Market Data

August 5, 2021

Mill Lead Times/Negotiations: No Significant Change

Written by Tim Triplett

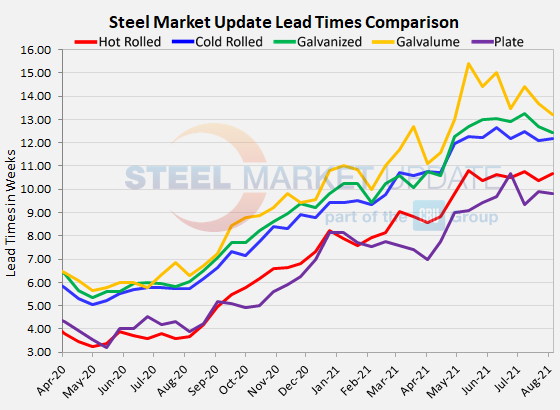

Steel Market Update’s check of the market this week shows no significant change in lead times for deliveries of spot orders from the mills. Average lead times for hot rolled orders remain above 10 weeks, while those for cold rolled and coated products are still above 12 weeks – at least twice as long as normal. SMU is keeping a close eye out for any shortening of lead times, which would signal a change in market conditions that could presage lower steel prices. There are no signs of that yet.

Lead times for hot rolled now average 10.67 weeks, up slightly from 10.36 weeks in the last survey. Cold rolled lead times inched up to 12.17 weeks from 12.11 two weeks ago. At 12.45 weeks, lead times for galvanized products are down slightly from 12.68 weeks earlier this month. Lead times for spot orders of Galvalume have dipped to 13.22 weeks from 13.67. Average plate lead times also saw a small downtick to 9.83 weeks, from 9.90.

Based on three-month moving averages, which smooth out the weekly volatility, flat-rolled lead times remain near historic highs. The 3MMA for hot rolled lead times now averages 10.54 weeks, cold rolled 12.30 weeks, galvanized 12.89 weeks, and Galvalume 14.03 weeks. Plate’s 3MMA has risen to 9.81 weeks.

None of the changes in the most recent data represent more than a day or two difference, up or down. Only when lead times see downswings of a week or more – indicating that the mills are less busy – should prices be expected to follow.

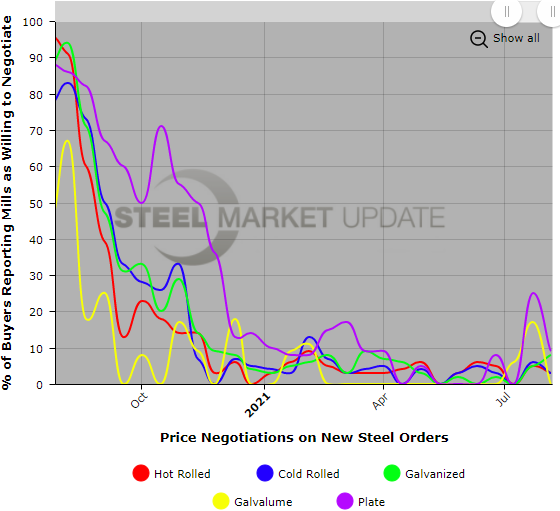

Negotiations

There’s also nothing new to report on steel price negotiations. Nearly all the respondents to this week’s poll confirmed that the mills still have all the leverage when it comes to price. “Still no negotiations of any kind, and very limited tonnages out there at the mill level,” one service center executive said. Mills may eventually be disappointed in their order levels because so many buyers have committed to cheaper imports, noted another.

By Tim Triplett, Tim@SteelMarketUpdate.com