CRU

September 12, 2021

CRU: North American Fundamentals Suggest Prices Will Soon Peak

Written by Josh Spoores

By CRU Principal Analyst Josh Spoores, from CRU’s Steel Sheet Products Monitor

Market fundamentals in the North American sheet market continue to evolve and clearly suggest that supply tightness is easing. From a broad point of view, these fundamentals include rising supply, service center inventories that are balanced with outbound shipments, and demand growth that is rising at a slower rate. Additionally, seasonality will soon affect this overall balance of supply and demand.

Domestic steel production has continued to rebound from the 2020 lows. As production has run at a strong rate over the last three months, it has recently been supported by the successful start-up of Ternium’s hot strip mill in Mexico. In addition to rising domestic production, import arrivals are high and trending higher. Due to the historic spread of domestic prices versus global prices, buyers have dramatically increased import orders with arrival in 2021 Q4 and 2022 Q1. Some have noted that they have placed orders for sheet products as much as $500 /s.ton below current mill offers for arrival in 2021 Q4.

Finally, service center data for sheet products shows that inventories are in balance with outbound shipments, though each of these remain below pre-pandemic levels. However, the amount of material these service centers have on order with mills is 65% higher than normal. This tells us that service centers are relying on existing orders for further inventory building, likely over the seasonally slower winter.

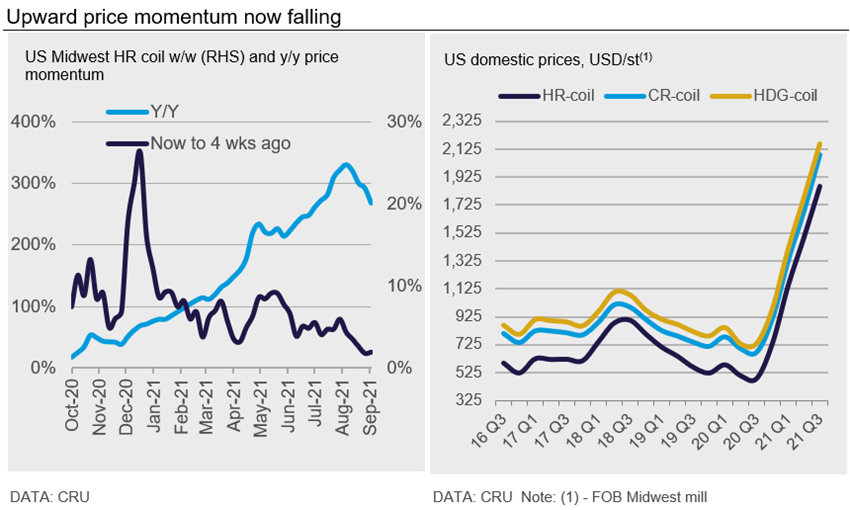

While these supply fundamentals continue to return back towards more normal levels, sheet prices have continued to reflect a market that remains in a supply deficit. Sheet prices have continued to increase, though the upward momentum has clearly slowed (see chart below).

U.S. West Coast steel sheet prices increased 3-6% m/m for products produced in November. Domestic mills continued to tightly control order books amidst strong demand, as buyers forecast a busy fourth quarter without the usual holiday slowdowns. Distributor inventories remain below historic levels, with customers reserving incoming mill tonnage well in advance of its arrival, just to ensure availability.

In Mexico, sheet prices have fallen this month after 12 consecutive months of price hikes. HR coil dropped by around 4% m/m and CR coil by 2% m/m. Meanwhile, Mexican flats production increased by 11% y/y in 2021 H1, according to Alacero, while sheet imports increased sharply by 39% y/y in the period. Supply is expected to increase further, partly due to Ternium’s new rolling mill and with AHMSA operating at a higher utilization rate despite the end of the company’s sale agreement. At the end of August, the deal to sell 55% of AHMSA to Alianza Minero Metalúrgico Internacional after eight months of negotiations has ended with no agreement. AHMSA said no formal proposal was presented to date, and thus, it will look for other partners to buy the share of the company owned by the controversial Alonso Ancira. Local news says there is one Mexican and one Asian group interested in buying the 55% stake and assume control of the company.

Outlook: Downside Price Risk Dominates the View

Our near-term outlook calls for a rapid easing of the supply deficit and a turn in sheet prices. However, planned mill maintenance, some of which was only recently announced, has kept near-term supply tight enough to maintain continued price gains. Preparation for these outages from Cleveland-Cliffs and U.S. Steel kept the sheet market tighter than expected over the past two months as these mills built up slab inventories in lieu of sales to the end market. But that process will now reverse.

We see upside price risk with any outage that takes longer than expected. However, the upward trend of production, slower seasonal demand, and the unavoidable bargain that imports offer, lead us to expect that sheet prices will soon reach a peak and start to ease. Further, this easing will come without considering the 5 Mt of new EAF capacity starting in the U.S. and without considering changes to S232. These changes may only serve to quickly bring sheet prices back in line with global prices, which currently is a difference of at least $500 /s.ton, inclusive of the S232 tariff and high freight costs.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com