Analysis

November 16, 2020

Final Thoughts

Written by John Packard

The Perfect Storm:

Long lead times, late deliveries, low service center inventories, strong demand, higher prices, lack of foreign steel imports, mill outages both planned and unplanned, maximum capacity utilization rates at a number of mills, NLMK USA strike, higher ferrous scrap prices that are expected to go much higher in the coming months, restrictions on Brazilian slabs…. The net result is business is tight, buyers are concerned about buying steel over the next few months, and the expectation is for prices to continue rising.

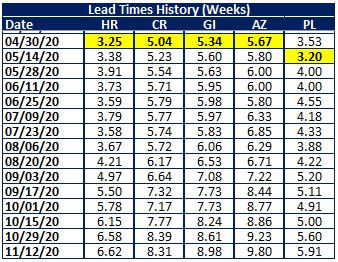

Lets talk about lead times for a moment. Below I have provided lead times for hot rolled, cold rolled, galvanized, Galvalume and plate steels since the end of April. The areas highlighted in yellow indicate the shortest lead times we published for this calendar year. Our lead times come from our flat rolled and plate steel market trends surveys, which are conducted every other week.

The lead times produced from last week’s survey are some of the longest we have seen since our survey began measuring lead times back in 2011. Hot rolled is at a record high at 6.62 weeks. The previous high for HRC was 5.73 weeks in April 2018. Cold rolled is at a record high at 8.31 weeks compared to the past record high of 8.19 weeks published in May 2018. In May 2016, Galvalume lead times were averaging 8.44 weeks. Now AZ is 9.80 weeks. The only item that is not setting a record on lead times is plate, which at 5.91 weeks is still a long way away from the 7.89 weeks reported in May 2018.

I would have to go back to my days representing Winner Steel around 2004 (NLMK Sharon Coatings is the mill’s name today) to find a time when lead times exceeded what we are reporting from our survey.

Just because our survey says the average lead time on hot rolled is more than six and a half weeks does not mean spot steel can or cannot be purchased sooner (or much later) than during that time frame. I spoke with one mill this morning who has not opened January production and will not open for another three weeks. They know they have limited spot that will be available when they open, and they will cover their steady spot customers first. I assume other mills are taking similar postures.

![]() I did hear ArcelorMittal plants are having significant production issues. One large service center told me part of their issue was related to a blast furnace being down at Cleveland Works and the mill having to bring slabs in from other plants.

I did hear ArcelorMittal plants are having significant production issues. One large service center told me part of their issue was related to a blast furnace being down at Cleveland Works and the mill having to bring slabs in from other plants.

When I asked the president of another service center if ArcelorMittal was having some production issues, I was told, “I can confirm they are over their heads…and seem to be screwing over even their best customers.” He added, “They have been hinting that [having no spot or limiting tonnage for first-quarter 2021] for awhile [regarding] shorting or excluding tons even from contracts.”

SMU canvassed a large group of flat rolled and plate steel buyers today and asked them if they were having any issues getting steel, and how the mills were doing on deliveries. We only heard from a few companies who disclosed they were having issues procuring enough material. Just about everyone related stories about the domestic mills being anywhere from two weeks to more than a month late on orders that are due (or past due).

When asked if their company was having any issues either buying steel or getting it delivered on time, this is a sampling of what we heard:

“Having some delays on mill shipments. We are in decent shape, but know of many others that are flat out of coil on some key sizes.” Service center

“For our ongoing spot, we have January needs that I’m 80% sure we’ll be okay with, once mills open. So, if there’s little to no spot available for January, then there’s a possibility of a problem. Lateness is an additional issue, and once again we’re OK for now, but if we see additional lateness (> 1 month late) then that too could be problematic.” Service center

“Every mill we deal with is shipping at least 10-20 days late. Every mill.” Service center

“Both answers are yes [having issues getting steel and mills are delivering late]. We are very busy, breaking all-time weekly and monthly sales records, and need more steel than planned. Extensive lead times are becoming a large issue for us, as well as steel mills running 2-3 weeks behind. To make matters worse, the steel mills are not communicating to us their lead time issues; it’s a one-way conversation, which is getting very frustrating. In a computer-driven world, it should be easy to change lead times for orders online so we can plan. They must be in the stone ages still.” Manufacturing company

“Steel is tight. Anything slightly out of the ordinary is tough to find. Plate lead times have moved into January.” Service center

We got a note from Ohio Steel Sheet and Plate that said, “I’m actually typing a letter to my 300 steel customers that Ohio Steel Sheet and Plate Inc. will be announcing an allocation for plate in December of 2020. You can publish that exact statement.” Eric Rebhan of Ohio Steel Sheet and Plate

Speaking of plate, Nucor provided some price guidance to the industry today in their price increase announcement. Instead of saying prices were going up by “X” dollars per ton, they provided specific “minimum base prices” for a wide variety of plate produced by the mill (see article on announcement in tonight’s newsletter).

I participated in a HARDI galvanized steel conference call today. The companies sharing information about their businesses relayed strong business conditions, balanced inventories, higher prices and concern about what the future has to hold.

I am hearing concerns about the uptick in COVID-19 cases across the United States and what this new wave of infections will mean for business when we get into 2021. All I can say is, wear your masks and be very careful over the Thanksgiving Holidays here in the States.

Registration is open for a couple SMU Events:

![]() Steel 101: Introduction to Steel Making & Market Fundamentals – I spoke with one of the mills this morning who told me that even though our workshop has gone virtual due to the pandemic, their company sees a tremendous amount of benefit in sending their new employees. The Dec. 8-9 workshop coming up will be especially interesting just due to the market conditions that exist today. I will be one of the instructors and will focus on some of the key fundamental issues driving steel prices, production, demand, etc. Our two metallurgists, Roger Walburn and Chuck McDaniels, will provide insights into the steelmaking and rolling processes from both EAF and blast furnace/BOF perspectives. Mario Briccetti will discuss prepaint, contract pricing, using an index and a number of other topics from a purchasing perspective. Our last Steel 101 workshop was virtual and was very well received by all 33 of our attendees. You can learn more and register by clicking here.

Steel 101: Introduction to Steel Making & Market Fundamentals – I spoke with one of the mills this morning who told me that even though our workshop has gone virtual due to the pandemic, their company sees a tremendous amount of benefit in sending their new employees. The Dec. 8-9 workshop coming up will be especially interesting just due to the market conditions that exist today. I will be one of the instructors and will focus on some of the key fundamental issues driving steel prices, production, demand, etc. Our two metallurgists, Roger Walburn and Chuck McDaniels, will provide insights into the steelmaking and rolling processes from both EAF and blast furnace/BOF perspectives. Mario Briccetti will discuss prepaint, contract pricing, using an index and a number of other topics from a purchasing perspective. Our last Steel 101 workshop was virtual and was very well received by all 33 of our attendees. You can learn more and register by clicking here.

Tampa Steel Conference: On Feb. 2, Steel Market Update along with our host Port Tampa Bay will conduct the 32nd Tampa Steel Conference. This year the event will be virtual and the timing could not be better for those of you interested in understanding the economy, impact of the Biden administration, trade issues, logistics issues and the steel industry in general. We are working on a one-full-day agenda, which will feature experts on each of these topics. We have intentionally priced this virtual conference so companies can send as many people as possible. The single person rate is $150; however those of you who have participated in a past Tampa Steel Conference can get a 50 percent discount ($75 per person) if you register by Dec. 31, 2020. SMU and CRU member companies get a $25 discount and there is an additional $25 discount for those companies who register more than one person. For more details and registration click here.

As always, your business is truly appreciated by all of us here at Steel Market Update.

John Packard, President & CEO