Prices

February 13, 2021

Import Share of Steel Market Moves Up in December

Written by David Schollaert

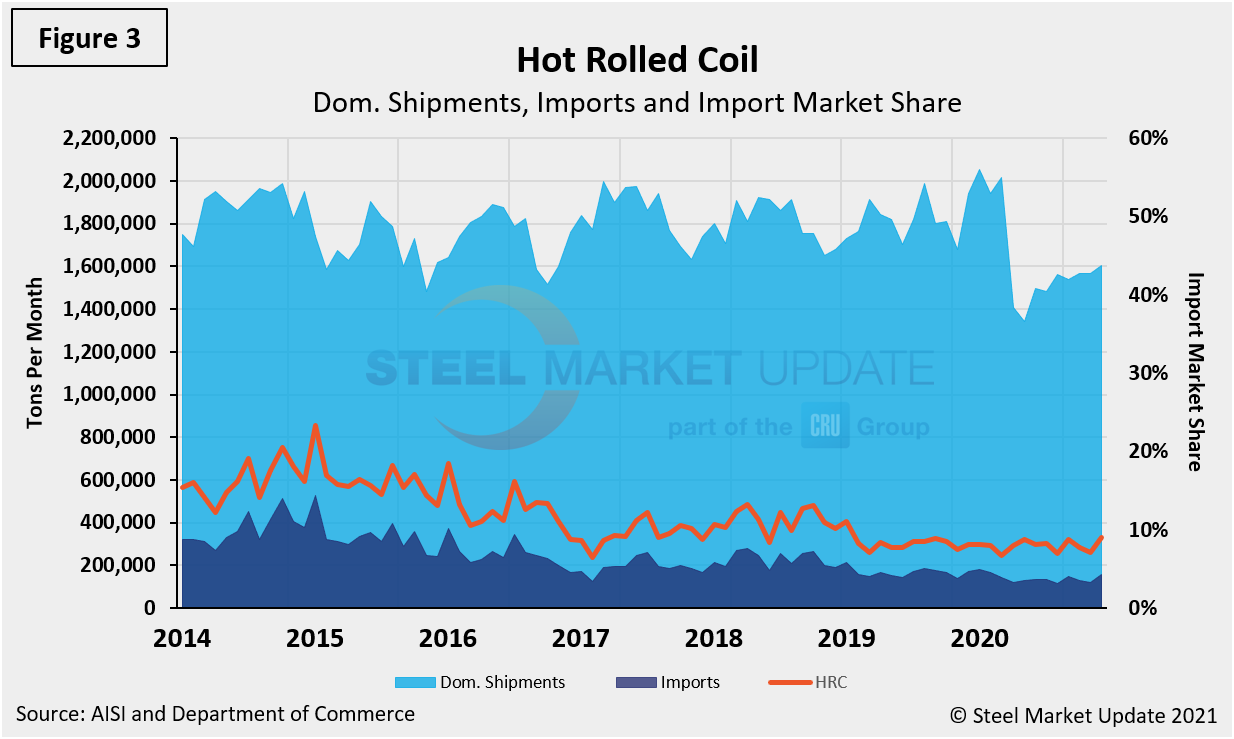

This report examines the import share of sheet, plate, long and tubular products. As of December 2020, imports’ share of total sheet products was 12.3%, up from 11.4% in November. The increase, albeit marginal, is notable as it’s the first increase for imports after declining for seven consecutive months following the most recent peak of 16.6% in May 2020. The import share of hot rolled coil has been below 10% since January 2019; however, it was also up to 9.0% in December, compared to 7.1% the month prior.

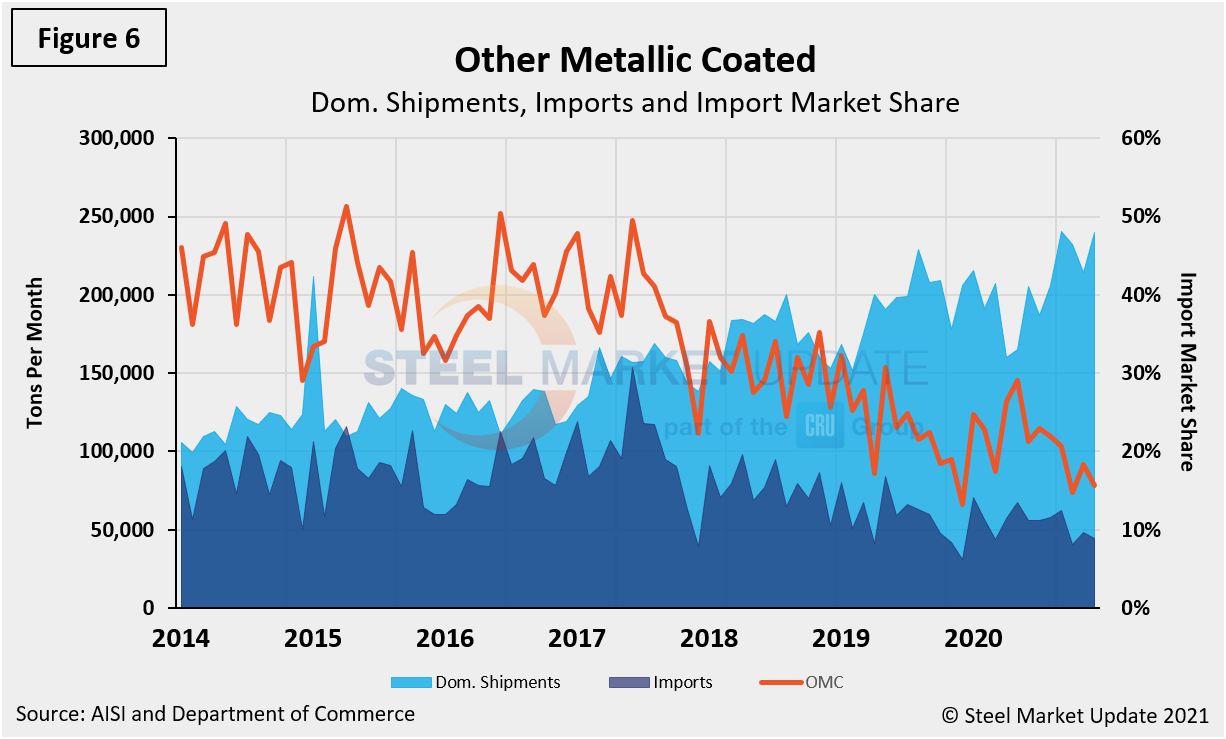

Other metallic coated sheet remains the product with the most drastic shift in import market share over the past several years, retracting from its most recent peak of 51.3% in April 2015 to 15.6% in December, and down from 18.3% month on month. This sharp swing is a result of the concurrent decrease in imports and an increase in domestic shipments since 2014.

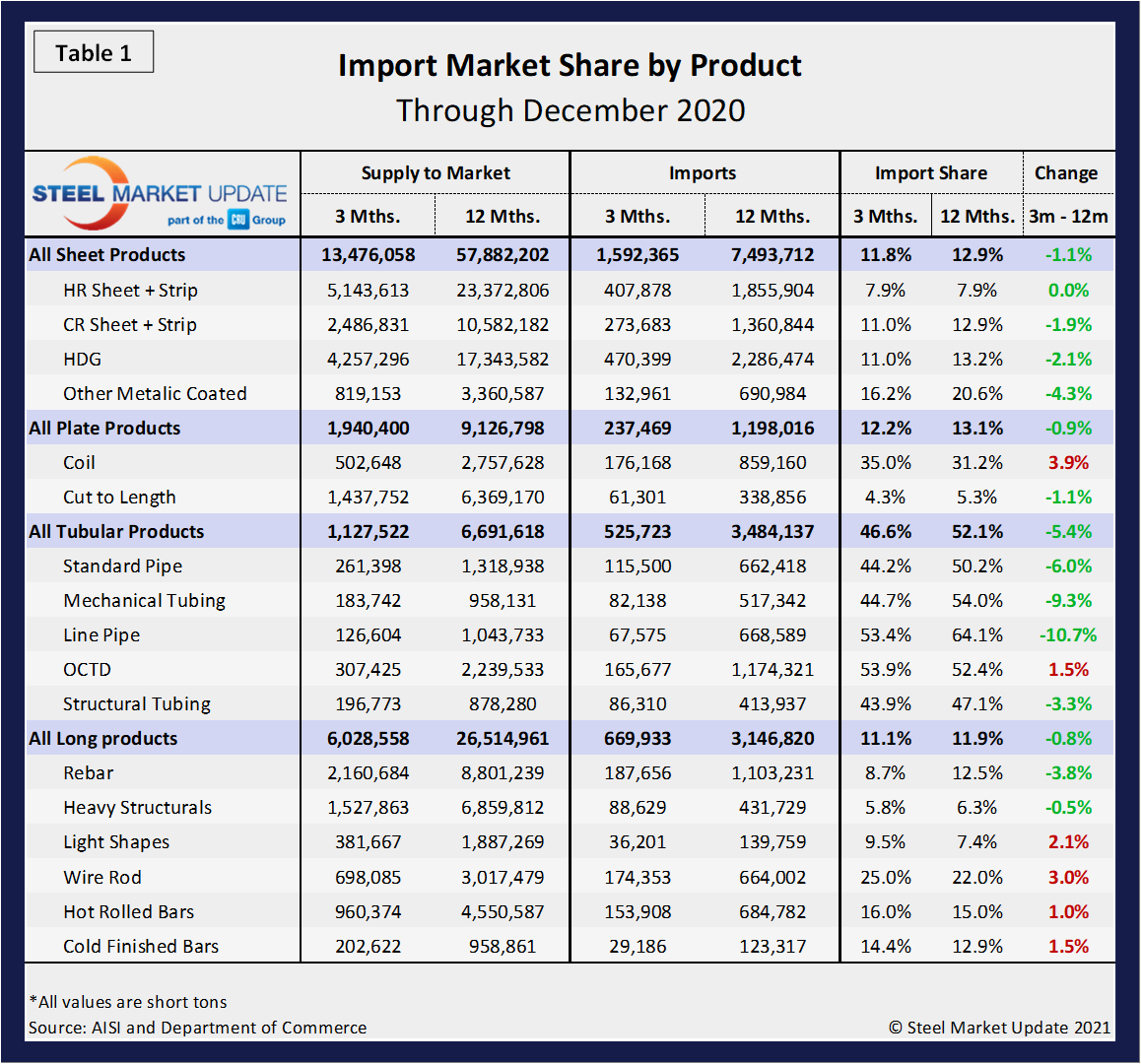

Table 1 shows total supply to the market in three months and 12 months through December 2020 for the four product groups and 17 subcategories. Supply to the market is the total of domestic mill shipments plus imports. It shows imports on the same three- and 12-month basis and then calculates import market share for the two time periods for 17 products. Finally, it subtracts the 12-month share from the three-month share and color codes the result green or red according to gains or losses. If the result of the subtraction is positive, it means that import share is increasing, and the code is red. The big picture is that import market share has decreased in three months compared to 12 months across all four product groups (sheet, plate, tubular and long), and 11 out of the 17 subcategories. Most notable of the seven subcategories that have experienced declining import market share are coil (3.9%), wire rod (3.0%) and light shapes (2.1%) in three months compared to 12 months through December 2020.

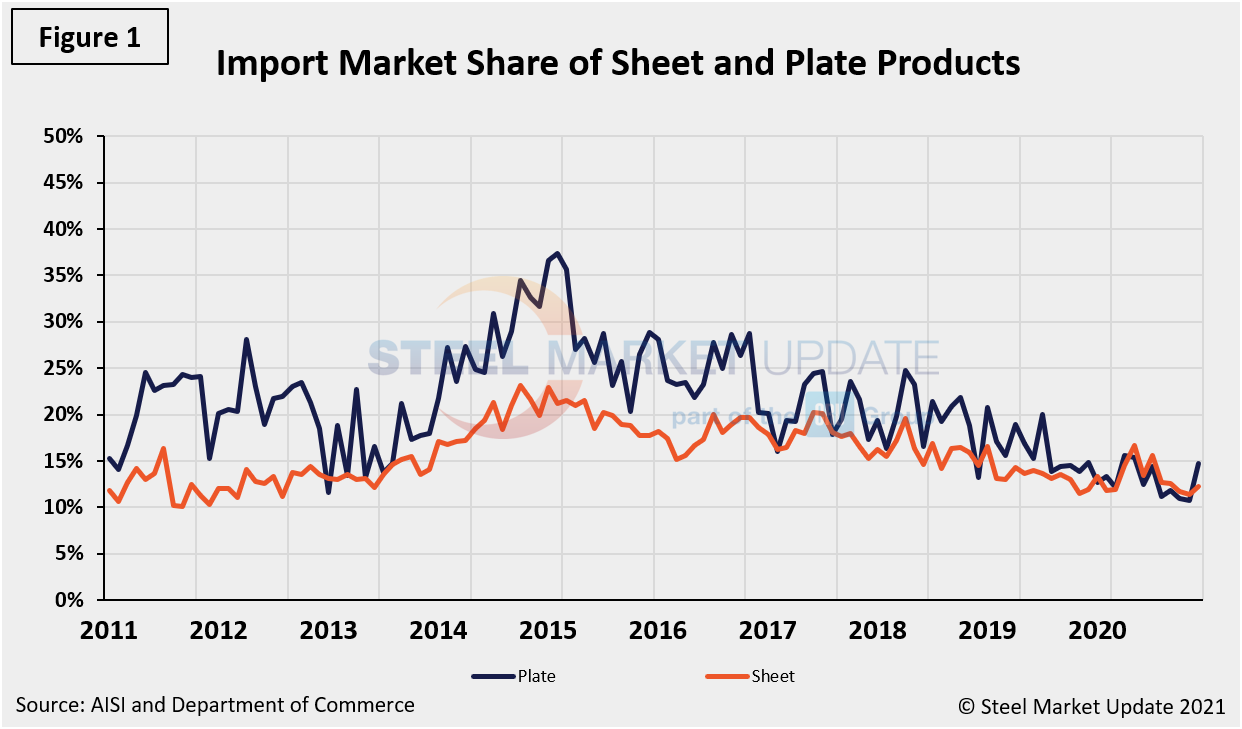

Figure 1 shows the historical import market share of plate and total sheet products. The import share of plate has been decreasing erratically since February 2015. Sheet product import share has also coasted downward in the same timeframe. That trend reversed in December with the share of plate and sheet product imports posting gains. Current market share of foreign plate as of December 2020 is 14.7%, up markedly from 10.7% in November. Sheet also rose month on month, from 11.4% in November to 12.3% in December.

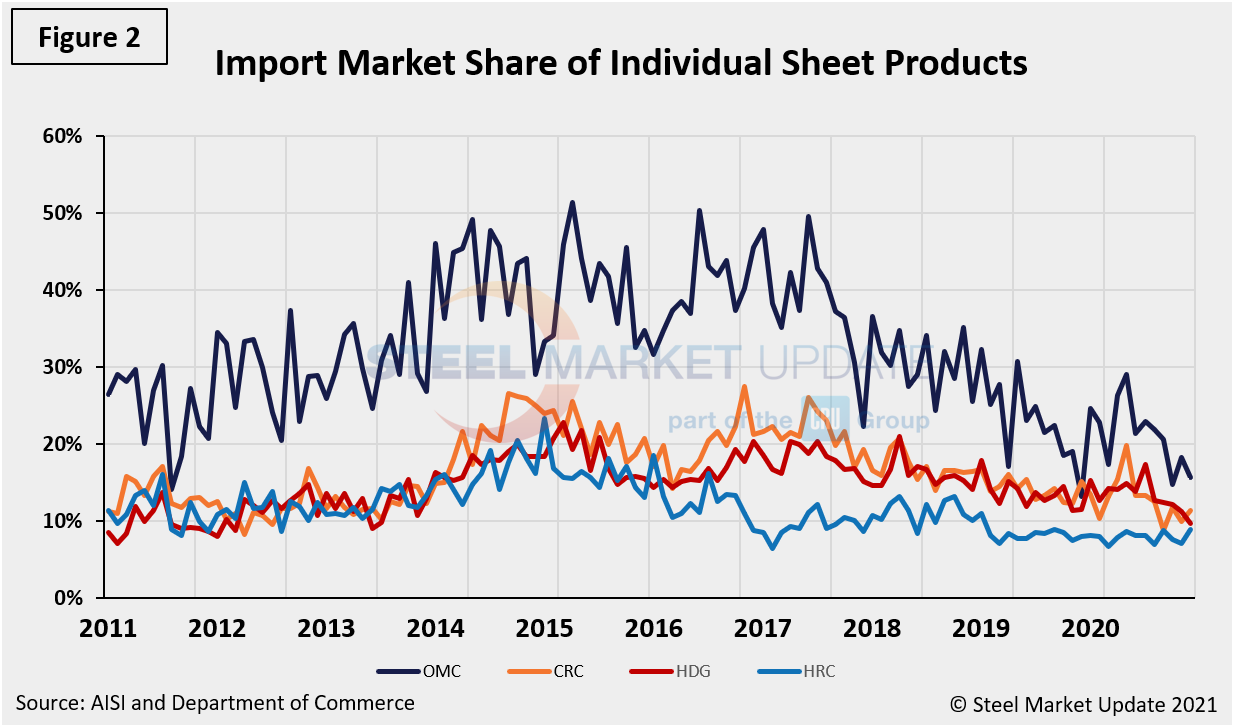

Figure 2 shows the import market share of the four major sheet products. Other metallic coated (mainly Galvalume) has traditionally had by far the highest import market share, but the gap has closed since late 2017. For the last four years, hot rolled coil has had the lowest import market share of the major sheet products, current at 9.0% through December. Although it has the lowest market share, December’s posting is an increase from 7.1% in November, and its highest percentage in nearly two years.

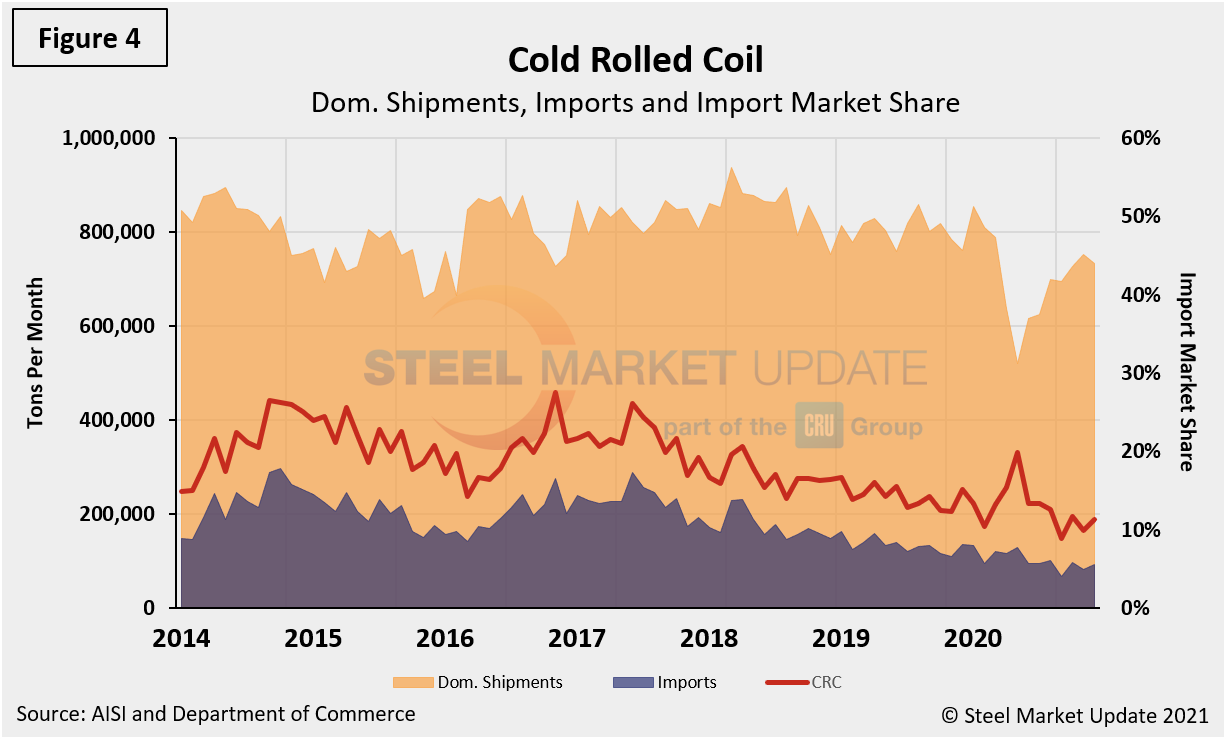

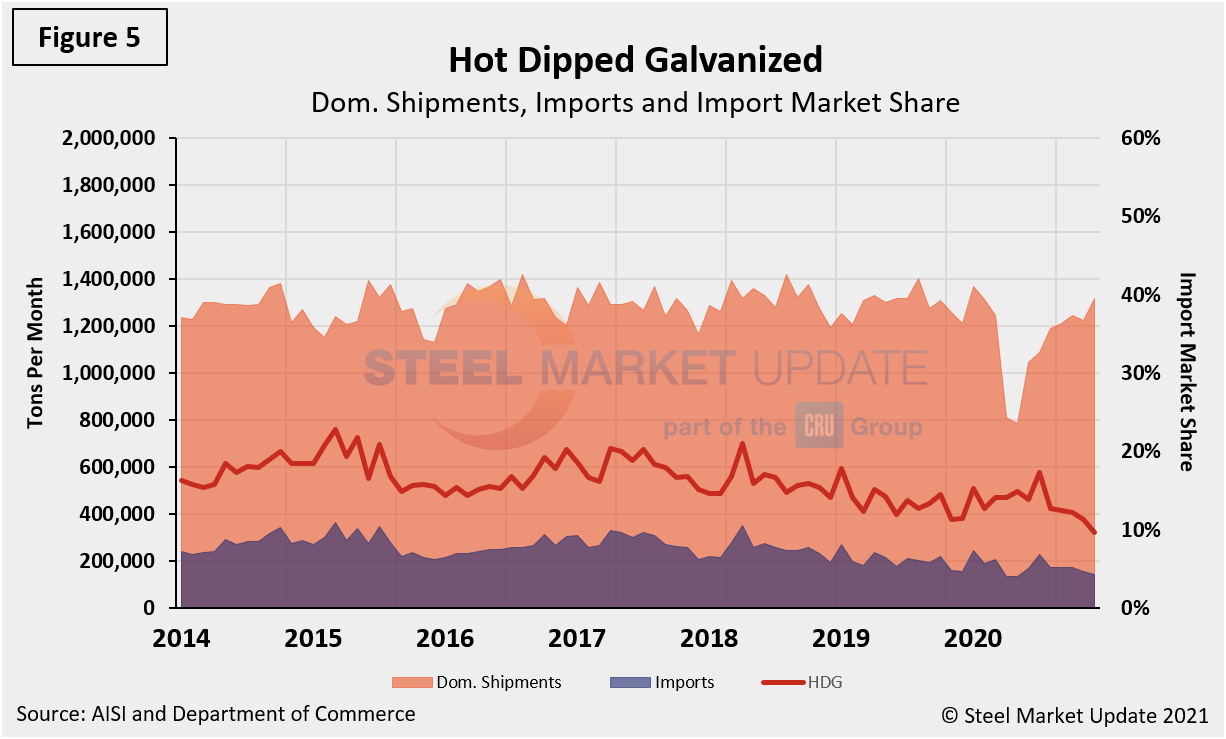

Figures 3 through 6 show the domestic shipments, imports and import market share of the four major sheet sectors. The biggest change has been that domestic shipments of OMC (Figure 6) have more than doubled since 2014 with a corresponding decrease in import market share. The import market share of cold rolled has declined by half since 2017. The import market shares of hot rolled and HDG have drifted down as well over a similar period, but at a less dramatic rate. Both HRC and CRC rose month on month, however, pointing to a potential trend for 2021 as more imports arrive as a result of the record high domestic prices.

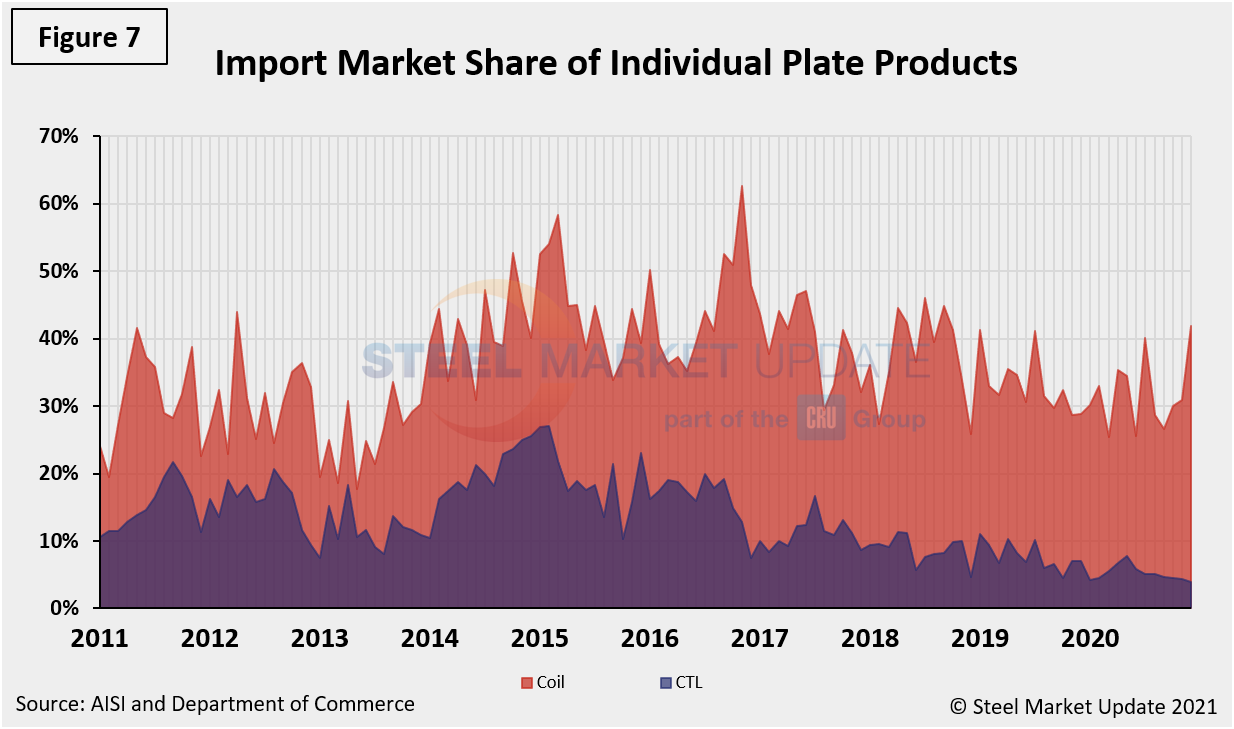

Figure 7 breaks out coiled and discrete plate from the flat rolled total and shows that in 2020 through December coil imports had more than five times the market share of CTL imports, while CTL imports fell from 20.0% in July 2016 to just 3.9% in December, down further from 4.4% the month prior. By comparison, coiled plate imports rose from 26.6% in September to 41.9% in December.

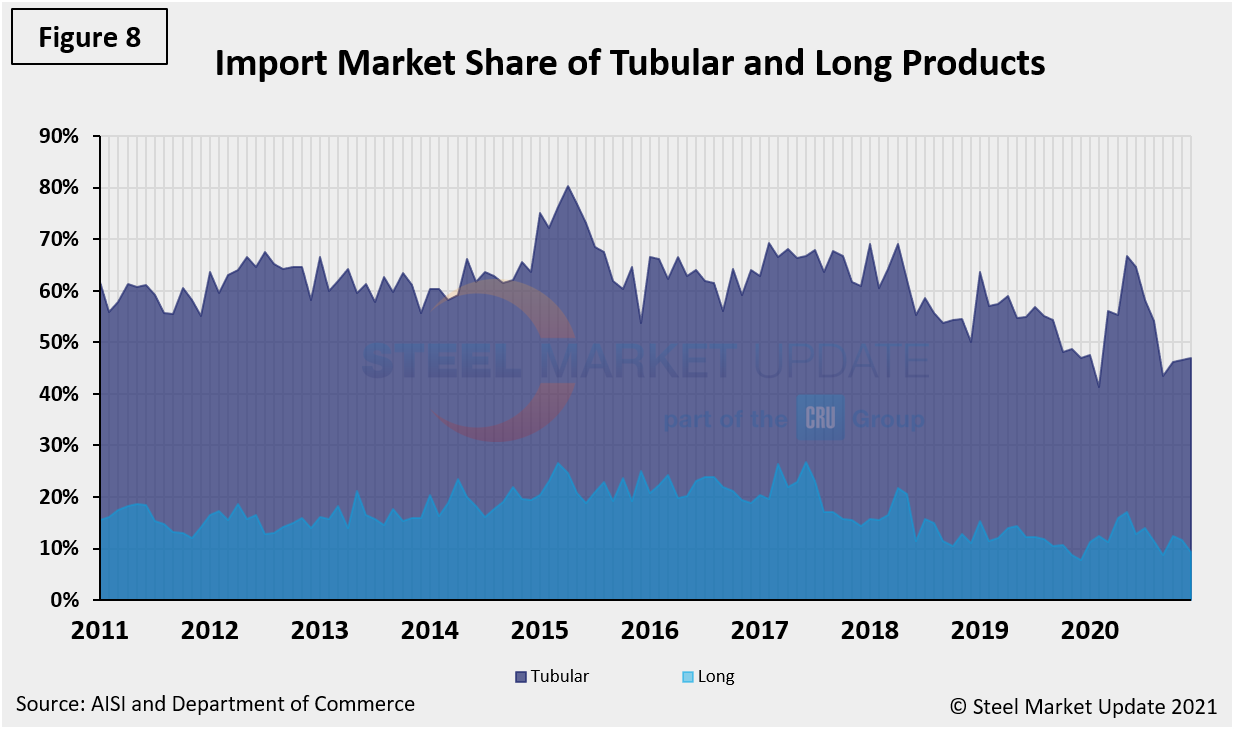

Figure 8 describes the total import share of tubular goods and long products. Both have seen steady decreases since 2015, though long products at a more accentuated rate. Since 2016 alone, the import market share of long products has declined by more than 50%, while tubular goods’ share has decreased by nearly 29% over the same prior. Even though long products have steadily dipped over the past two months, currently at 9.4% down from 12.4% in October, tubular goods increased during the same period from 43.5% in September to 47.0% in December last year.

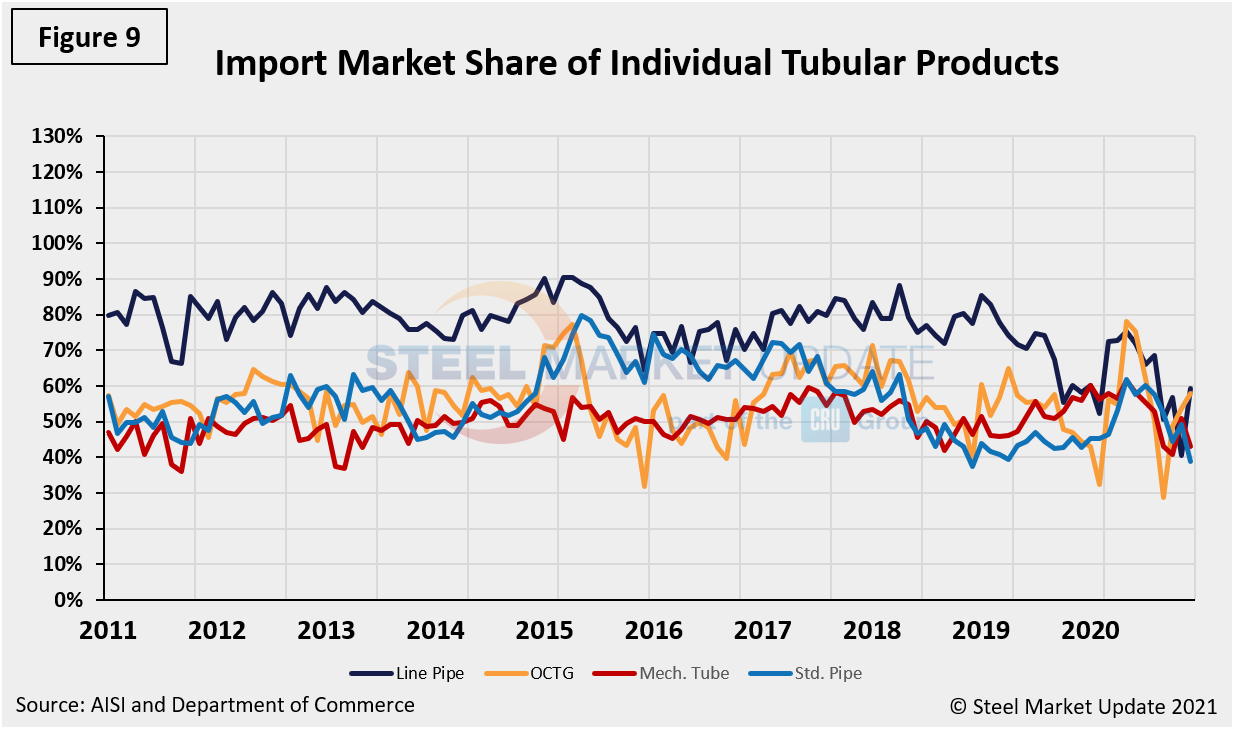

Figure 9 shows the import market share of the individual tubular products. Based on the available information, all are very high compared to other steel product groups. Line pipe is the highest despite some variation in 2020; it was up noticeably month on month, from 40.5% in November to 59.3% in December, but declined dramatically in 2019. OCTG has rebounded, after dropping from 78.2% in May to 28.7% in September, to close out 2020 at 57.8% in December.

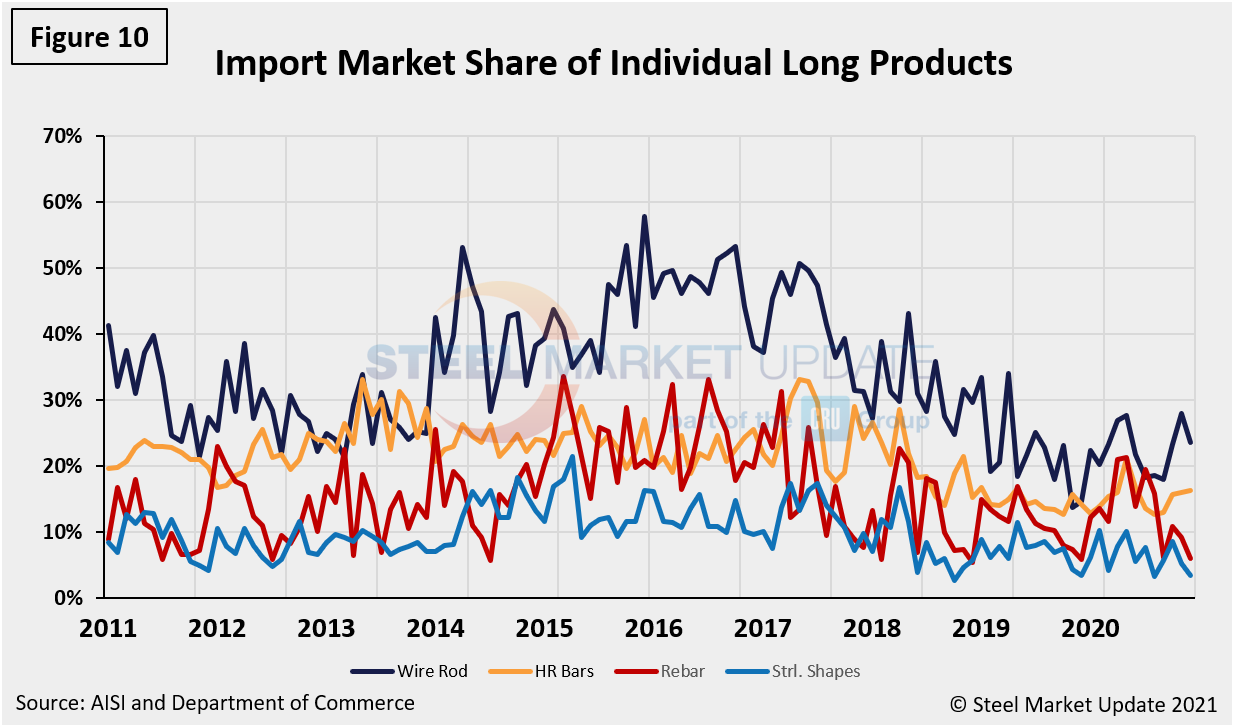

Figure 10 shows the detail for the four major sectors of the long products group since January 2011. The most significant change in this sector was for wire rod, which in the years 2014 through most of 2017 had double the import market share of the other long products. In the second half of 2017, the gap began to narrow to the point that in November 2019 the import share of wire rod fell below that of hot rolled bars. Rebar has been very erratic, but the import share fell to a historically low level in December 2019 before returning to a more normal level in 2020. The sole long product to close out 2020 on an up note was hot rolled bars, seeing repeated increases from 12.7% in August to 16.3% in December.

SMU Comment: Although overall import market share has decreased over three months compared to 12 months through December 2020 across all four product groups (sheet, plate, tubular and long) and most subcategories, this trend could shift as record higher domestic prices attract more imports as 2021 unfolds.

By David Schollaert, David@SteelMarketUpdate.com