also ordering to a longer horizon.”

“Mill capacity utilization is still in the low 60s, energy demand is flat, demand will not sustain an extended run-up in pricing.”

“The situation is unstable. Possible second COVID wave. Not sure about adding inventory.”

“It’s time to stabilize inventory at current levels.”

“Buy just what you need. No blanket orders.”

“The shortages are short-term.”

“Domestic lead times are moving out. HRC is now 4-8 weeks. Import lead times are for December/January or later arrivals. Just getting products, let alone build inventory, will be a challenge.”

“Steel prices will not maintain the increase.”

“The upswing will last a couple of months and then recede.”

“We are buying what we need, nothing more, nothing less.”

“Demand is exceeding forecast and lead times have moved out. Our inventories are lower than planned at this time.”

“We feel this rise in price will only be temporary. We have enough on order and in stock to ride this out.”

“We bought quite heavily over the last three months as pricing was descending. We are good through Q1 unless our business gets crazy busy.”

“Prices at $600 are no longer a good value. Buy what you need, nothing more. Otherwise we go back down in a hurry.”

“This is a short-term situation, not triggered by demand but by mill outages to artificially tighten supply. Our inventories are fine. The only product that is really tight for the short term is Galvalume, and that will subside by early November.”

“It appears that most inventories were already depleted. Due to extending lead times and strong foreign pricing, I fear if we don’t get inventory to normal levels now we will have some outages.”

“We think it’s short-term.”

“Running on fumes headed into the winter months on inventory levels is probably not advisable as several factors could cause shortages and outages and nobody likes that situation.

“The mills are determined to get to $30/cwt HR. They are almost there and demand is very strong. If you didn’t buy significant inventory at the bottom, you are in for a rough ride as prices will continue to climb.”

“Buy only what you need. Trying to time the market leads to inventory hangovers. Plus, good luck trying to get anything additional from the mills right now.”

“You add inventory when the cost to carry inventory today more than offsets the higher price tomorrow. Then, after everyone does the same thing, the price crashes…..again!”

“Service center inventories are low. Hopefully everyone has inventory inbound, with July pricing.”

“Restock before prices go any higher!”

“No, it only exacerbates misleading demand.”

“My rule is 6-8 weeks of inventory. It has worked well for 26 years. No need to change now.”